.png)

Stocks’ Details

Flight Centre Travel Group Limited (ASX: FLT)

Strong First Half Growth: In releasing its accounts for the six months to December 17, FLT revealed record global sales and $139.4 million of profit before tax (PBT) for the period. PBT increased by 23.2% over $113.2 million of underlying 1H PBT achieved last year. Profit during the period was slightly above the targeted 1H range ($120 million-$135 million) which compelled the Group to lift its full year guidance to a $360 million-$385 million as compared to the initial target of a $350 million-$380 million of underlying PBT. FLT’s business in Europe, the Middle East and Africa again performed strongly with TTV increasing by 16% and profit increasing by 37% and so the region generated almost 14% of the group sales and about 25% of the group PBT. The Transformation program that was initiated late in FY17 to ensure that FLT achieves scalable profitable growth throughout the economic sale has started to gain momentum and the company made a solid progress towards its 7-2-100 targets during the 1H. FLT also expects further market growth globally as the Golden Era of Travel continues and FLT’s transformation program is expected to deliver 2H benefits, along with some additional cost and so the 2H cost is expected to increase. The share price increased by 10.4% as on February 22, 2018 and we give a “Hold” recommendation at the current market price of $55.26

Results by Country (Source: Company Reports)

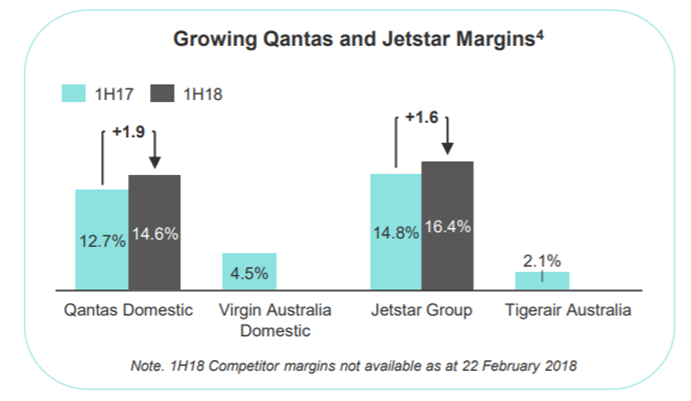

Qantas Airways Limited (ASX: QAN)

