Telstra Corporation Limited

.png)

TLS Details

Decent Progress in T22 Strategy: Telstra Corporation Limited (ASX: TLS) is engaged in the provisioning of telecommunications and information services. The market capitalisation of the company stood at $38.53 billion as on 29th May 2020. Recently, the company announced that it anticipates a non-cash impairment and write down of the carrying value of its 35% stake in Foxtel. TLS expects to recognise an impairment charge amounting to around $300 million against this investment in its FY20 results. This is expected to write down the value of its share in Foxtel from $750 million to around $450 million. During 1H FY20, the company experienced decent progress in its T22 strategy, which is currently in the second year of implementation.

The multi-brand strategy of the company has continued to deliver growth in customer numbers, mainly in the mobile segment. The company added 137,000 retail postpaid mobile services, 135,000 retail prepaid mobile services, and 173,000 pre and postpaid and IoT Wholesale service during the half-year.

.png)

Key Financials 1H FY20 (Source: Company Reports)

Guidance for Year Ahead: For FY20, the company expects total income to be in the range of $25.3 billion to $27.3 billion and underlying EBITDA in the ambit of $7.4 billion to $7.9 billion. The company forecasts free cash flow after operating lease payment in the vicinity of $3.3 billion to $3.8 billion.

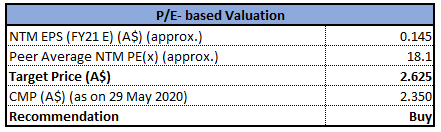

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The company has recently priced €500 million bond issue, which would further cement its balance sheet. TLS would use these proceeds for general corporate purposes which include prefunding of future debt maturities. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of lower double-digit (in percentage terms). Therefore, considering the growth in customer number, decent progress in T22 strategy and recent fund raising from the bond pricing and guidance for FY20, we give a “Buy” recommendation on the stock at the current market price of $3.240 per share on 29th May 2020.

TLS Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

OceanaGold Corporation

.png)

OGC Details

A Quick Look at Q1 FY20: OceanaGold Corporation (ASX: OGC) is a multinational gold mining company having operating assets in Philippines, New Zealand and the USA. The market capitalisation of the company stood at $1.91 Bn as on 29th May 2020. Recently, the company announced that it has scheduled to conduct its Annual General Meeting on 19th June 2020. During Q1 FY20, the company’s gold production stood at 80,707 ounces, reflecting a decline from 108.2 ounces of Q4 FY19, primarily due to lower average grades processed. OGC recorded consolidated AISC of $1,218/oz on sales of 91,388 ounces of gold, indicating an increase from the previous quarter because of the planned lower gold sales, partially offset by lower operating cost. During the same period, the company reported revenue amounting to $138.2 million and EBITDA of $42.4 million.

.png)

Results Q1 FY20 (Source: Company Reports)

Outlook: For FY20, the company forecasts to produce 360,000 to 380,000 ounces of gold on a consolidated basis (excluding Didipio) at an AISC of between $1,075 and $1,125 per ounce sold. During 2H FY20, the company anticipates increased production at lower All-In Sustaining Costs.

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

.png)

EV/Sales Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Operating cash flow for the first quarter amounted to $120.6 million, reflecting a significant rise from the prior quarter because of the inclusion of $78.5 million received for the presale of 48,000 gold ounces scheduled for delivery between September and December 2020. Current ratio of the company stood at 1.17x during March 2020 quarter as compared to the industry median of 0.93x. This implies that the OGC is in a decent position to address its short-term obligations against the peer group.We have valued the stock using an EV to Sales multiple based illustrative relative valuation method, and for the purpose, we have taken peers such as St Barbara Ltd (ASX: SBM), Regis Resources Ltd (ASX: RRL), Resolute Mining Ltd (ASX: RSG), etc., and arrived at a target price with an upside of lower double-digit (in percentage terms). Hence, in light of increased operating cash flow, decent liquidity position, and expected increase in the production, we give a “Buy” recommendation on the stock at the current market price of $3.130 per share, up by 1.954% on 29th May 2020.

