The Federal Budget has recently jolted the Australian market, particularly, the banking sector while charging high on the big banks with a new levy. On the other hand, there were some takers who rejoiced with the moves of the Australian Government. Let us have a look at the entire scenario with a focus on banking sector stocks.

Rebound expected in GDP:Australia’s transition from the investment phase of the mining boom to a broad-based economic growth is said to have advanced well; and historically low interest rates, a lower exchange rate and a flexible jobs market have been supporting the turnaround in the economy. Importantly, the budget snippets highlighted that the economy has generated jobs growth over the past few years despite huge fall in mining investment and commodity prices from record highs. Notably, the government has now planned to make significant investments of $50 billion in 2017-18 on infrastructure and in the form of grants to the states and others for capital investments. The Australian GDP is now expected to rebound to 2.75% in 2017-18 and 3% in 2018-19 as the detraction from mining investment eases and growth in household consumption and non-mining business investment improves. Moreover, an improving global growth will boost the scenario and Australian businesses are expected to find support from resource exports with buoyance from Australia’s tourism and education services scenario.

Levy of 6 basis points on banks with liabilities above $100 billion is a big setback:The four major banks have caught attention recently as the same are seen to have significant pricing power and this benefits the shareholders at the expense of the customers as the financial sector is highly concentrated. As part of new reforms, the government has announced several measures to support the economic growth and deliver better outcomes for small businesses and to boost the competition in financial services. The government announced a six basis-point levy on the deposits of the country's five biggest banks in its annual budget, a measure that will bring A$6.2 billion over next four years and the levy will be used to support budget repair. With the implementation of new levy, Australia's four largest banks, Commonwealth Bank of Australia, Westpac Banking Corp, Australia and New Zealand Banking Group, National Australia Bank and Macquarie Group will pay the charge on their liabilities including corporate bonds, commercial paper, certificate of deposits and tier-2 capital instruments. However, ordinary bank deposits, mortgages and other deposits protected by the financial claims scheme will be excluded from the levy base. The levy will also provide a more level playing field for smaller, regional banks and non-bank competitors.

Size of Australian banking groups (by total resident assets); Source: Budget documents 2017-18

New inquiry on ‘Big Four' banks and reducing barriers for new banks:Following a series of scandals in the banking sector and public allegations against the "Big Four" banks, the government has tasked the Productivity Commission to commence a review, on 1 July 2017, on the state of competition in the financial system. Further, to promote a more systematic approach for monitoring and to improve competition, Australian Prudential Regulation Authority (APRA) is reviewing existing bank licensing processes to make it more accessible to new entrants. APRA is already working on to reduce barriers for innovative new entrants by addressing significant obstacles such as, the limitation on closely-held ownership in the Financial Sector (Shareholdings) Act 1998 (FSSA); the prohibition on the use of the word ‘bank’ by certain authorized deposit?taking institutions (ADIs); and burdensome bank licensing processes. As part of new legislation, the government will remove the prohibition on the use of the term ‘bank’ by ADIs with less than $50 million in capital as it allows smaller ADIs to benefit from the reputational advantages of being called a ‘bank’.

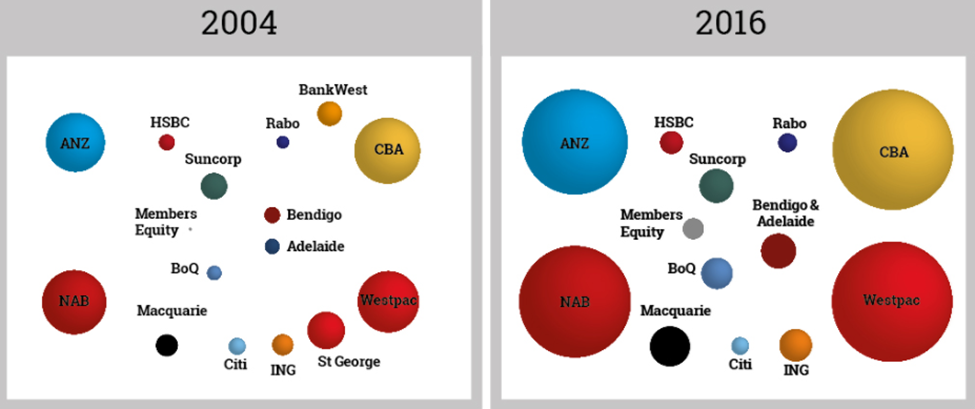

Major bank liabilities are greater than the size of Australian economy; Source: Budget documents 2017-18

