.png)

Stocks’ Details

Aristocrat Leisure Limited (ASX: ALL)

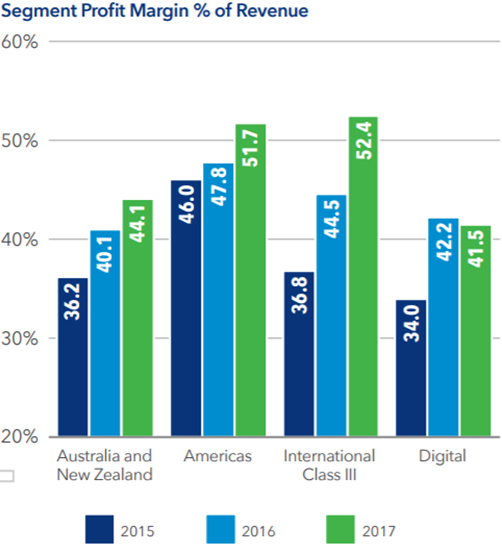

Efforts on Meeting targets: Aristocrat Leisure has reiterated its guidance for continuous growth in 2018 with contributions from bolt-on acquisitions. Aristocrat delivered a very strong result for the year 2017 despite flat market conditions and increased pressure from existing and new competitors. Group’s revenue improved over 15 per cent in reported terms and ALL recorded a revenue of more than $2.45b.EBITDA increased over 24 per cent in reported terms as compared to the prior corresponding period. The Group received the judgement of the Federal Court in respect of the Guy litigation and Court dismissed the claims made by Ms Guy. The Company went into a trading halt in February while the Federal Court of Australia was due to deliver its judgement relating to the compliance of certain electronic gaming machines with Federal legislation. In terms of changes at company level, Mrs Antonia Korsanos (Toni), the Company’s Secretary resigned and was to depart from her responsibilities by the end of March 2018. Meanwhile, Ms Cameron-Die was also appointed as the Chief Financial Officer of the Company. ALL’s acquisition of Big Fish had captured mixed views as benefits from this acquisition were pointed to be highly compelling in terms of Big Fish expected to provide a scale across its entire Digital Platform and its social casino will become the second largest social casino publisher globally; while acquisition cost was a concern. The stock prices were up by 14.6 per cent in the past six months but declined by 2.1 per cent in the last five days. Commonwealth Bank of Australia also ceased to be a substantial holder of ALL in March 2018. We believe that the stock is still “Expensive” at the current price of $24.06, and would look for a better buying opportunity.

Profit Margin % of Revenue (Source: Company Reports)

Jumbo Interactive Limited (ASX: JIN)