OGC Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

BHP Group Limited

.png)

BHP Details

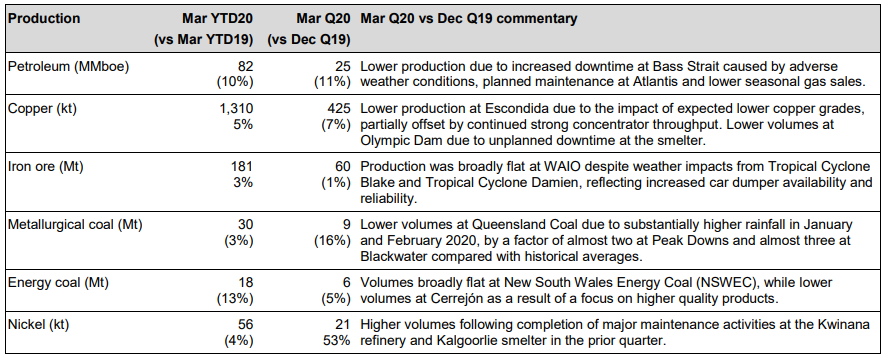

Appointment of Two Directors: BHP Group Limited (ASX: BHP) is involved in the exploration, production, and processing of minerals. The market capitalisation of the company stood at $103.58 Bn as on 29th May 2020. The company recently announced appointments of Dion Weisler and Xiaoqun Clever as independent Non-executive Directors, which will be effective from 1 June 2020 and 1 October 2020, respectively. In response to COVID-19, the priority of the company revolves around safety, health and wellbeing of its workforce and communities, and it has undertaken several measures to reduce the spread of COVID-19. During March 2020 quarter, the company reported Petroleum production of 25MMboe, reflecting a fall of 11% against Dec 2019 quarter because of increased downtime at the Bass Strait caused by negative weather conditions, planned maintenance at Atlantis as well as lower seasonal gas sales.

Production Summary (Source: Company Reports)

Future Aspects: BHP stated that the global economy has been dramatically impacted by COVID-19. Many major economies are likely to contract heavily in the June 2020 quarter, including the United States (US), Europe and India. BHP anticipates petroleum production in the range of 110 MMboe and 116 MMboe for FY20, with volumes expected to be at the bottom of the guidance range.

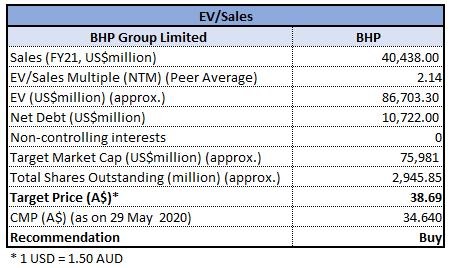

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

EV/Sales Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company possesses a strong financial position. BHP operates a strong business, which is supported by its low-cost operations. The company expects to generate solid cash flow from its strong business. Net margin of the company stood at 23.3% in 1H FY20 against the industry median of 14.3%, reflecting the decent capabilities of BHP to convert its top line into the bottom line as compared to the peer group. We have valued the stock using an EV to Sales multiple based illustrative relative valuation method, and for the purpose, we have taken peers such as Fortescue Metals Group Ltd (ASX: FMG), GR Engineering Services Ltd (ASX: GNG), Rio Tinto Ltd (ASX: RIO) and arrived at a target price with an upside of lower double-digit (in percentage terms). Thus, considering the strong financial position, resilient business, low-cost operations and decent capabilities to convert top-line into the bottom-line, we give a “Buy” recommendation on the stock at the current market price of $34.640 per share, down by 1.479% on 29th May 2020.

.jpg)

BHP Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Mirvac Group

MGR Details

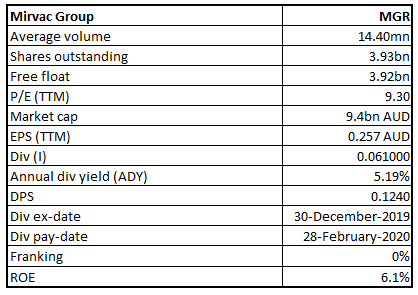

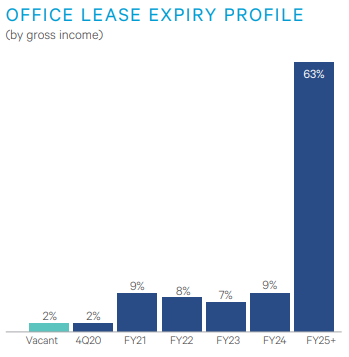

Focus on Construction Momentum: Mirvac Group (ASX: MGR) is in real estate investment, development and investment management. The market capitalisation of the company stood at $9.4 Bn as on 29th May 2020. Since the outbreak of COVID-19, the Office & Industrial division of MGR has focused on working with its commercial and retail tenants to create safe and productive working environments, as well as supporting tenants in need. During Q3 FY20, the occupancy of office division stood at 98.5% with a WALE of 6.6 years. The company is focused on maintaining construction momentum in its portfolio, and fast tracking its $5.4 billion future development pipeline, which is strategically weighted to Sydney fringe and Melbourne.

