.png)

Stocks’ Details

Woodside Petroleum Ltd

Maintaining Debt Portfolio & Strong Cash Flow are Key Catalysts: Woodside Petroleum Ltd (ASX: WPL) is involved in the production, exploration, evaluation and development of hydrocarbon. The company recently announced Lawrence (Larry) Eben Archibald, a Non-Executive Director of the company, has acquired 1,592 ordinary shares at a consideration of $27.83 per share. In another update, WPL stated that UBS Group AG and its related bodies corporate are ceased to be a substantial holder of the company, effective from 26 February 2020.

WPL& BHP Joint Interest Alignment: On 26 February 2020, WPL holding ~73.5% interest and BHP holding 26.5% interest, agreed to affiliate their join interests across the WA-1-R (Scarborough) and WA-62-R (North Scarborough) titles.Both the companies have also agreed to apply for Production Licences in respect of both titles, which is subject to regulatory authorisations.

FY19 Key Highlights: The company has recently released its FY19 results, wherein it reported production of 89.6 MMboe and FY19 net profit after tax of US$343 million. The company exited the year with a cash balance of more than US$4.0 billion and operating cash flow of more thanUS$3.3 billion, demonstrating the strength of its base business and the ability to fund growth. The decent financial performance enabled the Board to declare a full-year total dividend of US$0.91 per share, maintaining a payout of 80% of underlying profit.

.png)

FY19 Key Performance (Source: Company Reports)

Outlook: The company has given production guidance for FY20 to be in the range of 97 –103 MMboe. The company also remains on track to manage its debt portfolio by reducing near-term maturities and maintaining a low cost of debt.It is also predicting to sustain its high cashflow and outstanding margins with low spend in exploration. WPL also expects that the investment expenditure to be in the range of US$4,100 – 4,400 million in FY20.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation

.png)

Price to Earnings Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months, 1USD=1.52 AUD

Stock Recommendation: As per ASX, the stock of WPL is trading close to its 52-week low of $19.50. This offers a decent opportunity for investors to enter the market. During FY19, EBITDA margin of the company stood at 71.8%, higher than the industry median of 31.5%. Considering the returns, current trading levels, higher EBITDA margin and modest outlook, we have valued the stock using Price to Earnings based relative valuation method and arrived at a target price offering an upside of lower double-digit (in percentage terms). For the said purpose, we have considered peers such as Beach Energy Ltd (ASX: BPT), Santos Ltd (ASX: STO), Senex Energy Ltd (ASX: SXY), to name few. Hence, we recommend a “Buy” rating on the stock at the current market price of $21.54, down by 18.347% on 9 March 2020. Fears regarding the coronavirus outbreak have hit worldwide economic development. Additionally, OPEC’s failure to reach a deal with its associates regarding production cuts triggered Saudi Arabia to reduce its price. This caused WPL share price falling in the process.

Oil Search Limited

Exploration & Drilling Update: Oil Search Limited (ASX: OSH) is involved in the exploration, development and production of oil and gas resources. The company recently stated that in February 2020, the Mitquq 1 exploration well was side-tracked to additional assess the Nanushuk reservoir. The report also stated that the exploration of Stirrup 1 well was drilled to a total depth of 4,960 feet.

FY19 Key Highlights: The company’s net profit for FY19 for the period ended 31st December 2019 stood at US$312.4 million, indicating a decline of 8% year over year.This decline is mainly on the back of the fall in worldwide energy prices. During the year, the company declared a total dividend of US 9.5 cents per share. This comprises of interim and final dividend of US 5.0 and US 4.5 cents per share, respectively.

.png)

FY19 Key Metrics (Source: Company Reports)

Outlook: For 2020, the company anticipates production to in the range of 27.5 mmboe to 29.5 mmboe. The company remains on track to develop three-train integrated Papua LNG and P’nyang expansion projects in PNG.

Valuation Methodology: P/CF Multiple Based Relative Valuation

.png)

P/CF Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of OSH is trading close to its 52-week low level of $3.37. Net margin of the company stood at 19.7% in FY19 as compared to the industry median of 12.5%.We have valued the stock using Price to cash flow based-relative valuation approach, and for the purpose, we have taken peers such as Woodside Petroleum Ltd (ASX: WPL), Senex Energy Ltd (ASX: SXY), Origin Energy Ltd (ASX: ORG). to name few, and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Therefore, considering the above factors, we give a “Buy” recommendation on the stock at the current market price of $3.30 per share, down by 35.167% on 9 March 2020, due the failure of OPEC to agree on production cuts on the back of coronavirus outbreak and fears about price war between Saudi Arabia and Russia.

Origin Energy Limited

Sneak Peak in ORG’s 1HFY20 Results: Origin Energy Limited (ASX: ORG) is involved in the production & exploration of natural gas, electricity generation, and sale of liquefied natural gas. ORG has released its interim results for the period ending 31 December 2019, wherein it reported record production of 358 Petajoules in integrated gas with unit production costs of $3.5/gigajoule, down 13% year over year. In the same time span, the company recorded a free cash flow of $680 million, a growth of 22% year over year and reported a statutory profit of $599 million. Owing to its decent financial and operational performance, Origin Energy Limited declared a fully franked interim dividend of 15 cents per share, as compared to 10 cents in HY2019.

.png)

APLNG production (Source: Company Reports)

Future Expectations: Asia Pacific LNG is targeting improved production at the upper end of the guidance range of 690-710 PJ in FY20 and is anticipating higher cash distributions ranging between $1.1 to $1.3 billion. The company has provided guidance for FY20 and expects EBITDA to be between $1,400 – $1,500 million. The company remains on track to implement its strategy to deliver value in a changing energy market.

