NetComm Wireless Ltd

.JPG)

NTC Details

Growth prospects in place: NetComm Wireless (ASX: NTC) witnessed an initial stock rally of about 2% on August 28, 2017 before a stock plunge of 5% with the release of its FY17 full year results. The result entailed record revenue growth with group revenue rising 26.3% to $107.6 million owing to growth in M2M Business of fixed wireless, Fibre to the Curb (FTTC) and machine-to-machine. Revenues from the broadband business declined by 19.4% partly due to a slowdown in sales of powerline devices to a key Australian customer. Group’s earnings before interest, tax, depreciation and amortisation slipped by 41% while operating loss after income tax was $1.7 million down from $2 million of previous year. NTC has no debt and has cash of $22.1 million.

.png)

Driving growth in FY18 and beyond (Source: Company Reports)

The group’s key projects with nbn have begun to scale while those relating to AT&T fixed wireless have commenced. Further, investments have been made to drive growth going forward. In the last six months (as at August 25, 2017), the stock has fallen 18% and looks to be an investment opportunity with the latest result and growing orders relating to FTTC and AT&T projects. We give a “Buy” at the current price of $ 1.43

.PNG)

NTC Daily Chart (Source: Thomson Reuters)

Melbourne IT Ltd

MLB Details

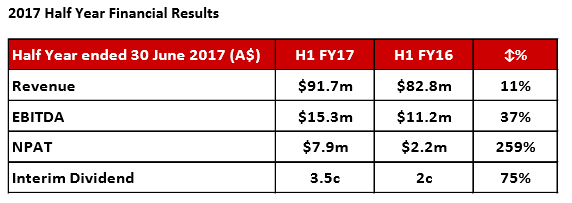

Guidance Reaffirmed: Melbourne IT (ASX: MLB) announced its results for the half year ending 30 June 2017, with strong increases in revenue, EBITDA, and net profit after tax. The Board of Melbourne IT also declared an interim dividend of $0.035 (100% franked) at the back of the strong result. The group’s strategy of transitioning Melbourne IT to a digital solutions business is said to have delivered strong organic growth. Its Enterprise Services division is now a leading end-to-end digital solutions provider for large Enterprise and Government customers; and the fully integrated Infoready business (acquired in April 2016) is also delivering the expected growth. Further, the group expects to witness strong momentum from the rapidly growing businesses in data analytics and mobile apps. The group’s earlier embattled Small to Medium Business has also returned to Profitable Growth.

Result (Source: Company Reports)

Melbourne IT has reiterated that it expects to report underlying EBITDA for 2017 in the range of $37.5m - $41.5m. Underlying EPS is expected to be in the range of $0.17 to $0.19 per share. Trading at higher levels, we believe that the stock is “Expensive” at the current price of $ 3.15

MLB Daily Chart (Source: Thomson Reuters)

Nearmap Ltd

.JPG)

NEA Details

Rise in global subscriptions and average revenue per subscription: Nearmap Ltd (ASX: NEA) stock price plunged 7% on August 28, 2017 owing to volatility while the group had released a decent result for the financial year ended 30 June 2017 (FY17) with total revenue of $41.1 million, up 31% on the prior year. EBITDA of $6.0 million was delivered within guidance. Further, statutory loss after tax was $(5.3) million against FY16 figure of $(7.1) million. NEA’s global subscriptions surged to over 7,800, with group average revenue per subscription (ARPS) increasing to about $6,000. Group Annualised Contract Value (ACV) was $47.0 million, up 29% on the prior comparative period; and the portfolio lifetime value has increased to $365.5 million from $223.9 million at 30 June 2016. The group made significant progress in the year with Australian business continuing to grow strongly under new leadership. NEA has also captured and published content from 12 major US cities from its target of 50% US population coverage. Going forward, the target has been said to capture five major metropolitan cities in Australia. HyperCamera2 capture in the US has also increased the frequency with which areas are being captured in the United States from 2 to 3. In Australia, NEA has increased the frequency of capture in regional centres and expanded the footprint to areas of urban development.We give a “Buy” recommendation at the current price of $ 0.58

.PNG)

NEA Daily Chart (Source: Thomson Reuters)

