Stocks’ Details

Magellan Financial Group Limited

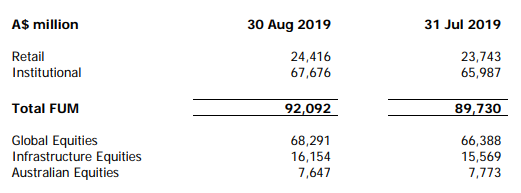

Profit Booking:Magellan Financial Group Limited (ASX: MFG) is into the business of funds management with the objective of offering international investment funds to high net worth and retail investors in ANZ and institutional investors globally. Recently, the company reported total funds under management of A$92,092 Mn as at 30th August 2019 in comparison to A$89,730 Mn as at 31st July 2019. In August 2019, the company experienced net inflows amounting to $315 Mn, which included net retail inflows of $162 Mn and net institutional inflows of $153 Mn.

As per the release dated 14th August 2019, the company announced that it has successfully wrapped up its fully underwritten institutional placement of $275 Mn, which was announced on 13th August 2019. In the same release, it was mentioned that, the company will be issuing 4.98 million new Magellan ordinary shares at a price of $55.20 per new share to institutional investors, which represents a discount of 6.0% to the dividend-adjusted last traded share price of $58.72 on 12 August 2019; and a 4.5% discount to the dividend-adjusted 5-day VWAP of $57.78 on 12 August 2019.

Funds Under Management (Source: Company Reports)

What to Expect:Magellan Financial Group Limited would continue to pursue its financial objectives which are to increase the profitability of the Group over time by increasing the value and performance of funds under management and seeking to grow the value of the group’s investment portfolio.

Stock Recommendation:MFG’s share generated an excellent YTD return of 132.43% and is currently trading slightly towards its 52 weeks high level of $62.60. On the valuation front, it reported a higher price to cashflow and price to book value on TTM basis (Trailing Twelve Months) of 28.4x and 14.6x respectively against the industry median of 12.5x and 1.4x respectively indicating the stock to be overvalued. Currently, it is trading at PE multiple of 25.49x, which is higher than the industry median of 12.2x. We presume that most of the positives are priced in at the current juncture.Hence, considering the aforesaid parameters coupled with stretched valuations and current trading levels, we advise the investors to book the profit at the current level and recommend a “Sell” rating on the stock at the current market price of $54.32 (up 2.704% on 6 September 2019).

Macquarie Group Limited

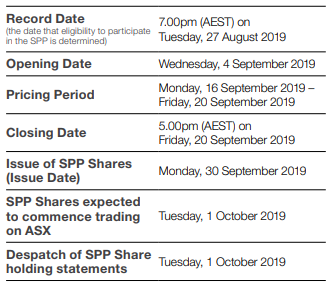

Share Purchase Plan Booklet:Macquarie Group Limited (ASX: MQG) acts as a non-operating holding company for consolidated entity. The activities of a consolidated entity are of the global financial group providing banking, financial, advisory, investment and funds management services. The market capitalisation of MQGstood at ~A$43.68 Bn as on 6th September 2019. The company has recently published its Share Purchase Plan (or SPP) booklet, wherein it was mentioned that the SPP provides shareholders with the opportunity to increase their holding of ordinary fully paid shares in Macquarie at the lower of the issue price paid by institutional investors under the Placement, being $120.00 per share, and a 1% discount to the volume-weighted average price of shares traded during the five ASX trading days immediately prior to and including the Closing Date (20th September 2019).

In another update, MQG stated that it successfully wrapped up the institutional placement amounting to $A1.0 Bn. It added that the Institutional Placement was conducted by the bookbuild method and would result in the issue of around 8.3 Mn fully-paid ordinary shares at a price of $A120.00 per new share, which represents a discount of 2.8% to the last closing price of $A123.51 on 27th August 2019 and 2.8% discount to the 5-day VWAP of $A123.46.