Setting up a one-stop shop for banking dispute resolution services:The Government will also establish a one-stop shop (The Australian Financial Complaints Authority) to ensure consumers have access to free, fast and binding dispute resolution services. Further, the Government will legislate a new Banking Executive Accountability Regime with enhanced powers for the APRA (Australian Prudential Regulation Authority) to remove and disqualify an executive and enforce new obligations on bank conduct, with penalties (up to $200 million) when those norms are not met.

Improving prospects for smaller and regional banks while the headwinds are rising for big banks:The new levy is expected to wipe out a considerable portion of cash profits of top four depending on the composition of their deposits, and further expected is an impact on future dividend payments to shareholders. With the new norms, growth prospects for regional banks and small lenders (Bendigo & Adelaide Bank, Bank of Queensland and Suncorp) now seem to be optimistic. However, the real impact of levy charges on bottom lines of major banks is yet to be seen. As of now, it may be perceived that the cost of the bank levy if passed on to shareholders and staff, and through other means related to higher interest rates, may call-in for a disastrous outcome. The housing market may also come under pressure if the big banks who already have repriced the mortgage books recently, go-in for further hikes. Thus, the short time frame for implementation of new levy is further signaling eruptions of many economic consequences. To address many concerns, the big banks attended a brief by Treasury officials but many questions went unanswered in the meeting. The voice being echoed by a majority of stakeholders is that the move has creeped in to reduce deficit and companies that look soft are being targeted. Ultimately, transitioning from big banks to smaller lenders is one approach that has picked up amidst this turbulent scenario, to manage risks at the moment.

Australia and New Zealand Banking Group Ltd

.JPG)

ANZ Details

Implementing agile approach to transform customer experience:Recently, ANZ announced that it will implement the scaled agile approach to organizing and delivering work within its Australia division to enable it to respond more quickly to changing customer expectations, engage and empower staff, and continue to improve efficiency. It has been already using the strategy to deliver around 20% of technology and digital projects including initiatives such as Apple Pay. The use of agile means a much less hierarchical to build around small, collaborative, self-directed teams focused on delivering continuous improvement in the customer experience. For H1FY17, ANZ reported 24% year on year (yoy) growth in unaudited cash profit to NZ$928 million, while posting unaudited statutory profit of NZ$869 million (up 14%), led by increased other operating income, higher trading income and valuation gains on derivatives aided by 12% decline in expenses. Further, lower levels of credit losses reflect improvements in credit quality in the commercial and agri portfolios, partially offset by new provisions. On the new levy, ANZ CEO has described the same as a “regrettable policy”, which would be putting pressure on millions of ordinary Australians. Given the challenging operating environment, the stock lost 4.4% in last five days (as at May 11, 2017). We maintain a “Hold” on the stock at the current share price of $ 29.22

.png)

ANZ Daily Chart (Source: Thomson Reuters)

National Australia Bank Ltd

.JPG)

NAB Details

Rise in cash earnings but subdued growth outlook:For H1FY17, NAB reported a 2.3% increase in cash earnings at the back of lending and trading income, while there was a 0.8% rise in costs owing to higher redundancy and general expenses (technology depreciation costs). The total bad debt increased by $19 million to $394 million and included an increase in provision overlays of $89 million for potential risks relating to the commercial real estate portfolio. Net interest margin fell by 11 basis points. Banks Common Equity Tier 1 (CET1) ratio stood at 10.1% as at 31 March 2017, an increase of 42 basis points in H1FY16. Further, the group has provided a subdued growth outlook due to challenges in the operating environment. In last five days, the stock has edged lower by less than 1% (as at May 11, 2017). We maintain a “Hold” on the stock at the current price of $ 32.33