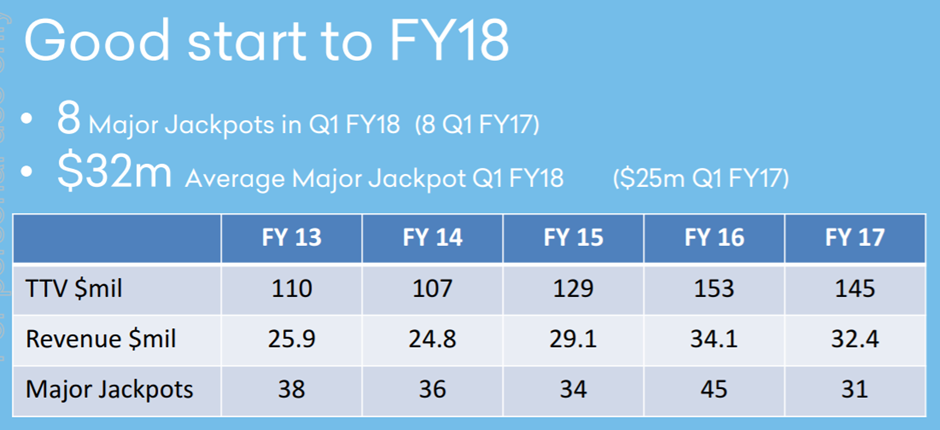

Trading Update for the first half of 2018: Group’s Customer acquisition has increased with large jackpots of $15 million or above in December 17 improving the engagement with existing customers. Revised Revenue Forecast for half year ending December 2017 amounted to $19.2 million and was about $16.0 million for the same period in the prior year. It also issued options to its Directors and staff with each option exercisable at $1.75 per share. The number of securities issued were about 50,000 (expiring on 18 November 2020) and the Company provided a notice to ASX about the same. The key risk to the company is the reliance on its business relationship with Tatts, the national lotteries business and a significant shareholder of Jumbo. Its Net Margin Percentage increased from 2016 level of 21.1% to 2017 level of 22.5%, whereas Percentage Cash Flow to Sales in 2016 was 24.5 and in 2017 it was 33.5. Its ROE in 2016 was 31.6%; and in 2017, the ROE was 12.0%. JIN stock has otherwise delivered huge gains of over 49.1 % in the last six months (as of March 29, 2018) and trades at a higher level. As per the March quarter rebalance of S&P/ASX indices, JIN has been added to All Ordinaries index, effective from March 19, 2018. We give an “Expensive” recommendation on the stock at the current price of $4.10.

Historical Performance with good FY18 start (Source: Company Reports)

Crown Resorts Limited (ASX: CWN)

