Boral Limited (ASX:BLD)

.png)

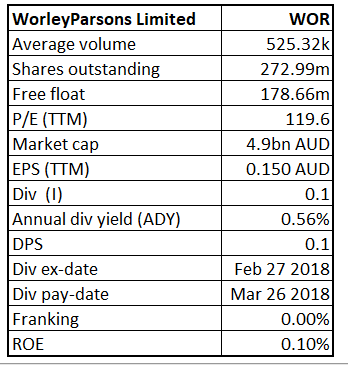

BLD Details

Impact from Infrastructure Spend - Boral Limited is an Australia-based company, which is engaged in the provision of building and construction materials. Lately, the group signed a deal with Mirvac to incorporate an extra 278 hectares of land in the development arrangements for Boral's Donnybrook property in Victoria. Under the arrangements, Mirvac will encourage the urban development of the 465-hectare sites over a multi-decade time frame. BLD expects property earnings to be at the high end of its guidance range of $55-$65 million of EBITDA for FY2018.

.png)

Revenue and Statutory NPAT Performance (Source: Company Reports)

Significant earnings are expected from FY2028 to FY2037 as the land is being progressively developed. The Group will be releasing its financials around 29 August 2018. While there is a threat from US-China trade war, Boral Limited that already has a large US exposure, is expected to benefit from the infrastructure spending boom in both the US and Australia market. The US is planning to spend big on infrastructure because there might be a need to offset the impact with some form of additional stimulus.

.png)

EBITDA Variance Analysis (Source: Company Reports)

The Group has made few management changes in its Board like it appointed former ANZ Bank executive and ex-Reserve Bank board member, Kathryn Fagg as its new chairman and it is expected that these changes will bring some positive impact on the Group. The stock declined by 6.20 per cent in last one year (as on 16 July 2018 ) and by 1.07 per cent as on 17 July 2018. We recommend to “Buy” the stock at the current market price of $6.43 (near to its 52-week low price, that is $6.17) by looking at the potential and the impact from the infrastructure spending.

BLD Daily Chart (Source: Thomson Reuters)

QBE Insurance Group Limited (ASX:QBE)

.png)

QBE Details

Positive operating environment- QBE Insurance is an international property and casualty insurance company based in Australia, but it only writes about 24% of its annual gross earned premiums in its home country. QBE is now targeting to achieve the combined operating ratio (COR) in the range of 95.0 per cent - 97.5 per cent in 2018 and investment return in the range of 2.5 per cent - 3.0 per cent given the various initiatives undertaken by the group.

The Group performed well in the first half and generated a substantial cash profit, and a dividend of 22 Australian cents per share which represented a pay-out of 61 per cent which was consistent with its dividend policy of paying up to 65 per cent of cash profits. The Group is planning to release its financials on 16 August 2018. It is expected that some pressure might be persisting on operating margins due to potential negative changes to its reinsurance structure in 2019, but these risks are already factored in the stock price and the group seems to be free from drags that were seen last year in terms of impairments. The Group has been performing well in Europe, North America and Australia.

.png)

Earnings Performance (Source: Company Reports)

The Company is making continuous efforts to achieve consistent excellence towards improvement in underwriting quality, pricing and claims especially it is focussing on repositioning its North America operations so that it delivers an improved underwriting performance and is remediating its Asia operations through improved pricing and risk selection. Rise in the bond yields or appreciation of US Dollar can have an impact on the Group’s profits. The stock price has been declining in the last one year and was down by 20.05 per cent (as on 16 July 2018) but started rising in last three months with a surge of 4.5% in last one month. We give a “Buy” recommendation at the current market price of $9.82 by looking at the interest-rates scenario and positive operating environment of the sector.

.png)

QBE Daily Chart (Source: Thomson Reuters)

REA Group Limited (ASX:REA)

.png)

REA Details

Positive Outlook- REA Group Limited is engaged in the real estate online advertising and related services. Recently, ACCC (Australian Competition and Consumer Commission) has given green signal for the acquisition of Hometrack Australia Pty Ltd by realestate.com.au Pty Ltd. It is expected that this transaction will generate synergy benefit to REA once the Hometrack business is fully integrated into REA’s platforms as it is expected that Hometrack Australia will deliver revenue between $13 million to $15 million and EBITDA between $6 million to $ 7 million for their financial year ending on 30 September 2018. During past few months, the Group has experienced some exciting developments, including a rapidly growing portfolio of original content. The Company will release its financials on 9 August 2018.

.png)

Group EBITDA Performance (Source: Company Reports)

ROE improved from (9.2 per cent) in June 2017 to 15.9 per cent in December 2017.The Group is seeking some interest with regards to overseas based property websites. It is expected that the Group’s earnings might grow significantly (over 15 per cent per annum) for the next 2 years. In February 2018, the Board of Directors declared a semi-annual cash dividend of $0.10 per share for Class A Common Stock and Class B Common Stock and this was paid on 18 April 2018.

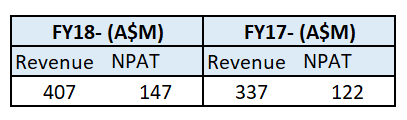

Revenue and NPAT Performance (Source: Company Reports)

It was worth noting that for nine month period (ending on 31 March 2018) the Group repaid A$120 million (approximately $93 million) of the A$480 million revolving loan facility it used to fund the iProperty acquisition, corresponding to the sub facility due in December 2017. In last six months, the stock price jumped up by 20.28 per cent and 16.64 per cent in last three months as on 16 July 2018.By looking at the overall performance and real estate and information technology landscape, we give a "Hold” recommendation at the current marketprice of $88.52.

