.png)

Stocks’ Details

REA Group Limited

REA Expects a Reduction in Costs: REA Group Ltd (ASX: REA) is involved in offering property and property-related services on mobile applications and websites across Australia and Asia. Recently, the company announced that Owen Wilson had made a change to his holdings in the company by acquiring 8,342 performance rightson 3rd December 2019.

Key Highlights for the Quarter Ended 30 September 2019. The company reported revenue for the quarter at $202.3 million, down 9% year over year. EBITDA from core operations during the quarter came in at $114.9 million, down 14% year over year. Operating expenses for the quarter came in at $87.4 million as compared to $88.8 million reported in the year-ago quarter. Free cash flow for the first quarter stood at $41.8 million, down 20% year over year.

.png)

Q1 Financial Highlights (Source: Company Reports)

What to Expect: The company expects listings for the first half of FY2020 to be lower than pcp, on the back of relatively positive listings environment in 1H FY19, especially in Melbourne and Sydney.

Stock Recommendation: As per ASX, the stock gained ~7% in the past six months. Currently, the stock is trading above the average of its 52-week high and low level of $113.040 and $71.540, respectively. As on 03 January 2020, the company’s market capitalisation stands at ~$13.86 billion, with 131.71 million outstanding shares.FY19 was characterized by strong cost management and efficiencies that resulted in a decline in total operating expenditure. The above factors are likely to support further cost reduction in the coming year. Moreover, performance during the year stood well against the unprecedented market conditions. Given the backdrop of the above factors and current trading levels, we give a “Hold” recommendation on the stock at the current market price of $106.540 per share, up 1.226% on 03 January 2020.

Woolworths Group Limited

Restructuring Plan Approved by Federal Court:Woolworths Group Limited (ASX: WOW) is involved in the business of general retail, food and speciality merchandising via chain store operations. The company operates in Australia and New Zealand, with more than 3,000 stores. On 19 December 2019, the company’s restructuring plan to merge Woolworths Group’s drinks and hospitality businesses received approval from the Federal Court. The joint entity will be known as the Endeavour Group.

Robust Sales Increase in First Quarter ended 06 October 2019: During the quarter, the company reported $10.7 billion Australian Food sales, up 7.8% year over year. The New Zealand Food sales delivered growth of 4.6% year over year. During the quarter, Group Online sales increased by 37.4% and came in at $802 million. Total Group sales from continuing operations stood at $15.9 billion, up 7.1% year over year.

.png)

Q1 Financial Highlights (Source: Company Reports)

Outlook: The company expects sales momentum to continue through FY2020. The company further anticipates prospects to open value for its customers and shareholders in FY2020, despite uncertainty in the consumer environment and input cost pressures.

Valuation Methodology: EV to Sales Multiple Approach

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock gained ~10.2% in the past six months. Currently, the stock is trading above the average of its 52-week high and low level of $40.040 and $28.210, respectively. As on 03 January 2020, the company’s market capitalisation stands at ~$45.76 billion, with 1.26 billion outstanding shares. Its ROE stood at 14.4% in FY19, which is above the industry median of 13.3%. The company’s EBITDA margin and net margins stood at 6.3% and 2.6% in FY19, which is above the industry median of 5.8% and 2%, respectively. The company reported a debt to equity ratio of 0.3x in FY19 as compared to 0.42x in FY18. Based on the current trading position, growth in net margin and valuation, we have valued the stock using EV/Sales Multiple approach and, for the said purposes, we have considered peers like Coles Group Ltd (ASX: COL), Wesfarmers Ltd (ASX: WES) and Metcash Ltd (ASX: MTS). Therefore, we have arrived at a target price of lower single-digit upside (in % terms). Hence, we give a “Hold” rating on the stock at the current price of $36.35 per share, up by 0.193% on 03 January 2020.

