National Australia Bank Limited

.png)

NAB Details

Capital Raising Worth $1.25 Billion: National Australia Bank Limited (ASX: NAB) provides banking, financial and related services. The market capitalisation of the bank stood at ~$59.48 Bn as on 30th June 2020. The bank has recently issued A$215,000,000 subordinated notes with respect to its US$100,000,000,000 global medium-term note programme. The bank recently became a substantial shareholder of Nine Entertainment Co. Holdings Limited, with a voting power of 5.011%. In another update, the bank announced that it has completed its Share Purchase Plan, raising a total amount of A$1.25 billion. NAB increased the SPP size by A$750 million above its original target of A$500 million, considering the strong support showcased by eligible shareholders.

During 1H FY20, the bank reported sound underlying performance but experienced the impact of COVID-19 on a group level. Cash earnings for the period witnessed a decline of 24.6% against 1H FY19 due to higher credit impairment charges and mark-to-market losses on its high-quality liquid portfolio within markets and treasury. Net Interest Margin for the period declined by 1 basis point to 1.78%. This implies repricing in the home lending portfolio offset by a lower earnings rate on deposits and capital considering the impact of a low-interest-rate environment, together with competitive pressures. The bank is likely to release its Q3 FY20 trading update on 14th August 2020.

Key Financial (Source: Company Reports)

Outlook: The bank is expecting uncertainty in the industry due to the challenges created by COVID-19. However, the bank is undertaking decisive action for further strengthening its balance sheet.

Key Risks: National Australia Bank Limited is exposed to strategic risk, which is associated with the inability of the group to execute its chosen strategy effectively or in a timely manner. Moreover, NAB’s business is sensitive to credit risk, which arises from its lending activities as well as markets and trading activities. Macro-economic and geopolitical risks and financial market conditions, which pose a credit risk may adversely impact the operations of the Group.

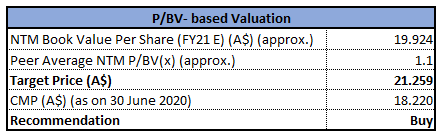

Valuation Methodology: P/BV Multiple Based Relative Valuation (Illustrative)

P/BV Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The bank entered the challenging period caused by COVID-19 in a robust position, with decent capital, funding, and liquidity position. NAB declared a fully franked dividend of 30 cents per share during 1H FY20, which is payable on 3rd July 2020 with a record date of 4th May 2020 and ex-date of 1st May 2020. We have valued the stock using Price to Book Value multiple based illustrative relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). For the purpose, we have taken peers such as Westpac Banking Corp (ASX: WBC), Commonwealth Bank of Australia (ASX: CBA) and Bank of Queensland Ltd (ASX: BOQ). Hence, considering decentcapital, funding and liquidity position, and completion of Share Purchase Plan, we give a “Buy” recommendation on the stock at the current market price of $18.220 per share, up by 0.607% on 30th June 2020.

NAB Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Lendlease Group

LLC Details

Completion of SPP: Lendlease Group (ASX: LLC) is into retail property management, asset management and development of large-scale urban regeneration and greenfield development projects. The market capitalisation of the company stood at ~$8.18 Bn as on 30th June 2020. Recently, the company has finished its security purchase plan and raised $260 million. The company increased the size of the SPP from the original target of $200 million as a result of the high level of demand under the offer. The company raised total equity of $1.21 billion, consisting of $950 million via placement and $260 million from the SPP. These funds allow the company to continue the delivery of its development pipeline and derive benefits out of investment and development opportunities as markets stabilise.

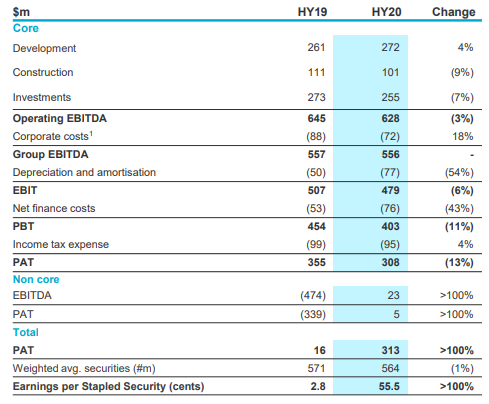

During 1H FY20, the company secured two major urbanisation projects in London and San Francisco Bay Area. The company reported a profit after tax amounting to $313 million and earnings per stapled security stood at 55.5 cents.

Financial Performance (Source: Company Reports)

Near-Term Outlook: The company believes that the near-term outlook for the core business is likely to be supported by the anticipated conversion of commercial and residential development opportunities in its major urbanisation projects.

Key Risks: LLC’s business is sensitive to the failure in execution of strategy or projects, which affects its ability to match its corporate objectives. The company’s business is also sensitive to global and local events or shifts in government policy in the regions in which it operates. These factors may adversely impact its ability to achieve its strategic objectives.