Wisetech Global Ltd

WTC Details

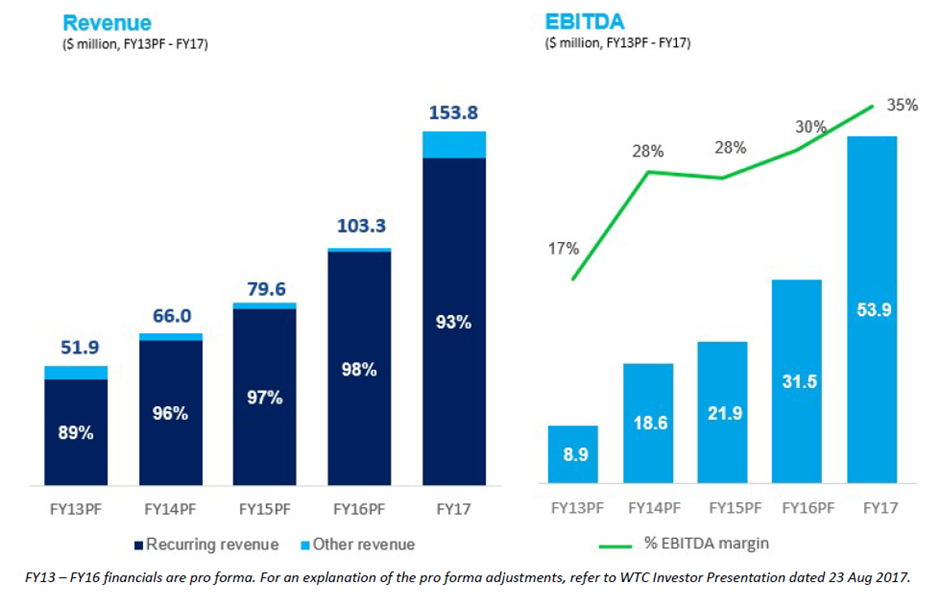

Boost from existing customer revenue growth: Wisetech Global Ltd (ASX: WTC) reported a 50% surge in FY17 statutory revenue of $153.8 million against FY16 while net profit attributable to equity holders of $31.9 million was up 1371%. There has been 127% increase in net profit at the back of significant growth in revenue from existing customers across transactions, modules and geographies and new sales worldwide. Primarily, WTC has got a boost from existing customer revenue growth of $27.2 million, delivering 78% of the FY17 organic revenue growth. The group now expects FY18 revenue of $200 - $210 million (growth of 30% - 37%) and EBITDA of $71 - $75 million (growth of 32% - 39%).

Revenue and EBITDA (Source: Company Reports)

Wisetech Global invested over $50.4 million in FY17, representing 33% of its revenue and over 50% of its people in product development, significantly expanding its platform. The company is progressing well with regards to integration of its acquisitions in China and South Africa and, has announced 7 further acquisitions in Italy, Germany, Brazil, Australia and Taiwan. The stock has risen 44% in last six months (as at August 25, 2017) and is now trading at higher levels already accounting for the strong performance and boost from latest acquisitions. We give an “Expensive” recommendation at the current price of $ 7.85

.PNG)

WTC Daily Chart (Source: Thomson Reuters)

NEXTDC Ltd

.JPG)

NXT Details

Attaining new debt funds: NEXTDC Ltd (ASX: NXT) has updated that the Asia Pacific Data Centre Group (ASX: AJD) has unanimously recommended to go with NEXTDC’s unconditional all-cash offer of $1.87 per security in the absence of a superior proposal. The offer represents 19.5% premium to the $1.57 closing price of AJD securities on 1 May 2017. Meanwhile, 360 Capital Group (ASX: TGP) also updated about the proposal it made to AJD securityholders to purchase all of the securities it did not own for $1.80 subject to certain conditions, including due diligence which is under process. TGP is now expected to inform the market soon. On the other hand, NXT has attained financial close on its A$300 million 3-year Syndicated Senior Secured debt facilities. These will replace the existing A$100 million undrawn senior secured debt facility. NXT will use the majority of the new debt funds for future growth capital expenditure and developments. We give a “Hold” recommendation at the price of $ 4.25, aheadof its FY17 full year results to be announced on August 31, 2017.

NXT Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...