Janus Henderson Group PLC (ASX: JHG)

Improved Investment Performance: Janus Henderson Group will announce its FY 17 Audited Results on 28 February 2018. Meanwhile, the Adjusted diluted EPS has been reported to be US$2.48 which was up by 28% as compared to prior year. AUM also increased to US$370.8 billion by 16% as compared to prior year and was driven by positive market scenario and FX. Its performance fees for FY 17 was driven by strong performance in UK Absolute Return, segregated mandates and private accounts. During 4Q17, there was a 3% increase in management fees which was driven by higher average AUM. As on 31 December 2017, the total debt which was outstanding declined by 7% due to US$27 million of early conversion notices which were received from holders of 2018 Convertible Senior Notes that were settled in cash for US$42 million. The group will continue to focus on achieving organic growth by being a trusted partner for clients and will deliver first class investment performance. However, the stock looks “Expensive” at the current price of $45.76

.png)

Revenue Analysis (Source: Company Reports)

Carsales.Com Limited (ASX: CAR)

Continued Positive Momentum: Despite releasing a positive result for 2018 first half, Carsales.com’s stock slipped by 1.7% on February 07, 2018 which may be partly owing to group’s performance being below the market’s expectations. The Group delivered growth against prior corresponding period across all the three key financial metrics as revenue was up by 12%, EBITDA was up by 9% and adjusted NPAT was up by 11% as compared to the first half of 2017. The Adjusted EPS was up by 2.4 per share and came to 25.2 cents which was higher by 11% as compared to first half of last year. Interim Dividend for H1FY 18 was 20.5 cents per share which was up by 10% on pcp as H1FY17 interim dividend was 18.7 cents per share. In its last 4 years, the latest result represented the highest adjusted NPAT growth. It continued to expand its domestic core business as operating leverage was achieved and costs were in control. The cash capex also increased by 51% on pcp which was due to the incremental cost for implementing new ERP and CRM systems. Moreover, acquisition of remaining 50.1% of SK Encar also got completed in January 2018 and investment in Soloautos also increased to 100% in December 2017. It anticipates that if market conditions remain stable, the growth rate will continue to increase. However, with a run-up of 42.4% in last one year, the stock looks “Expensive” at the current price of $14.12

.png)

Financial Performance Growth Trend (Source: Company Reports)

Cimic Group Limited (ASX: CIM)

Strong Growth in core businesses: Revenue for FY 17 was $13.4bn which was up by 24% as compared to last year. Profit Before Tax for FY 17 was also up by 30% as compared to prior year while NPAT surged 21%. EBITDA cash conversion of 101% in FY 17 reflected that the group completely focuses on managing working capital and on cash generation. The free operating cash flow for FY 17 also increased by 12% on prior year. Interim ordinary dividend for FY17 was 60 cents per share which was up by 25% on prior year and the final ordinary dividend for FY 17 was 75 cents per share which was up by 21% on prior year. On 31 December 2017, the net cash was $910 m which was up by more than $500m as compared to prior year. In 2017, Moody’s upgraded the group’s rating to Baa2 from Baa3 and S&P rating was also upgraded to BBB from BBB-. Meanwhile, the group released its FY 18 NPAT guidance which will be in the range of $720m-$780m that is up by 3%-11% on prior year but is subject to market conditions. The sound balance sheet provides flexibility to pursue strategic growth opportunities and sustainable shareholders returns. Recently, Group’s contractor CPB was selected by the City of Sydney to design and construct the Gunyama Park Aquatic and Recreation Centre which will be the largest pool complex in Sydney. It is expected that construction will commence in 2018 and will be concluded in late 2019. While the result is encouraging, the stock is trading at a high level and looks “Expensive” at the current price of $46.46

.png)

Highlight of Financial Performance (Source: Company Reports)

Genworth Mortgage Insurance Australia Limited (ASX: GMA)

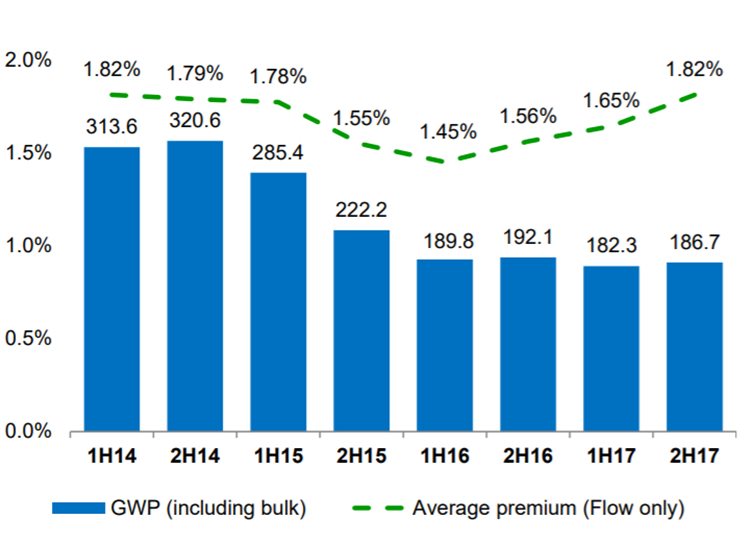

Mixed Performance: Genworth Mortgage Insurance Australia slipped over 2% on February 07, 2018 at the back of a mixed FY17 result. During 2H 2017, the Group undertook an on-shore market share buy-back program under which 17.0 million shares were purchased but were subsequently cancelled for a total consideration of $50.9 million. The Group participated in on-market sale transactions during the buy-back program and maintained approximately 52% stake. The Gross Written Premium decreased by 3.4% in FY 17 as compared to prior year. This decline was partially offset by the impact of the premium rate actions which were taken in 2016 and reflected the changes in the customer portfolio. The insurance margin for FY 17 also showed a dip and were recorded at 40.0% as compared to prior year which was 48.1% in FY 16 and it was driven by unfavourable mark to market movements of the investment portfolio. Group’s capital position was strong as on 31 December 2017 and its regulatory capital solvency level was 1.93 times the Prescribed Capital Amount and 1.74 times the CET1 ratio. Net claims incurred decreased from $158.8 million in FY 16 by $17.0 million in FY 17, and this was primarily driven by a favourable movement in non-reinsurance on paid claims. The Group declared a fully franked final ordinary dividend of 12 cents per share which is payable in March 2018. We maintain a “Hold” on the stock at the current price of $2.74

Gross Written Premium Trend (Source: Company Reports)

Commonwealth Bank of Australia (ASX: CBA)

Drop in cash profit: CBA’s 1H FY18 cash profit of $4.73 billion for continuing operations on underlying operating income of $13.03 billion was down 1.9% against the prior corresponding period. The bank flagged for about $375 million provision in relation to the civil penalty in the AUSTRAC proceedings. Meanwhile, CBA improved its NIM and its APRA capital ratio that jumped up 10.4%. In January 2018, the Group issued USD1.25 billion subordinated notes that constitute Basel III compliant Tier 2 capital. It will add approximately 35 basis points in Tier 2 capital which is over and above the 31 December 2017 reported level. The Group’s CET1 ratio as measured on internationally comparable basis is 16.3% as on 31 December 2017, compared with 15.6% on 30 June 2017 and 15.4% on 31 December 2016. The Group’s spot LCR (Liquidity Coverage Ratio) as at 31 December 2017 was 131% as compared to 135% on 31 December 2016 which is well above the regulatory minimum.Given the challenges faced by the bank in terms of alleged involvement in rate rigging and anti-money laundering act, we maintain an “Expensive” recommendation on the stock at the current price of $76.79

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...