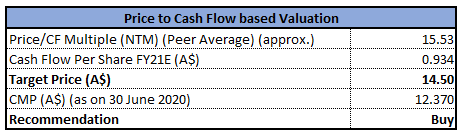

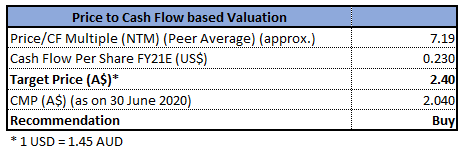

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The core segments of the company are well placed for medium-term success. The development pipeline has increased to $112 billion with a growing number of major urbanisation projects in its international gateway cities across the US and Europe. Debt to equity multiple of the company stood at 0.60x in 1H FY20 as compared to the industry median of 0.94x. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers like Stockland Corporation Ltd (ASX: SGP), Vicinity Centres (ASX: VCX), Mirvac Group (ASX: MGR), etc. Thus, considering the recent capital raising, increased development pipeline and deleveraged balance sheet, we give a “Buy” recommendation on the stock at the current market price of $12.370 per share, up by 4.037% on 30th June 2020.

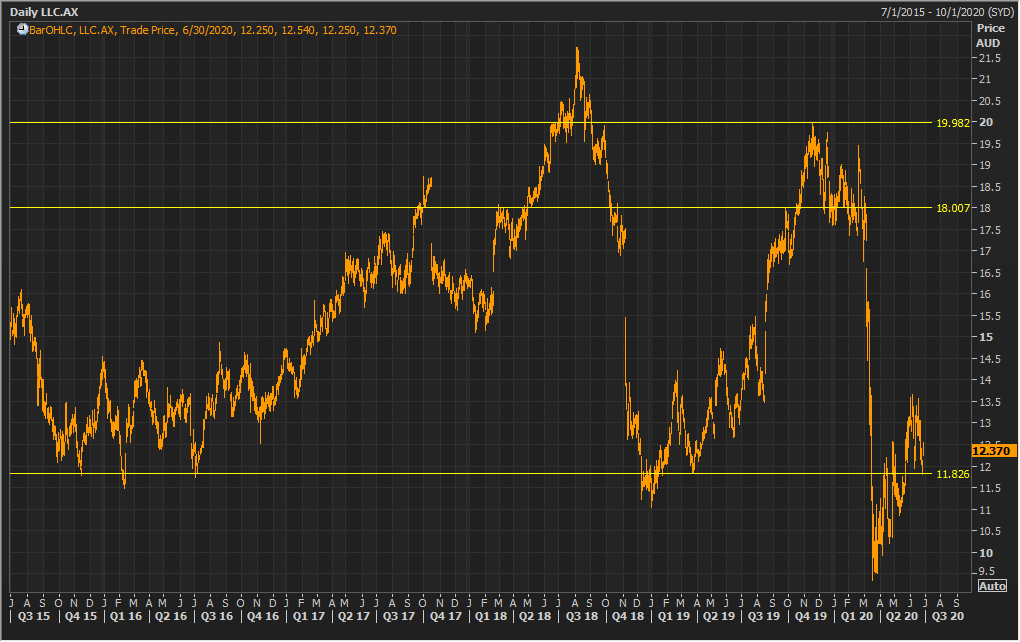

LLC Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

South32 Limited

S32 Details

Maintaining Safe and Reliable Operations: South32 Limited (ASX: S32) is engaged in mining and metal production. The market capitalisation of the company stood at ~$9.57 Bn as on 30th June 2020. The company recently stated that it continues to embed high-quality options with a bias to base metals. In response to COVID-19, the company is maintaining safe and reliable operations by stopping all non-business critical work and maintaining access to critical supplies for its operations. The company added that the production and sales volumes from the Australian operations remain unaffected to date (12th May 2020) by COVID-19 containment measures. Cash from operations has significantly surpassed the capital expenditure during 1H FY20.

Cash Flow (Source: Company Reports)

Production Guidance: For FY20, the company expects production from Worsley Alumina of 3,965kt and from Hillside Aluminium operations, S32 anticipates production of 718kt.

Key Risks: The operations of the company are sensitive to the actions by governments, political events or tax authorities. The company’s business is also exposed to global economic uncertainty and liquidity risk. To manage this risk, S32 is prioritising a strong balance sheet and an investment-grade credit rating, so that it remains in control through economic cycles. The company aims to reshape its portfolio to outperform its peers, which will expose it to the risk of failure in investments made in commodities.

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: Current ratio of the company stood at 2.03x in 1H FY20 as compared to the industry median of 1.81x. This implies that S32 is in a decent position to address its short-term obligations against the broader industry. The stock of S32 is inclined towards its 52-week low level of $1.585, offering a decent opportunity for accumulation. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers like OZ Minerals Ltd (ASX: OZL), Lynas Corporation Ltd (ASX: LYC), etc. Thus, in light of a decent liquidity position, excess cash balance, and guidance, we give a “Buy” recommendation on the stock at the current market price of $2.040 per share, up by 3.291% on 30th June 2020.