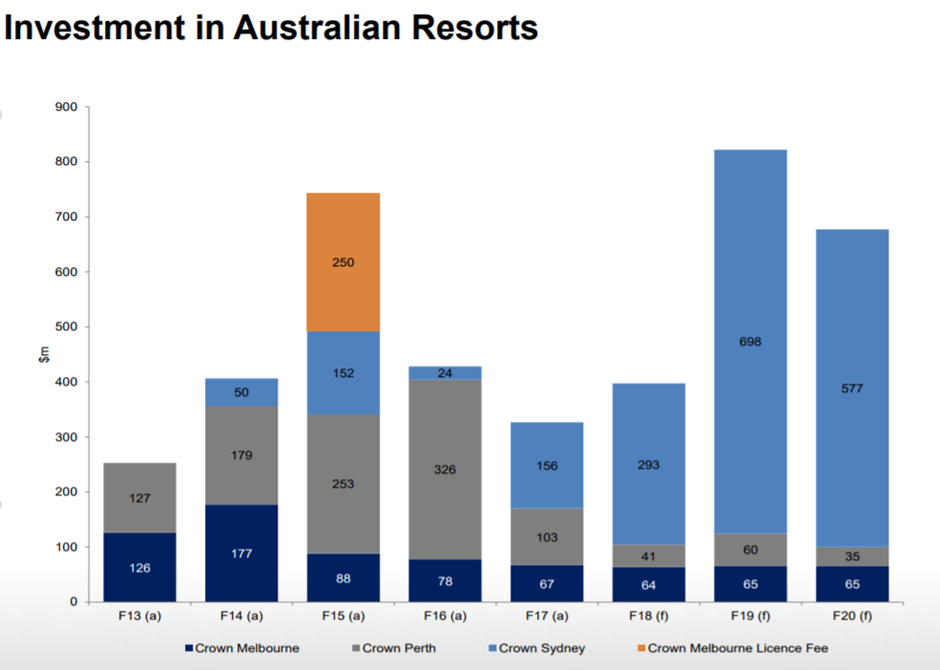

Transactions for debt reduction: Crown updated the market about its buy-back programme wherein a cumulative total of 1,276,329 of outstanding Subordinated Notes were bought back and about 4,043,371 of outstanding Notes were issued but not bought back by the Group, as on 29 March 2018. James Packer, the Director had resigned from his position due to some personal reasons. Earlier, CWN reached in-principle agreement with Mr James Packer to sell two floors of the Crown Sydney Residences at the Crown Sydney Hotel resort to Mr Packer for $60 million and this sale was approved by the Crown’s independent directors. Finally, the sale of 8,240,933 of shares which was due since long was finally settled by CPH Crown Holdings Pty Limited, a wholly-owned subsidiary of Consolidated Press Holdings Pty Limited. Recently, CWN announced that its majority owned subsidiary, Alon Las Vegas Resort, LLC completed the sale of its interest in a 34.6-acre vacant site on Las Vegas Boulevard to a subsidiary of Wyn Resorts, Limited for US$300 million. It received approximately US$264 million as sale proceeds. It also progressed on a number of transactions as a part of its ongoing debt reduction strategy; and completed the sale of its 62% interest in CrownBet for about $150 million. CWN released its half year results for the period ending on 31 December 2017 wherein Net Tangible asset backing per ordinary security on issue as on 31 December 2017 was $5.13 against $4.80 as on 31 December 2016. The Directors declared an interim dividend of 30 cents per share (franked at 60 per cent) which will be paid on April 04, 18. The Group reported a net profit of $238.6 million for the period of six months ending as on 31 December 17, lower than $359.1 million for the same period in the prior year, in actual terms. Crown Melbourne’s main floor gaming revenue increased on the pcp while non-gaming revenue was flat. Crown Perth’s main floor gaming revenue has been softer due to challenging market conditions, while non-gaming has grown in part due to the opening of Crown Tower Perth. As far as its return on capital is concerned, a special dividend was issued and approximately $500 million of shares were bought back on-market. CWN recently committed to fund approximately $2 million to Indigenous education programs. The stock price increased by 12.2% in past six months, so by looking at the overall picture and decent fundamentals in view of tourism trends while trading conditions have stayed slightly challenging, we recommend to “Buy” the stock at the current price of $12.69

Investment in Australian Resorts (Source: Company Reports)

Tabcorp Holdings Limited (ASX: TAH)

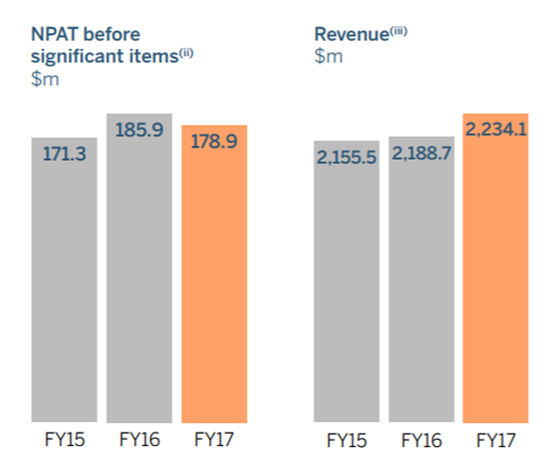

Reshaped the Business for Growth: The Group recently appointed Chris Murphy as the new Company Secretary after taking all the necessary regulatory and ministerial approvals and Michael Scott who already has all the necessary approvals was also appointed as Company Secretary. It announced about issuing long-term notes (US$1.4 billion) to the investors in US private placement market and the same are subject to the customary conditions of the market. This will extend the Company’s debt maturity profile. The proceeds from the issue of Notes will be used by the Company to fully repay the A$1.8bn bridge financing facility, put in place in connection with the combination with Tatts Group and to repay existing bank debt. Meanwhile, Vanguard Group, Inc. decreased its relevant interest in Tabcorp Holdings Limited as on December 29, 2017 to 5.295% of the issued fully paid ordinary capital, with a relevant interest in 106,462,742 ordinary shares. National Australia Bank Limited and its associated entities ceased to become a substantial holder in Tabcorp since 22 December 2017. Finally, Tatts has now been wholly-owned by Tabcorp and the latter also completed the disinvestment of Odyssey Gaming Services to Australian National Hotels which was a requirement under the authorization on the merger process. The group also announced a fully franked final dividend of 12.5 cents per share taking the full year FY 17 dividend to 25 cents per share. FY 18 dividend target is 90% of NPAT before any significant items. The share price has fallen by 21.2% this year to date and we recommend to “Hold” the stock at the current price of $4.39, at the back of the recent developments.