Key Dates (Source: Company Reports)

Future Prospects:Macquarie Group Limited remains well-positioned in order to deliver superior performance in the medium-term. It added that Q2 FY20 is anticipated to see an around $A1.6 Bn increase in capital usage throughout annuity-style and markets-facing businesses. The short-term outlook for 1H FY20 and FY20 primarily remains subject to the completion rate of transactions and period end reviews, market conditions as well as the impact of foreign exchange.

Stock Recommendation:On the stock performance front, it produced a negative return of 1.97% in the time period of six months. As per ASX, the stock of MQG is trading closer to its 52-week higher levels and, thus, it can be said that the price might witness some correction moving forward.Hence, we suggest investors to closely watch the stock at the current market price of $127.080, up 1.453 % as on 6 September 2019 and wait for better entry levels.

CSL Limited

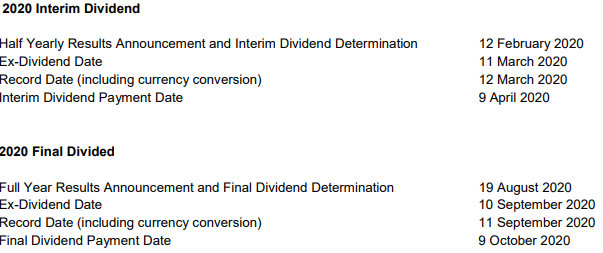

Key Dates for 2020:CSL Limited (ASX: CSL) develops and delivers innovative medicines that save lives and protect public health. It has a market capitalisation of ~A$108.62 Bn as on 6th September 2019. As per the recent release, the company provided key dates for 2020. It will announce its half yearly results and interim dividend determination on 12 February 2020 and full-year results announcement and final dividend determination would be made on 19 August 2020. The company will be conducting its Annual General Meeting 2020 on 14th October 2020.

Key Dates for 2020 (Source: Company Reports)

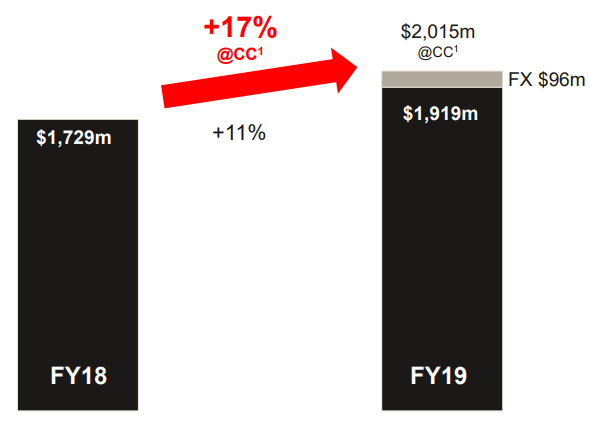

On the financial front, the company’s reported net profit after tax amounted to $1,919 Mn in FY19, reflecting a YoY rise of 17% at constant currency basis and revenue increased by 11% on a constant currency basis, which was mainly because of (1) continued strong growth in immunoglobulin and albumin therapies, (2) high patient demand for specialty products, i.e., Haegarda® & Kcentra®.

Net Profit After Tax (Source: Company Reports)

Future Aspects:For FY20, the company anticipates net profit after tax to be in the ambit of around $2,050 Mn to $2,110 Mn at constant currency basis, which represents growth over FY19 of around 7-10%. The company further added that this growth considers the one-off financial headwind of transitioning to a new model of direct distribution in China.

Stock Recommendation:As per Australian Securities Exchange, the stock of CSL Limited is trading closer to its 52-weeks higher levels. Thus, it looks like there is a probability that the stock price might witness some sort of correction moving forward. The stock has given a decent return of 20.48% and 22.14% in last three months and six months, respectively. Therefore, considering the above-stated facts coupled with decent returns in the recent past and current trading levels, we advise investors to closely watch the stock at the current market price of A$241.990 per share (up 0.976% on 6th September 2019) and wait for better entry levels.