CSL Limited

Received FDA Approval for aH5N1c: CSL Limited (ASX: CSL) is engaged in the development, processing and distribution of pharmaceutical and diagnostic products, cell culture media and human plasma fractions. Recently, the company informed about the issuance of 3,059 fully paid ordinary shares under the Performance Rights Plan.

FY19 Financial Highlights for the Period ended 30 June 2019: CSL Limited announced its full-year results, wherein the company reported total revenue on reported basis at US$8,539 million as compared to US$7,915 million in FY18. The company reported NPAT at US$1,919 million as compared to US$1,729 million in the previous financial year. CSL reported GP margin and EBIT margin at 55.9% and 29.3%, respectively, as compared to 55.4% and 30.1% in FY18. The company reported R&D expense at US$832 million as compared to US$702 million in FY18. The business reported FDA acceptance of aH5N1c, world’s first adjuvanted, cell-based pandemic influenza vaccine.

.png)

FY19 Financial Highlights (Source: Company Reports)

Outlook: As per the FY20 guidance, the Management expects a strong demand for plasma and recombinant products followed by slight margin growth from plasma product mix shift, recombinant products growth & conclusion of HELIXATE®. The company also expects Seqirus to perform as per the prior guidance and is likely to benefit from product differentiation and process improvement. FY20 NPAT is expected to be between ~US$2,050 million and ~US$2,110 million on a constant currency basis.

Valuation Methodology: Price to Earnings Multiple Approach

.png)

Price to Earnings Based Valuation (Source: Thomson Reuters), *1 USD = 1.44 AUD

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Recommendation: The stock of CSL is quoting at $277.300, with a market capitalization of ~$124.83 billion. The stock has generated decent returns of 17.21% and 26.16% in the last three months and six months, respectively. At the current market price, the stock is trading at the upper band of its 52-week trading range of $184 and $287.90. The company is likely to invest ~US$1.3 billion for FY20 and expects revenue growth of ~6% on y-o-y basis. Considering the aforesaid facts, we have valued the stock using one relative valuation, i.e., price to earnings multiple and,for the said purposes, we have considered peers like Ramsay Health Care Ltd (ASX: RHC); Cochlear Ltd (ASX: COH); Resmed Inc (ASX: RMD). Therefore, we have arrived at a target price with the downside of lower-double digit (in % terms). Looking at the recent price movement, current trading levels, and valuation, we recommend an ‘Expensive’ rating on the stock at the current market price of $277.300, up 0.822% on 03 January 2020.

OceanaGold Corporation

FY19 Gold Production Anticipated between 460,000 ounces to 480,000 ounces: OceanaGold Corporation (ASX: OGC) operates in development and exploration of gold. Recently, the company informed about the resignation of Dr Nora L. Scheinkestel from the Board of Directors.

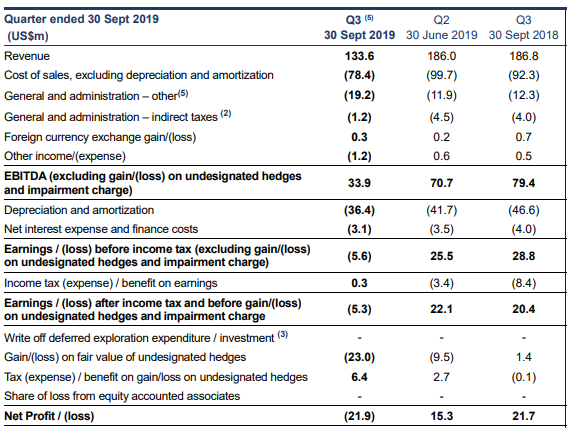

Q3FY19 Operational Highlights for the Period ended 30 September 2019: OGC announced its quarterly results, wherein the company reported revenue of US$133.6 million as compared to US$186.8 million in Q3FY18. The company reported a net loss of US$21.9 million as compared to a profit of US$21.7 million in the previous corresponding quarter. During the quarter, the company reported gold production of 107.5 koz at an AISC of $1,122/oz while gold sales stood at 94.3 koz.During the quarter, EBITDA was impacted by lower sales while Haile delivered operating improvements for the third consecutive quarter.