S32 Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

OceanaGold Corporation

OGC Details

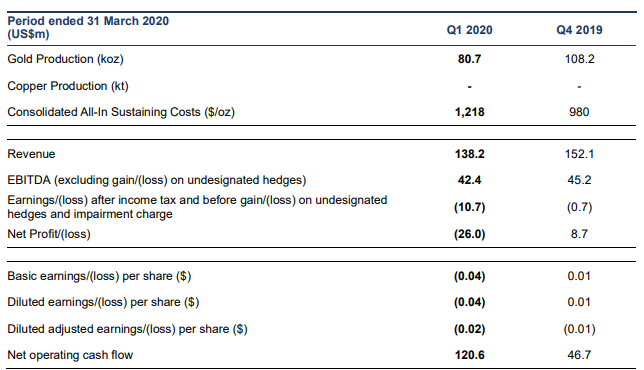

A Look at Q1 FY20 Performance: OceanaGold Corporation (ASX: OGC) is a mid-tier gold mining company with a market capitalisation of $1.93 Bn as on 30th June 2020. During the quarter ended 31st March 2020, the company produced 80,707 ounces of gold, reflecting a decline of 25% due to planned lower production from Haile and Macraes, while Waihi completed mining of Correnso underground in February 2020. Revenue for the quarter stood at US$138.2 million, with Earnings before Interest, Depreciation and Amortisation of US$42.4 million and net loss of US$26.0 million. During the quarter, operating cash flow stood at US$120.6 million with full diluted cash flow per share before working capital of US$0.07 and US$0.19 per share inclusive of the gold presale.

Key Metrics (Source: Company Reports)

Outlook: During 2H FY20, the company expects increased production at lower All-In Sustaining Costs. At Haile, mined and processed grades are likely to increase progressively with two-thirds of Haile’s annual gold output expected in the second half.

Key Risks: As of now, potential risks for the company include repercussions of the suspension of Didipio underground operation, the coronavirus pandemic, and the changes in the market price of gold and copper.

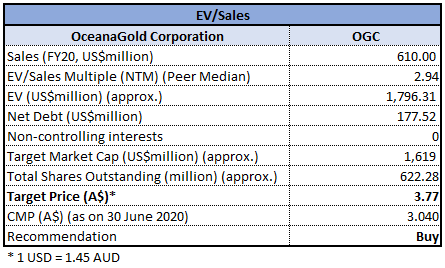

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: During Q1 FY20, the company has undertaken proactive steps to increase cash reserves, including draw down of the remaining US$50 million on the revolving credit facility, US$78.5 million gold presale, and US$22.7 million divestment of a non-core equity position. We have valued the stock using the EV/Sales multiple based illustrative relative valuation method. For the purpose, we have taken peers such as St Barbara Ltd (ASX: SBM), Regis Resources Ltd (ASX: RRL), Resolute Mining Ltd (ASX: RSG), and arrived at a target price of lower double-digit upside (in percentage terms). Thus, considering the performance in Q1 FY20, proactive steps to increase cash reserves, and a modest outlook, we give a “Buy” recommendation on the stock at the current market price of $3.040 per share, down by 1.935% on 30th June 2020.

.png)

OGC Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Coles Group Limited

COL Details

Decent Growth in Sales: Coles Group Limited (ASX: COL) is engaged in the retailing of food, groceries, household goods, liquor, fuel and financial services via stores and online operations. The market capitalisation of the company stood at ~$22.6 Bn as on 30th June 2020. Recently, the company has been notified with a class action proceeding in the Federal Court of Australia in relation to the payment of Coles managers employed in supermarkets. However, the company believes that the class action proceeding is without merit and will defend the proceeding. During Q3 FY20, the company experienced a rise in sales of 12.9% to $9.2 billion. The company added that the Supermarket sales growth was impacted by customer stock piling due to rising concerns relating to COVID-19 in late February 2020. This unprecedented demand led the company to begin placing product limits per customer in certain categories from early March.

Key Sales Metrics (Source: Company Reports)

Outlook: During Q4 FY20, the company expects an elevated cost base because of the additional investment it is making as a result of COVID-19. This investment includes higher remuneration costs due to additional team members in store to ensure a safe environment for customers and team members, investment in cleaning, team member discounts, etc. The company would also continue to review operational and strategic learnings and opportunities.

Key Risks: The company’s business is exposed to the strategic risk created by competition, changing consumer behaviour and digital disruption. To manage this risk, the company is implementing a strategy focused on inspiring customers, smarter selling and winning together. Coles is also exposed to material adverse fluctuations in interest rates, foreign exchange rates and commodity movements, which could impact business profitability.

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: Net margin of the company stood at 2.6% in 1H FY20, which is in line with the industry median. During FY19 and FY18, the company has maintained positive free cash flows, which implies the effective use of working capital. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with an upside of high single-digit (in percentage terms). For the purpose, we have taken peers like Wesfarmers Ltd (ASX: WES), Woolworths Group Ltd (ASX: WOW), Super Retail Group Ltd (ASX: SUL), etc. Therefore, considering the growth in sales during Q3 FY20 and effective use of working capital, we give a “Hold” recommendation on the stock at the current market price of $17.170 per share, up by 1.358% on 30th June 2020.

COL Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...