.png)

NAB Daily Chart (Source: Thomson Reuters)

Commonwealth Bank of Australia

.JPG)

CBA Details

Concerns over margins: During Q3FY17, the group’s Net Interest Margin fell on account of the better average liquids and competition effects. The group reported a cash earnings of over $2.4 billion in the quarter while the unaudited statutory net profit reached over $2.6 billion.Deposit funding and liquidity coverage ratio (LCR) stood at 67%, 124% respectively, while Common Equity Tier 1 (CET1) capital ratio improved by 37 basis points to 9.6% on an APRA basis.

.png)

Funding and Liquidity (Source: Company Reports)

On the other hand, CBA’s insurance income was impacted by adverse weather conditions. In last five days, the stock fell over 2.7% (as at May 11, 2017) but still trades at higher levels. We maintain an “Expensive” recommendation at the current price of $ 81.67

.png)

CBA Daily Chart (Source: Thomson Reuters)

Westpac Banking Corp

.JPG)

WBC Details

Increasing mortgage rates across business portfolio:During H1FY17, Westpac further strengthened its balance sheet, with the common equity tier-1 (CET-1) capital ratio of 10.0% against 9.5% in H2FY16, which is above the group’s preferred range of 8.75% to 9.25%. Moreover, the group’s funding mix also strengthened with a rise in more stable funding sources (customer deposits and long term wholesale funding) while general insurance gross written premiums reported a 2% yoy growth. Further, liquidity position has remained solid at liquidity coverage ratio (LCR) of 125%, while the new net stable funding ratio (NSFR) stood at 108%. The bank has been expected to increase mortgage rates across a range of products as it will increase variable home loan rate for owner occupiers by 3-8 basis points, and 23-28 basis points for property investors. Westpac group has also reacted to the new bank tax by stating it to be “a hit on the retirement savings of millions of Australians as well as all bank customers”. Given the prevailing scenario with stock fall of over 3.6% in last five days as at May 11, 2017, we maintain an “Expensive” recommendation on the stock at the current price of $ 32.57

.png)

WBC Daily Chart (Source: Thomson Reuters)

Bendigo and Adelaide Bank Ltd

.JPG)

BEN Details

Results impacted by rising competition: The bank reported an after tax statutory profit of $209.0 million for the six months ending on December 31, 2016. Underlying cash earnings rose 0.4% year on year (yoy) to $224.7 million while cash earnings per share fell 0.9 cents to 48 cents yoy. The bank’s net interest margin witnessed pressure as it was impacted by additional liquidity for the Keystart portfolio acquisition, while the increasing competition remains a concern despite the group’s focus on customers. The stock has risen 2.5% in last five days as at May 11, 2017. However, given the fragile prospects, we maintain an “Expensive” rating on the stock at the current price of $ 12.12

.png)

BEN Daily Chart (Source: Thomson Reuters)

Bank of Queensland Ltd

.JPG)

BOQ Details

Gaining over the rising headwinds for big banks:For H1FY17, BOQ reported 2% and 3% yoy decline in cash earnings and profit before tax led by intense competition in a low interest rate environment contributed to flat loan growth and 5bps decline in Net Interest Margin (NIM). However, management has guided for better H2FY17 as number of the headwinds that occurred in 2016 waned in H1FY17. While the big banks pay charge on their liabilities including corporate bonds, commercial paper, certificate of deposits and tier-2 capital instruments, BOQ seems to be well positioned to take advantage from the situation for earning higher margins. The stock has risen 2.7% in last five days as at May 11, 2017. We give a “Buy” recommendation on the stock at the current price of $ 11.92

.png)

BOQ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...