National Australia Bank Limited

.png)

NAB Details

Issue of Subordinated Notes: National Australia Bank Limited (ASX: NAB) is a well-known bank in Australia. The market capitalisation of the bank stood at A$73.48 Bn as on 13th January 2020. The bank has recently responded to the civil legal action by ASIC in the Federal Court with respect to the alleged breaches concerning ongoing fee arrangements with clients of NAB Financial Planning. The key personnel of the company added that NAB has already acknowledged failures where customers have paid fees for services they didn’t receive and paid $37.8 million to 27,500 NAB FP clients. Remediation of the same commenced in December 2018 and is anticipated to wrap up by June 2020. In another update, the bank announced that it has issued CAD1,000,000,000 subordinated notes due June 2030, with respect to its US$100,000,000,000 global medium-term note programme. The following picture provides an overview of financial performance for FY19:

.png)

FY19 Performance (Source: Company Reports)

Increased Financing Target: The bank has committed to be a leading arranger of renewable energy finance of Australia and in mid-November 2019 it increased its environmental financing target from $55 billion to $70 billion by 2025. NAB plans to half its financing to thermal coal mining by 2028 and intends it to be effectively at zero by 2035.

Valuation Methodology: P/E Multiple Approach

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The bank has strengthened its financial settings as well as its capital position. The bank currently stands above APRA’s unquestionably strong capital requirement for January 2020. We have valued the stock using the P/E based relative valuation approach and arrived at a target price, which is offering an upside of lower single-digit (in percentage terms). Hence, considering the cost savings amounting to $480 million in FY19, significant uplift in capability as well as innovation in its leading SME franchise, we give a “Buy” recommendation on the stock at the current market price of A$24.930 as on 13th January 2020.

.jpg)

NAB Daily Technical Chart (Source: Thomson Reuters)

Commonwealth Bank of Australia

.png)

CBA Details

Settlement of GST Issues: Commonwealth Bank of Australia (ASX: CBA) happens to be a leading bank of Australia and the market capitalisation of the bank stood at A$146.04 Bn as on 13th January 2020. The bank recently announced that it has ceased to be a substantial holder in Ingenia Communities Holdings Limited, Ingenia Communities Management Trust and Ingenia Communities Fund, on 10th January 2020. The bank together with the Australian Taxation Office has agreed to a settlement to resolve all outstanding Goods and Services Tax (GST) issues. The bank would meet the requirements of updated ATO expectations with respect to the amount of GST credits claimed on costs. The following picture depicts the 2020 financial calendar:

.png)

2020 Financial Calendar (Source: Company Reports)

What to Expect: The bank anticipates its operating context to remain challenging as it adapts to heightened regulatory change, increasing competition, evolving customer preferences, as well as the need to invest in risk and compliance and in technology and innovation. CBA will continue to serve the requirements of its customers and making the necessary changes in order to become a simpler, better bank.

Valuation Methodology: Price to Book Multiple Approach

.png)

Price to Book Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:CBA is well position to navigate the changing landscape on the back of a resilient balance sheet, strong customer base and leading distribution, as well as digital assets. As per ASX, the stock of CBA is trading close to its 52-week high level of $83.990. We have valued the stock using Price to Book based relative valuation method and arrived at a target price, which is reflecting a limited upside at current trading levels (in percentage terms). Hence, we advise investors to closely watch the stock at the current market price of A$82.480 per share, down 0.024% on 13th January 2020.

.jpg)

CBA Daily Technical Chart (Source: Thomson Reuters)

Transurban Group

.png)

TCL Details

Distribution for the Six Months Ended 31 December 2019: Transurban Group (ASX: TCL) is an owner, operator and developer of the electronic toll road and intelligent transport systems. The market capitalisation of the company stood at A$42.12 Bn as on 13th January 2020. The company recently announced that Hills M2 Motorway (100% owned by TCL) has successfully raised A$403 million of non-recourse debt through a new bank facility with a tenor of 12 months. The proceeds raised from the new bank facility would principally be utlilised by Hills M2 for refinancing an existing bank facility maturing in March 2020.