Q3FY19 Income Statement (Source: Company Reports)

Guidance: As per the FY19 full-year guidance, the company expects gold production in between 460,000 ounces to 480,000 ounces along with 10,000 to 11,000 tonnes of copper. Consolidated AISC is expected in the range of US$1,040 and US$1,090 per ounce sold, while the company upgraded its cash cost guidance to US$710 to US$760 per ounce sold.

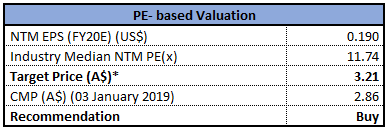

Valuation Methodology: Price to Earnings Multiple Approach

Price to Earnings Based Valuation (Source: Thomson Reuters), *1 USD = 1.44 AUD

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of OGC is quoting at $2.860 with a market capitalization of $1.73 billion. The stock is quoting at the lower band of its 52-week trading range of $2.490 to $5.280. The stock has generated negative returns of 28.90% and 27.23% in the last three months and six months, respectively. The company reported solid exploration results across its business followed by development of Martha UG underway at Waihi. Considering the aforesaid facts, we have valued the stock using Price to Earnings based relative valuation method and, for the said purposes, we have considered peers like St Barbara Ltd (ASX: SBM); Northern Star Resources Ltd (ASX: NST); Resolute Mining Ltd (ASX: RSG); Alacer Gold Corp (ASX: AQG); Gold Road Resources Ltd (ASX: GOR). Therefore, we have arrived at a target price of lower double-digit (in% terms). Looking at the current trading levels, price movement, guidance and business prospect, we recommend a ‘Buy’ rating on the stock at the current market price of $2.860, up 2.878% as on 03 January 2020.

Qantas Airways Limited

Group Unit Revenue Improved 2.1% on y-o-y Basis: Qantas Airways Limited (ASX: QAN) operates in transportation services and engages in the sale of worldwide and domestic holiday tours and associated support activities. Recently, the company informed that the BlackRock Group became a substantial holder with a voting power of 5.02%.

Q1FY20 Operating Highlights for the Period ended 30 September 2019: QAN declared its Q1FY19 quarterly results, wherein the company reported total group revenue at $4.56 billion, up 1.8% in y-o-y basis. The company reported 0.9% y-o-y decline in group domestic unit revenue on account of mixed market conditions. Despite flat demand across corporate travel and slowdown of demand across the small business travel segment, the business reported improved market share in both these segments. The business reported total passengers carried at 14.341 million, up 1.7% on y-o-y basis while revenue seat factor stood at 84.8% as compared to 83.7% in the previous corresponding quarter. The company reported 2.1% improvement on y-o-y basis in Group unit revenue during Q3FY19.

Q1FY20 Operational Highlights (Source: Company Reports)

Guidance: Protests in Hong Kong region are likely to negatively impact the Group’s first half profit performance by ~$25 million. The business’s full-year fuel cost is expected at around $3.98 billion, including a $29 million increase in the first half as compared to the previous corresponding period.

Valuation Methodology: Price to Earnings Multiple Approach

Price to Earnings Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of QAN is quoting at $7.190 with a market capitalization of ~$10.67 billion. The stock has generated positive returns of 11.87% and 31.86% in the last three months and six months, respectively. At the current market price, the stock is quoting at the upper band of its 52-week trading range of $5.185 to $7.460. The business has seen significant upside from competitor capacity contracting more than anticipated, which is expected to continue for the first half of FY20. Considering the aforesaid facts, we have valued the company using one relative valuation method, i.e., price to earnings multiple and arrived at a target price of higher single-digit upside (in % terms). Looking at the aforesaid facts, current trading levels, price movement and business prospects, we recommend a ‘Hold’ rating on the stock at the current market price of $7.190, up 0.419% as on 03 January 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...