Cooper Energy Limited

New Gas Field Discovery at Annie: Cooper Energy Limited (ASX: COE) is a listed energy company which generates revenue from the discovery, commercialisation and sale of gas to south-east Australia and low-cost Cooper Basin oil production. The market capitalisation of the company stood at ~A$948.61 million as on 6th September 2019. The companyhas announced that the exploration well Annie-1 has made a new gas field discovery in the Otway Basin offshore Victoria. Cooper Energy’s Managing Director David Maxwell described the Annie gas discovery as a solid and promising result from the first well in the program. The Annie gas discovery is the first by an offshore well in the Otway Basin in 11 years, with the most recent being the Netherby gas field in 2008.

Awarded Gippsland Basin Offshore Exploration Permit VIC/P75: COE has announced that it has been awarded the offshore exploration permit VIC/P75 located in the Gippsland Basin, offshore Victoria.The Gippsland Basin is the major gas-producing region in the South-East Australia and presents as a competitive supply source for new developments. VIC/P75 fits well in the portfolio the company has built in the region which includes the recently developed Sole gas field, the Manta Gas and liquids resource. The permit is awarded to Cooper Energy for a six-year term, of which the first three years is a guaranteed work program consisting of seismic reprocessing and geological studies.

VIC/P75 and other Cooper Energy Gippsland Basin permits (Source: Company Reports)

Stock performance: On 6th September 2019, the stock of COE was closed at a price of $0.620 per share. As per ASX, the stock is trading towards its 52-week high of $0.685. In the previous six months, the company has given a total return of 20.39%. The company’s current ratio stood at 3.30x in FY 2019, which is higher than the industry median of 1.25x and, thus, it can be said that the company is in a better position to meet its short-term obligations. Additionally, decent liquidity levels might help the company in making deployments towards strategic business activities moving forward. Hence, considering the above-stated facts, we give a “Hold” rating on the stock at the current price of A$0.620 per share (up 5.983% on 6 September 2019).

Computershare Limited

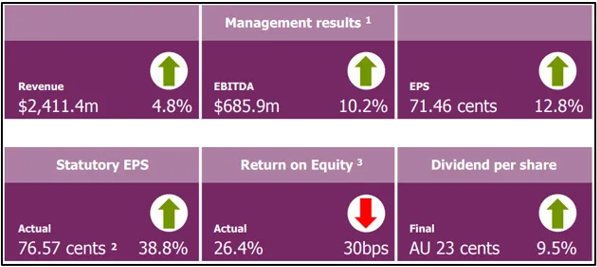

FY19 Financial Highlights: Computershare Limited (ASX: CPU) is a global market leader in transfer agency and share registration, employee equity plans, mortgage servicing, proxy solicitation and stakeholder communications. The market capitalisation of the company stood at A$8.3 billion as on 6th September 2019. The company reported a decent set of numbers for FY19 with revenue up by 4.8% to $2,411.4 million. EBITDA increased by 10.2% to $686 million, aided by improved revenue mix coming from margin income. Depreciation and amortisation rose $5.5 million and $12.2 million respectively, reflecting increased capex and investments in Mortgage Servicing Rights. The following picture is important for the investors as it provides a brief overview of the key numbers:

Key Numbers (Source: Company Reports)

The company has announced an on-market buy-back of ordinary shares of 542,955,868 shares. The reason for the buyback happens to be capital management.

Outlook for FY20:In constant currency, the company expects management EPS to be down by around 5% for FY 2020. The company also expects margin income revenue this year to be like FY19.

Stock performance: As per ASX, the stock is trading towards its 52-week low of 14.180 and, therefore, it can be said that the current trading levels are offering a decent opportunity for accumulation. In the previous six months, the company has given a negative return of 13.32%. As per the ASX, the stock is trading at a P/E multiple of 14.440x. Hence, considering the above-stated facts and current trading levels, we give a “Buy” rating on the stock at the price of A$15.770 per share (up 3.207% on 6th September 2019).

.PNG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...