For the six months ended 31st December 2019, the company declared a distribution of 31.0 cents per stapled security. This distribution comprises 29.0 cent distribution from Transurban Holding Trust and controlled entities and a 2.0 cent fully franked dividend from Transurban Holdings Limited and controlled entities. The following picture provides an overview of EBITDA margins for FY 2019:

.png)

EBITDA Margins (Source: Company Reports)

Reiterated Distribution Guidance: The Board of the company has reaffirmed the guidance in relation to the distributions to total 62.0 cents in FY20, which includes the distribution of 31.0 cents for the six months ending 31 December 2019.

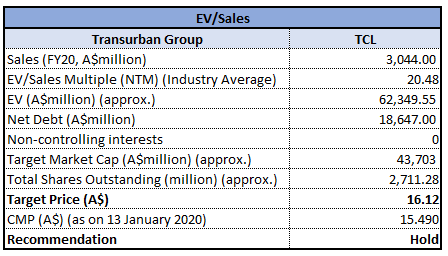

Valuation Methodology: EV/Sales Multiple Approach

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months.

Stock Recommendation: During the September 2019 quarter, the company experienced a rise of 1.8% in average daily traffic with growth achieved throughout all markets. The company added that the development activities across its markets will continue to progress, with three additional projects on track to open by the end of 2020. We have valued the stock using EV/ Sales multiple approach and arrived at a target price, which is offering an upside of lower single digit (in percentage terms). The stock of TCL provided returns of 30.15% in one year and 3.42% on a YTD basis. Therefore, considering the decent performance in Q1FY20, favorable valuations and returns in the past period, we give a “Hold” recommendation on the stock at the current market price of A$15.490 per share, up 0.519% on 13th January 2020.

TCL Daily Technical Chart (Source: Thomson Reuters)

Alumina Limited

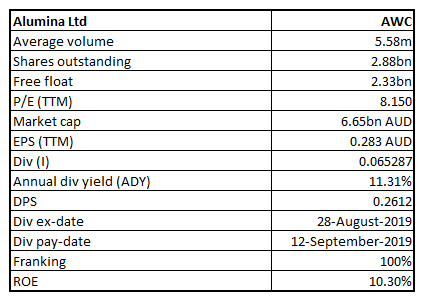

AWC Details

A Look at Q3 FY19 Performance:Alumina Limited (ASX: AWC) possesses a joint venture interest in bauxite mining, alumina refining and aluminium smelting through its 40% interest in the series of operating entities of Alcoa World Alumina and Chemicals or AWAC. The market capitalisation of the company stood at A$6.65 Bn as on 13th January 2020. The company recently announced that the Vanguard Group Inc and its controlled entities have become an initial substantial holder in the company on 23rd December 2019 with the voting power of 5.001%. During the quarter ended 30 September 2019, Alumina Limited reported receipts amounting to $101.6 million, up from $72.6 million reported in 2Q 2019.

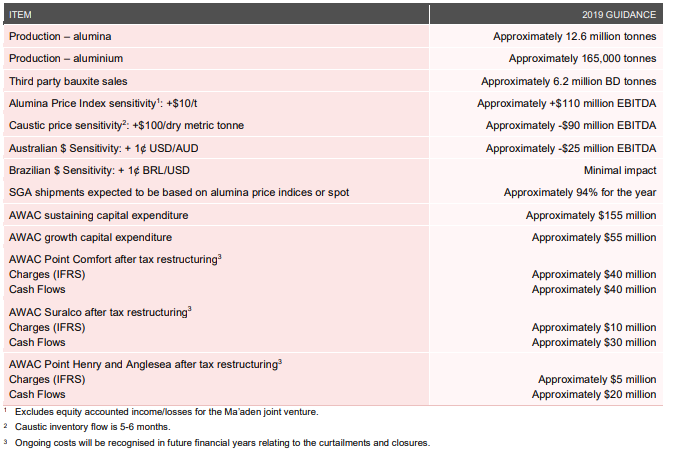

What to Expect: With respect to Bauxite, the company stated that considering the anticipated on-going ample supply of bauxite, mainly from Guinea and Australia and to a lesser extent Indonesia, prices are anticipated to remain under pressure for FY19. The following picture provides an idea of 2019 guidance for AWAC:

AWAC 2019 Guidance (Source: Company Reports)

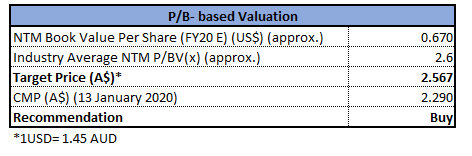

Valuation Methodology: Price to Book Multiple Approach

Price to Book Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:As per a recent presentation at the Melbourne Mining Club, the company notified that the AWAC refineries have reported the lowest CO2e emission intensity in the industry. We have valued the stock using P/E based valuation approach and for the purpose, we have taken the peer group – BHP Group Limited (ASX: BHP), Iluka Resources Limited (ASX: ILU), Northern Star Resources Limited (ASX: NST), etc. Therefore, we have arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Thus, considering the increase in cash receipts, anticipated growth in Bauxite demand from China, valuations, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of A$2.290 per share, down 0.866% on 13th January 2020.

AWC Daily Technical Chart (Source: Thomson Reuters)

G8 Education Limited

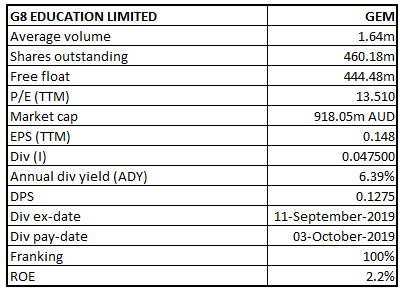

GEM Details

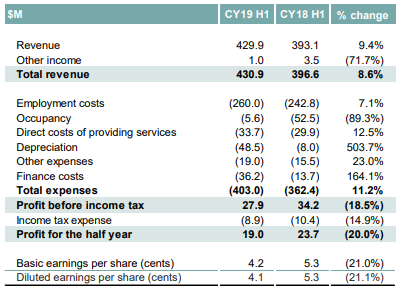

Completion of Sale: G8 Education Limited (ASX: GEM) is engaged in the operation of early education centres owned by the Group. GEM also owns early education centre franchise. The market capitalisation of the company stood at A$918.05 Mn as on 13th January 2020. The company recently announced that it has wrapped up the divestment of 25 centres in Western Australia, which was announced on 14th November 2019. The amount of around $6.4 million raised from the sale would be used for repayment of debt with a view to ultimately recycle proceeds into growth opportunities, as they arise. The following picture provides an idea of statutory results for the half year ended 30th June 2019:

Statutory Results (Source: Company Reports)

Future Guidance: The company expects underlying EBIT in the ambit of $131 million - $134 million for CY19. In addition, the strategy of driving quality, capability and team engagement is on track and generating positive results despite increased supply.

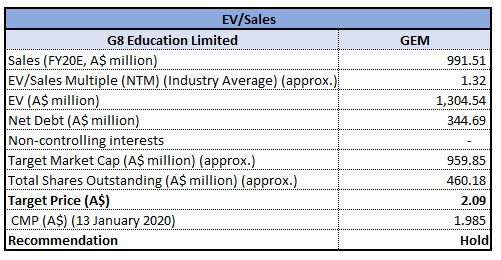

Valuation Methodology: EV/Sales Multiple Approach

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months.

Stock Recommendation: The Board of the company has declared a fully franked dividend amounting to 4.75 cps, reflecting a rise of 0.25% for the half-year ended 30th June 2019. The company experienced improved wage performance during the first half, with further efficiency gains expected in H2. We have valued the stock using EV to Sales based relative valuation method and arrived at a target price, which is offering an upside of lower single digit (in percentage terms). Thus, considering the company’s network growth strategy aimed at growing the centre network, strong cash flow conversion and balance sheet flexibility, we maintain a “Hold” rating on the stock at the current market price of $1.985 per share, down 0.501% on 13th January 2020.

GEM Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...