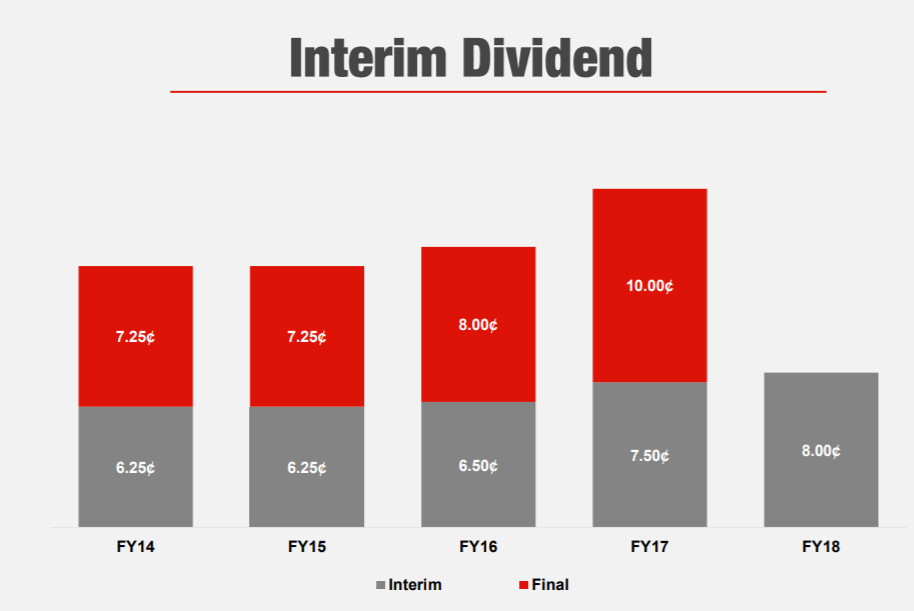

Strong Portfolio of businesses: The Group delivered its highest-ever first half underlying profit before tax of $976 million for the six months ending 31 December 2017. The result surpasses the previous record of $921 million that was achieved in the first half of FY16. Despite the recent increases in fuel cost and a continued international capacity growth, it has performed really well. Qantas and Jetstar domestic flying operations combined posted their highest ever first half underlying EBIT of $652 million. Jetstar International operations generated strong earnings which was helped by the operating costs of the 787-8 Dreamliner but was impacted by around 10 million from the Bali ash cloud disruption. Qantas loyalty posted another record profit in the first half of $184 million and was up by 1.7 per cent. Operating cash flow increased by 48 per cent and reached a record level of $1.7 billion. The Board announced up to $500 million of capital that will be returned to shareholders and the interim dividend of 7 cents per share will be paid on 12 April 18. The share price decreased by 12.46% in the past six months and increased by 5.88% as on 22 December 17, and we see an opportunity given the price movement and recommend a “Buy” at the current market price of $5.58

Growing Margins (Source: Company Reports)

Air New Zealand Limited (ASX: AIZ)

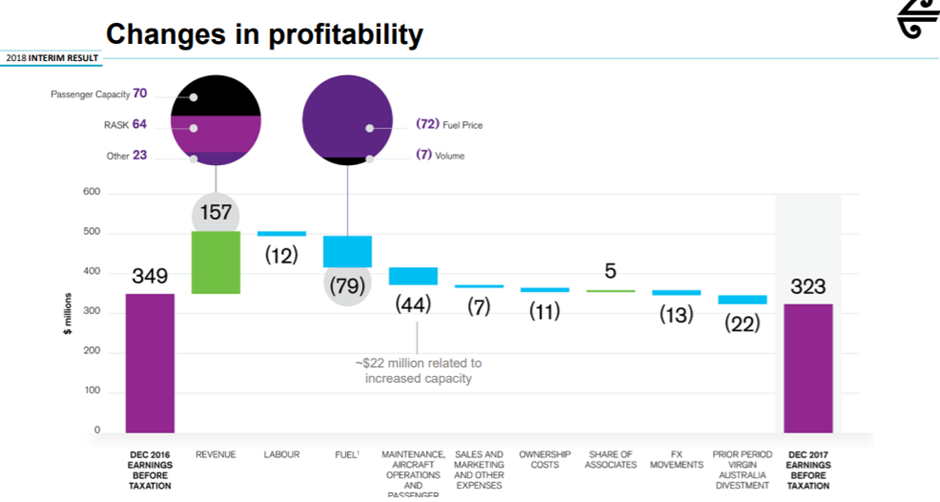

Mixed financial performance: AIZ announced earnings before taxation of $323 million for the first six months of 2018 as compared to $349 million in the prior period. The group’s operating revenue growth was 5.6 per cent, with robust demand across all the markets and particularly strong growth in short-haul network. Passenger revenue reached an all-time record for an interim result at $2.3 billion. The interim dividend of 11.0 cents per share will be paid on 16 March 2018. Cash flow from operations grew by $103 million or by 27 per cent and amounted to $479 million that was driven by growth in cash operating earnings and a strong working capital cash flow as the business grew. The airline announced the launch of a new direct service to Taipei which will commence in November 2018. However, the stock looks “Expensive” at the current market price of $2.83

Changes in Profitability (Source: Company Reports)

Webjet Limited (ASX: WEB)

