NEXTDC Ltd (ASX: NXT)

.JPG)

NXT Details

Momentum expected from new customer contracts:NEXTDC stock has moved up 26.7% this year to date (as at September 11, 2017) while this Data-Centre-as-a-Service (DCaaS) provider had reported FY17 results in line with its guidance (statutory net profit after tax of $23.0 million over FY16 figure of $1.8 million). NXT also increased its senior secured debt facilities from $100 million to $300 million. FY18 outlook includes about 14-25% growth in EBITDA over prior year and as per the expectations. In a recent update, the Board of Asia Pacific Data Centre Group (APDC, which has been approached by NXT for a takeover) has been said to be in discussions with 360 Capital Group on the development of an alternative proposal to acquire APDC securities. The offer constituted a $0.65 capital distribution by APDC and $1.30 cash consideration paid by 360 Capital. APDC is open to 360 Capital for an all-cash, fully-funded takeover bid at a price which exceeds the offer price of $1.87 under the NEXTDC Offer. Otherwise, APDC Board has recommended the security holders to accept the NEXTDC Offer in the absence of a superior proposal.

.png)

FY18 Game Changers (Source: Company Reports)

Positive outcome of the takeover issue and cornerstone customer contracts at the back new Generation 2.0 facilities that include Brisbane 2, Melbourne 2 and Sydney 2, are expected to drive momentum. The stock is already peaking towards its 52-week high levels; and given the prospects, we put a “Hold” at the current price of $ 4.66

.PNG)

NXT Daily Chart (Source: Thomson Reuters)

Australian Finance Group Ltd (ASX: AFG)

.JPG)

AFG Details

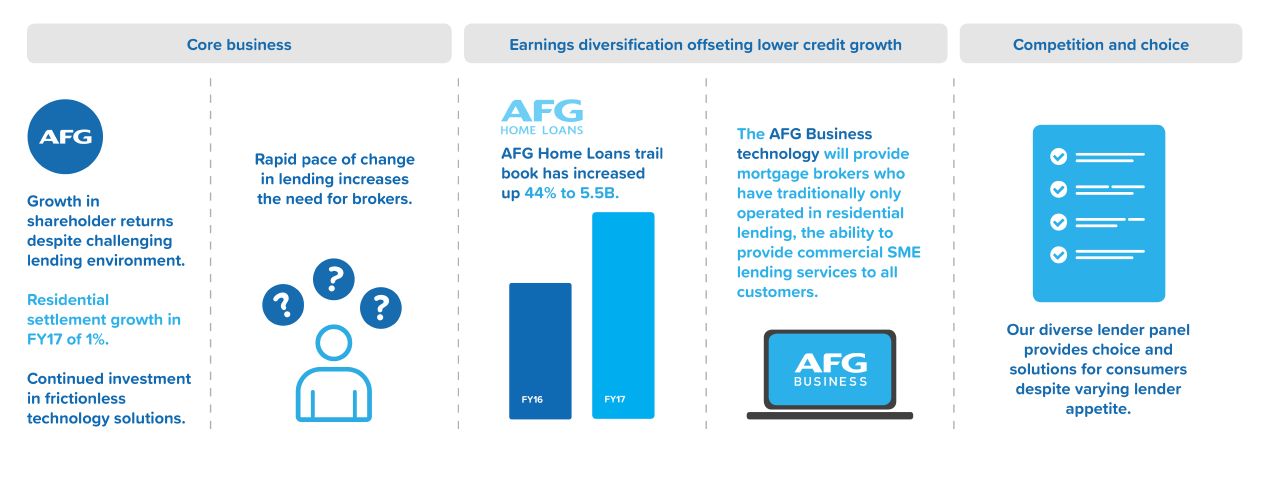

Strategy delivering positive results: Australian Finance Group, Australia’s mortgage broking company, has demonstrated an improved credit growth since Q1 FY17 despite regulatory headwinds; and is expected to witness momentum from a robust suite of branded products, a complex lending environment, recruitment and the AFG Business platform. The group has reported a net profit after tax (NPAT) of $30.2 million for the 2017 financial year, which is ahead of the result forecast as per the profit upgrade provided in June 2017 and represents a 33% growth over FY2016. The NPAT figure excludes the impact of the recognition of AFG Home Loans (AFGHL) white label settlements relating to prior years (normalised NPAT). The group’s core business of residential mortgages, commercial lending, and the continued strong growth in the own-branded AFGHL business, have driven the performance. AFG’s combined residential and commercial loan book of $133 billion has demonstrated a growth of 11% over FY2016, and its strategy to deliver competitive choice to Australian borrowers is working well. Further, the residential loan book of $126 billion is expected to generate ongoing trail commission.