Valuation Methodology:P/CF Multiple Based Relative Valuation

.png)

P/CF Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of ORG is inclined towards its 52-week low of $5.685, proffering a decent opportunity for accumulation. During 1H20, net margin of the company witnessed an improvement over the previous half and stood at 8.9%, up from 5.9% in 2H19. Considering the trading levels, improvement in margins and decent growth opportunities, we have valued the stock using a P/CF based relative valuation approach and arrived at a target price of lower double-digit upside (in percentage terms). For the said purpose, we have considered AGL Energy Ltd (ASX: AGL), APA Group (ASX: APA), and Spark Infrastructure Group (ASX: SKI), as peers. Hence, we recommend a “Buy” rating on the stock at the current market price of $5.72, down by 15.758% on 9 March 2020, due to crude oil prices tumbles and the rise of the coronavirus suppresses global economic growth.

Leigh Creek Energy Limited

Interim Results for the Period Ended 31 December 2019: Leigh Creek Energy Limited (ASX: LCK) is engaged in exploring and developing energy and minerals. For 1HFY20, the company’s operating loss declined to $3,193,773, which was mainly due to a decline in depreciation, employee benefits expense and other expenses. The company exited the period with cash and cash equivalents of $3,880,822, with total borrowing amounting to $1,62,877. Net cash provided by operating activities for the period stood at $2,936,461.

.png)

Financial Performance (Source: Company Reports)

What to Expect: LCK is making substantial improvements in securing a strategic and cornerstone partner for Leigh Creek Energy Project (LCEP), which will result in significant shareholder value. Leigh Creek Oil & Gas Pty Ltd and Bridgeport Energy (QLD) Pty Ltd inked a farm-in-agreement for a 20% participating interest in two permits in the Cooper & Eromanga Basins.

Stock Recommendation: As per ASX, the stock of LCK is currently trading close to its 52-week’s low level of $0.095, offering a decent opportunity for accumulation. During 1HFY20, current ratio of the company stood at 4.45x, higher than the industry median of 1.06x. The company also reported a stable balance sheet with Debt/Equity ratio of 0.01x, lower than the industry median of 0.48x. In terms of valuation, Price/Book Value multiple stood at 2.2x, lower than the industry average (Energy) of 6.1x. Thus, considering the returns, current trading levels, stability in financial position, etc., we recommend a “Speculative Buy” rating on the stock at the current market price of $0.115, as on 9 March 2020.

Cooper Energy Limited

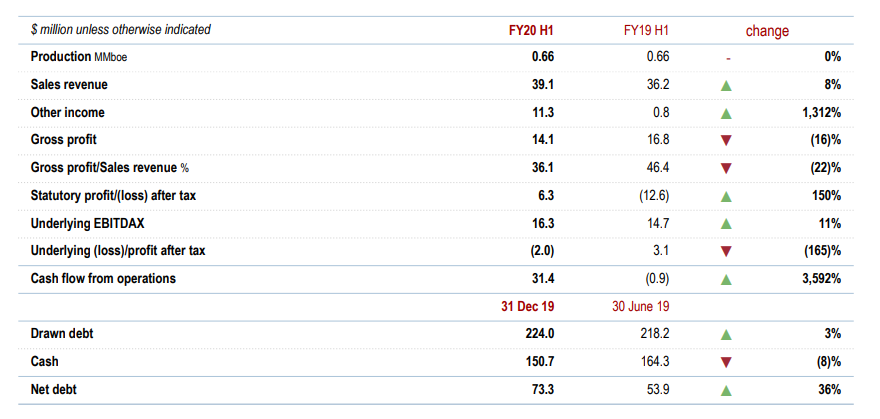

Reported Strong Cash Flow from Operations: Cooper Energy Limited (ASX: COE) is an upstream oil and gas exploration and production company and the key purpose revolves around securing, developing, producing and selling hydrocarbons. The company recently announced that H.E.S.T Australia Ltd, became a substantial holding of the company with a voting power of 5.01%.

1HFY20 Results for the Period Ended 31 December 2019: For the period, the company reported sales revenue of $39.1 million, up by 8% year over year, due to higher gas production and prices. During the same time period, production remained flat year over year to 0.66 million boe. Gross profit for the period stood at $14.1 million, down 16% year over year. Cash inflow from operations stood at $31.4 million as compared to cash outflow from operations of $0.9 million. Net debt amounted to $73.3 million at the end of 31 December 2019, up 36% from 1HFY19.

Financial Performance (Source: Company Reports)

Outlook: For 2HFY20, the company expects existing producing assets unchanged at 1.2 MMBoe. For FY20, the company expects capital expenditure to be in the range of $86 – 93 million (previously $100 – 110 million), due to Lower Otway and Cooper Basin expenditure. COE expects that Minerva Gas Plant would be connected by CY 2021. The company remains on track to manage capital with an aim to offer shareholders with optimal risk-weighted return from the application of the expertise in the exploration, development, production along with sale of the hydrocarbons.

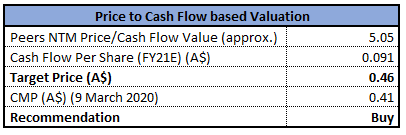

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation

P/CF Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of COE is trading below its 52-week low and high level of $0.395 and $0.685, respectively. The stock has given a negative return of ~24.19% in the past six months. Given the valuation and current trading levels, we have valued the stock using a P/CF based relative valuation method and arrived at a target price of lower double-digit upside (in percentage terms). For the said purpose, we have considered Beach Energy Ltd (ASX: BPT), Senex Energy Ltd (ASX: SXY), Origin Energy Ltd (ASX: ORG), to name few, as peers. Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.41, down by 12.766% on 9 March 2020, due to a fall in crude oil prices and the impact of coronavirus outbreak.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...