Office Lease Expiry Profile (Source: Company Reports)

Suspension of Guidance: MGR stated that the COVID-19 pandemic has transformed the world in the space of a few short months and considering uncertainties arising from the pandemic, the company has suspended its earning and distribution guidance for FY20.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: Mirvac entered the COVID-19 pandemic with a strong balance sheet. The gearing of the company stood at 20.8%, and the weighted average debt maturity was 7.7 years as at 31 December 2019. During Q3 FY20, the company bolstered its short-term resilience and maintained its focus on the future. The company continues to work on its development pipeline, exploring a range of additional opportunities and improving its capabilities to expedite the recovery process. Over the span of four years (2016-2019), the company delivered a CAGR of 3.6% in free cash flow. This implies prudent use of working capital over the period. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of lower double-digit (in percentage terms).For the purpose, we have taken peers such as Goodman Group (ASX: GMG), Dexus (ASX: DXS), LendLease Group (ASX: LLC).

Thus, considering the strong balance sheet, focus on maintaining construction momentum in its portfolio and future development pipeline and prudent use of working capital, we give a “Buy” recommendation on the stock at the current market price of $2.350 per share, down by 1.674% on 29May 2020.

MGR Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Sandfire Resources Limited

SFR Details

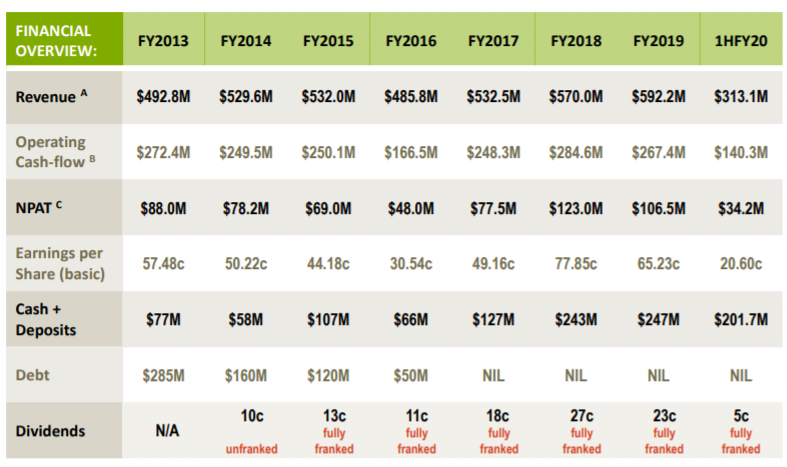

DeGrussa Operations Update: Sandfire Resources Limited (ASX: SFR) is a gold and base metal exploration company with strong history of safe, consistent and profitable production from its flagship high-grade DeGrussa Copper-Gold Operations, located in Western Australia. In a recent business update, the company informed that its operations at DeGrussa are running at full capacity, with strong mine production and milling rates maintained during the first half of the June 2020 Quarter. During the first half of the quarter, the company produced 9,932t of contained copper and 6,500oz of contained gold, taking the Year-to-date production for FY2020 to 62,856t of contained copper and 35,222oz of contained gold.

The company recently released its RRS investor forum presentation in which it highlighted that over the past several year, the company has able to maintain strong and consistent financial performance.

Financial Overview (Source: Company Reports)

What to expect: For the full financial year 2020, the company expects its production for contained copper to be in between 70- 72,000t and contained gold to be in the range of 38-40,000oz at a C1 unit cost of ~$0.90/lb. With strong performance in the first half of the June 2020 Quarter, the company is currently on track for a strong finish to FY2020.

Issue of Ordinary Shares: In a recent update, the company advised that its 22,366 fully paid ordinary shares have been allotted and issued to Kopore Metals Ltd per the terms of the Share Sale Agreement for the acquisition of Kopore’s Namibian exploration properties.

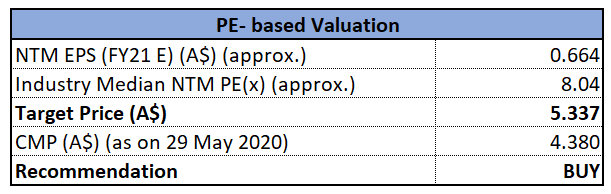

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to earnings Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation. The company current has a strong balance sheet with $242 million cash at 31 March 2020 and no debt. Over the last six months, the stock of SFR has declined by 20.39% on ASX, and is inclined towards 52 weeks low price, offering an opportunity for accumulation. We have valued the stock using Price to Earnings based illustrative relative valuation method and have arrived at a target price with lower double-digit upside (in % terms). For the purpose, we have taken peers St Barbara Ltd (ASX: SBM), Resolute Mining Ltd (ASX: RSG) and Dacian Gold Ltd (ASX: DCN). Considering the aforesaid facts, the company’s decent production results, its robust balance sheet and current trading levels, we give a “Buy” recommendation on the stock at the market price of $4.380, down by 2.45% on 29 May 2020.

.jpg)

SFR Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...