REA Daily Chart (Source: Thomson Reuters)

Kathmandu Holdings Limited (ASX:KMD)

.png)

KMD Details

Enhanced in-store customer experience - Kathmandu Holdings Limited is engaged in design, marketing and retailing of clothing and equipment for outdoor, travel and adventure. The Group recently released its report on sales performance and forecast earnings for the year ended 31 July 2018. The Group reported that its sales (year to date to 24 June 2018) were up by 7.7 per cent from last year. In addition, Kathmandu gross profit margin was 240 bps (2.4%) above last year due to improved full price sell through, and a higher average selling price. The Group expects that its FY2018 EBIT and NPAT (after $2.0m Ob?z acquisition transaction costs) will be in the range of $72-$77 million and $48-$52 million respectively. The Group’s second half performed well across both Australia and New Zealand, with Australia experiencing double digit same store sales growth and was driven due to successful launch of innovative new products, enhanced in-store customer experience, inspiring content and engagement on social media and digital channels. The Group will release its financials on 18 September 2018.

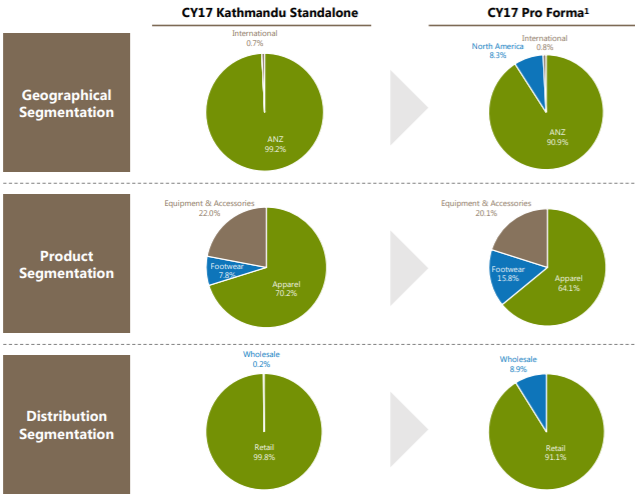

Pro-Forma Combination Analysis (Source: Company Reports)

As a result, the Board of Directors declared fully franked interim dividend of NZ$ 4.0 cents per share which is in-line with the previous corresponding period. The group agreed to acquire US-based Oboz Footwear LLC for a base cash consideration ofUS$60 million and earn-out of up to US$15 million. The objective of this deal was to expand its footprint into North America regions via Oboz distribution channel.

It is expanding in US markets also and has a solid expansion strategy. The stock was down by 3.42 per cent as on 17 July 2018 while it was up by 26.96 per cent in last one month as on 16 July 2018. We give a “Buy” recommendation at the current market price of $2.82 by looking at the expansion strategies that Company has been undertaking.

.png)

KMD Daily Chart (Source: Thomson Reuters)

WorleyParsons Limited (ASX:WOR)

WOR Details

Mining Contracts in Pipeline - WorleyParsons is a leading global provider of professional services, such as engineering procurement and construction management, to the oil, gas, mining, power and infrastructure sectors. Recently, Advisian, the global consulting firm of WorleyParsons, has been appointed as the owners’ engineer to Noor Energy 1 for a 700 MW concentrating solar power installation in Dubai. Further, Advisian will support the project with basic and detailed engineering, technology risk management, factory acceptance testing and technical support as required during construction and commissioning and the contract is for four years and Advisian will deliver the project using teams across Spain, Shanghai and Dubai offices.

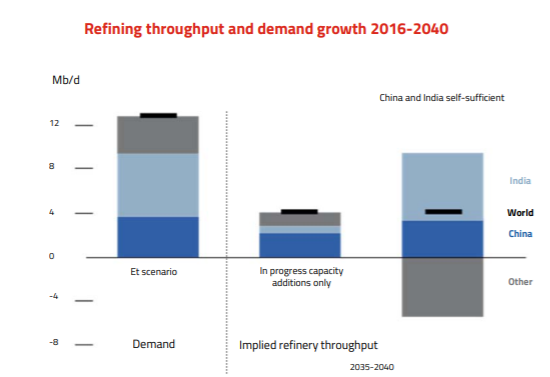

Demand Growth (Source: Company Reports)

The Group was recently awarded a contract extension by Chevron Australia to continue providing services to support Chevron’s assets of Australasian Strategic Business Unit. Additionally, WOR’s backlog is strong, has strong operating and financial metrics, bid activity is increasing and UK acquisition is delivering results. The group lately bagged the offshore engineering, procurement, construction, installation and commissioning (EPCIC) contract by Neptune Energy; and a contract extension by Maersk Oil UK.

It is expected that commodity price scenario will boost the contractual works from the mining and energy companies. The Group will release its financials on 22 August 2018. The stock was down by 3.28 per cent as on 17 July 2018 with change in commodity prices and overnight softness developing for oil. The stock otherwise rose up by 20.48 per cent in three months as on 16 July 2018. One can “Hold” the stock at the current market price of $17.35 (which is near its 52-week high price of $18.37).

WOR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...