Strategic and Market Outlook (Source: Company Reports)

The Australian lending market is complex and entails an environment of increasing regulatory scrutiny, and this in a way, provides an opportunity for AFG to gain traction with its aggregator platform, new products and repayment options for laying out more choices for the consumers. AFG is also continually providing good value while the external environment with levy on major banks and cuts to broker commissions has been challenging. The group is expected to benefit from its cash position for delivering on strategies. In last three months, the stock has risen 27.5% (as at September 11, 2017) and more upside momentum is expected. We put a “Buy” on the stock at the current price of $ 1.57

AFG Daily Chart (Source: Thomson Reuters)

GetSwift Ltd (ASX: GSW)

.JPG)

GSW Details

Expanding into untapped zones via an exclusive deal:GetSwift stock surged 18.7% on September 12, 2017 as the software-as-a-service solution company inked an exclusive commercial 5-year agreement with N.A. Williams (which is a leading representative group for the North American Automotive Sector in the United States). This deal is expected to raise reoccurring revenues by over $138 million per year once fully captured. The move is said to provide GSW an opportunity to expand into untapped zones. Recently, GSW brought an additional partner, Takeaway.com through subsidiary Vietnammm.com, to its ecosystem, and under its move to expand in Asia. The stock has already surged 478.33% this year to date, as at September 11, 2017. We give a “Hold” at the current price of $ 2.06

.PNG)

GSW Daily Chart (Source: Thomson Reuters)

Aventus Retail Property Fund (ASX: AVN)

AVN Details

Benefitting from leasing spread: Aventus, a fund established to invest in Australian retail property, has retail showrooms in some large format retail centres in Australia. Since IPO, the combination of active portfolio management, value enhancing developments and strategic acquisitions have contributed to a total unitholder return from the fund of 31.9%. The fund has increased its land bank (total site area) to 1.3 million sqm in FY17. Funds from operations’ (FFO) earnings of 17.7 cents per unit (cpu) has also been in line with the guidance of 17.5 cpu. The focus on value adding development projects is expected to drive benefits going forward and these include, redevelopment of the former Bunnings tenancy that is on budget and programmed for completion during the first quarter of FY18, construction of the first child care facility in the portfolio at Cranbourne Home, and 11 planning approvals sought for further expansion in eight AVN centres. Overall, key aspects to note include the fund’s exposure to large format retail assets and leases to a varied range of tenants with structured rental growth. However, headwinds in the retail sector including the ones from Amazon’s entry in Australia appear to be important to keep in mind. Nonetheless, it is expected that the group might be able to mitigate these headwinds given its focus on occupancy, incentives, and leasing spreads. AVN has forecasted its FY18 FFO guidance of 2%–4% higher than FY17 FFO per unit. The group offers an impressive distribution yield and trades at a reasonable level. We give a “Speculative Buy” on the stock at the current price of $ 2.30

.PNG)

AVN Daily Chart (Source: Thomson Reuters)

Bapcor Ltd (ASX: BAP)

.JPG)

BAP Details

Acquisition synergy reaping optimisation benefits:Bapcor, operator in Auto Parts stores across Australia, has recently indicated about the optimisation benefits estimated to be witnessed following the acquisition of Hellaby Holdings. The acquisition synergies are said to provide growth via the adopted strategy. Meanwhile, BAP has also reported for a decent result with revenue of $1,013.6 million up by about 48% and NPAT of $65.8 million from continuing operations, which is up by 50.9%. Increased sales and margin improvement have driven the earnings growth. Burson Trade segment has delivered strong sales and profit growth with total revenue growth of 11.0%. Retail & Service segment recorded an increase in EBITDA of 30.3% while Specialist Wholesale segment (excluding Hellaby) recorded revenue growth of 105.7% and EBITDA growth of 141.1%. Overall, BAP is said to be progressing well on its five-year strategic plan. The group now expects its net profit from continuing operations to be up about 30% in FY 2018. The group plans to provide an insight of its strategy and operations during its annual general meeting on November 02, 2017. Looking at the trading scenario, some of the positives seem to be already considered in the present stock value and the stock appears to trade at a higher level compared to many peers. We give an “Expensive” recommendation at the current price of $ 5.38

.PNG)

BAP Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...