NPAT and Revenue growth (Source: Company Reports)

Ardent Leisure Group (ASX: AAD)

On track to Improvement: AAD has updated the market about completion of the sale of Bowling & Entertainment Division to The Entertainment and Education Group to be witnessed in first half of 2018. On the other hand, AAD’s Main Event recently achieved a constant centre revenue growth of 1.3% over the 26-week period ending on 26 December 2017 versus the prior period and this was driven by event sales growth and improving trends in walk-in business. Since 31 December 2017 to date, the Company had drawn $40,000 against its facility and issued 3,846,153 shares and thus taking the total shares issued to the date against the facility to 27,193,552 while raising $308,159. The Group earned a proforma net loss of $13.2m for the half year ending as on 31 December 2017 against $49.4m for the same period in the prior year. As US Government came out with new Tax Reforms which reduced the corporate tax rate from 35% to 21%, it impacted Main Event’s deferred tax balances which now need to be restated as the same will be realised at the lower tax rate. Attendances at Dreamworld were also up by 41.2% between 10 December 2017 and 31 January 2018 as compared to the same period in the prior year. It has also changed its retail calendar year and reporting period for second-half for 2018 will be 27th December 2017 to 26th June 2018. The Group is actively looking out for some new joint ventures to explore better business opportunities. The share price was down by 7.75% in the past three months; and looking at the improvement, we recommend to “Hold” the stock at the current price of $1.845

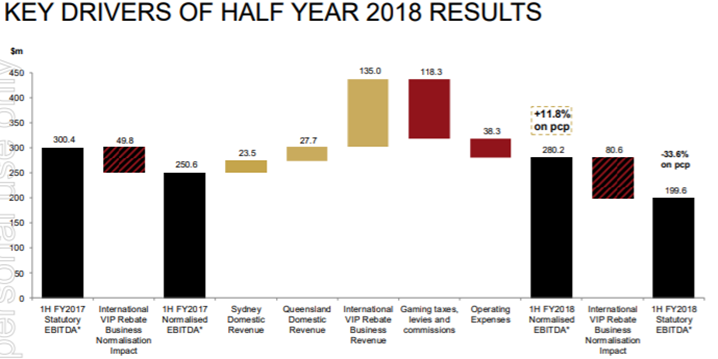

The Star Entertainment Group Limited (ASX: SGR)

Expansion of the strategic partnership:The Group is expanding its strategic partnership with Chow Tai Fook Enterprises Limited (CTF) and with Far East Consortium International Limited (FEC) to enhance the long-term value of The Star’s properties and core businesses. This will accelerate and will de-risk Star’s existing capital-light strategy of investing in its core business through joint venture developments with partners who have complementary skills and businesses. This partnership requires arrangements at both the ends, operational and financial. For instance, it requires commitment by the parties to jointly pursue and participate in significant growth developments. For this, equity investment by CTF and FEC via $490 million placement is required to be completed in SGR; and post this, Star’s gearing of 2.1x Net Debt/Actual 12 month trailing EBITDA as on 31 December 17 will reduce to 1.2x Net Debt/Actual 12 month trailing EBITDA as on 31 December 17 on a pro-forma basis which will provide The Star with enhanced financial flexibility so that it can fund any kind of development and other growth projects.

On the performance front, Group’s Star Gold Coast and International VIP Rebate Business are witnessing growth while Star Sydney is still in a mixed trading scenario. Actual Group’s gross revenue for the period 1 January to 25 March 2018 was flat, with a win rate of 1.11 per cent in the International VIP Rebate business which is below the theoretical rate of 1.35 per cent in 2HFY18 year to date. In the past three months, the share price declined by 12.99 per cent (as at March 29, 2018), and despite this, the stock seems to be a bit “Expensive” at the current market price of $5.29

Key Drivers of Half Year 2018 Results (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...