Strong Growth in Revenue: The Company’s B2B Travel Business, WebBeds sold hotel rooms to travel industry partners via online channel. Following the acquisition of JacTravel, WebBeds is now the #2 B2B player globally and #2 B2B player in the important European market. In the 6-month period to 31 December 2017, the Company delivered a significant uplift in all key financial metrics over the prior corresponding period with Total Transaction Value, Revenue, EBITDA and NPAT rise of 54.9%, 290%, 62.8% and 25%, respectively. For the six months period ending on 31 December 2017, its statutory EPS decreased by 55% and edged to 16.5 cents and whereas EPS from continuing operations increased by 9% and amounted to 17.8 cents. An interim dividend for the for six months ending 31 December 2017 was $0.08 per share and was fully franked and totalled to $9.5 million. WEB stock price zoomed up 16% on 22 February 2018 at the back of the update. However, the stock seems to be “Overvalued” at the current market price $12.01

Interim Dividend Performance (Source: Company Reports)

Crown Resorts Limited (ASX: CWN)

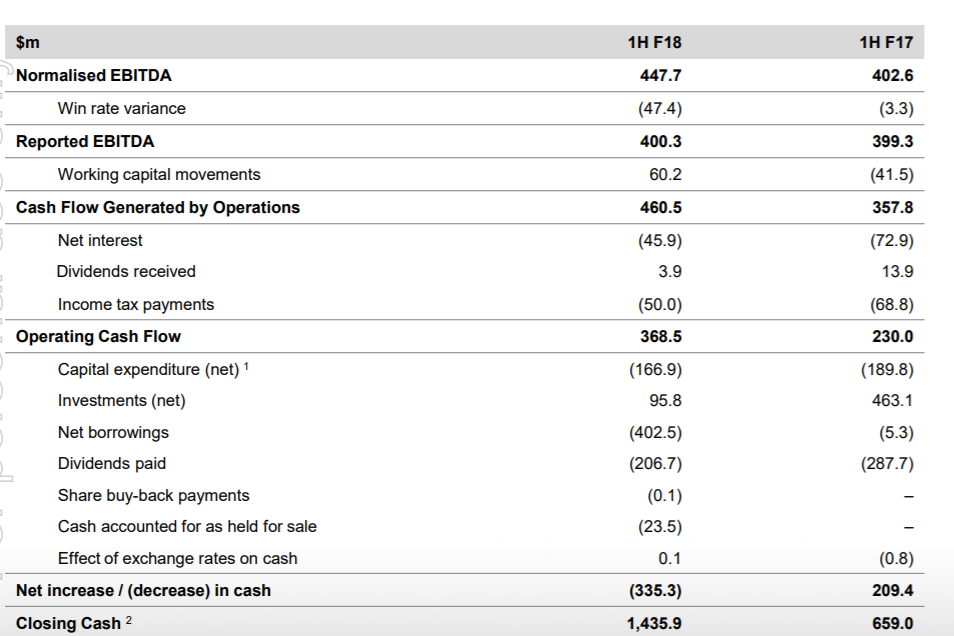

Improved trading conditions: CWN declared its results for the half year ending 31 December 2017 wherein total normalised revenue across Crown’s Australian resorts increased by 4.8% on pcp basis. Group’s VIP program player turnover in Australia of $22.6 billion has been encouraging. Main floor gaming revenue increased by 0.7 per cent. Normalised EBITDA and Revenue from Crown Melbourne was up by 7.2% and by 8.2% on pcp basis, respectively. Crown is working diligently to deliver the Crown Sydney Hotel Resort at Barangaroo South and Crown has commenced stage one sales of the Crown Sydney Residences and that will be situated above the Crown Sydney Hotel Resort. The project is expected to complete in first half of the calendar year 2021. Crown intends to implement the on-market share buy-back of up to approximately 29.3 million shares on or after 23 February 2018. The group declared an interim dividend of 30 cents per share. The interim dividend is franked to 60% and will be paid on 4 April 2018. The growth prospects look encouraging and we recommend a “Buy” at the current market price of $13.05

Cash Flow Analysis (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...