Magellan Financial Group

-

Outstanding FY15 Performance: Magellan Financial Group Ltd (ASX: MFG) funds under management (FUM) surged by 55% yoy to $36.4 billion in the fiscal year of 2015, while the net profit soared 110% yoy to $174.3 million. Subsequently, MFG’s diluted earnings per share rose 108% yoy to 101.8 cents per share (cps) and declared a final dividend of 37.8 cps, resulting into a fully franked dividend of 74.9 cps, which is 96% higher against last fiscal year.

.png)

Improving performance over the years (Source: Company Reports)

-

Solid Investment Performance:Magellan Global fund has been demonstrating a solid performance over the years, and delivered 29.5% investment performance for the year ended on June 30, as compared to MSCI world NTR index by 4.9%. Magellan infrastructure fund soared 12.3% during the period against global infrastructure benchmark of 4.8%. Moreover, the group recently launched currency hedged version of ASX quoted Magellan global equities fund (ASX: MGE). MGE was introduced on March 2015, and witnessed an outstanding performance by surging to over $257 Million with over 4450 unit holders as at July 31st, 2015.MFG is also making arrangements with AMP and BT/Westpac.

Dividend Numbers (Source - ASX)

Dividend Numbers (Source - ASX)

-

Stock Outlook: Magellan Financial Group stock delivered a year to returns of 12.9% against the broader index fall by 4.4%. However, the shares have been consolidating over the last three months posting a slight declining by 0.2% impacted by the net institutional outflows in the months of April and June. But, the ongoing FUM growth, solid investment performance and strong FY15 would boost the stock further in the coming months. Based on the foregoing, we give a “BUY” recommendation to the stock at the current levels of $19.01.

MFG Daily Chart (Source - Thomson Reuters)

Insurance Australia Group

MFG Daily Chart (Source - Thomson Reuters)

Insurance Australia Group

-

Berkshire Hathaway Strategic Alliance: Insurance Australia Group Ltd (ASX:IAG)has entered into a strategic relationship with Berkshire Hathaway, with 20% quota share agreement across the group’s insurance business, so that IAG could shield its earnings volatility and capital requirements for the next ten years. IAG intends to maintain its 15% return on equity through this move. Insurance Australia estimates that this quota share arrangement would reduce its capital requirement of over $700 million for the next five years, while $400 million of that benefit estimated to be realized by FY16.

-

IAG Daily Chart (Source - Thomson Reuters)

-

Focus on Asian Pacific markets: The Berkshire agreement would also support the IAG’s focus on Asia pacific markets. Moreover, the group intends to raise its stake in SBI General, the general insurance joint venture with State Bank of India, to 49% from 24% subsequent to the legislative changes on foreign ownership by the end of 2015 fiscal year. IAG acquired PT Asuransi Parolamas, a small general insurance company, to get insurance license in Indonesia. The group recently launched InsureLite, a new solution for families seeking for home insurance affordability stress in Queensland.

-

Stock Performance: Insurance Australia Group shares tumbled over 11.5% in just last five days due to poor fiscal year of 2015 results, wherein Insurance profit reduced to $1.1 billion against $1.6 billion in FY14, while underlying insurance margin reduced to 13.1% in FY15 from 14.2% in pcp. Although, personal Insurance rose 5.2% in GWP, the net natural peril claims costs offset the gain, and surged to $1.05 billion in FY15, which is $348 million more than the allotted allowance of $700 million for the year. On the other hand, management issued a positive outlook for next fiscal year and estimates insurance margin to be in the range of 14% to 16%, including a 2% contribution from the Berkshire Hathaway agreement. IAG is also trading at attractive valuations, with a P/E of 16.9x and has a dividend yield of 5.5%. We remain upbeat on the stock and give a “BUY” recommendation at the current levels of $5.19.

Coca-Cola Amatil

-

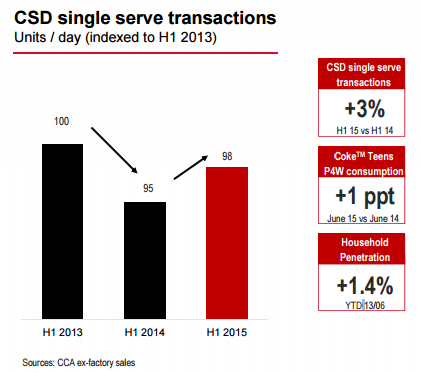

Targets mid-single earnings digit growth: Coca-Cola Amatil Ltd (ASX: CCL)reported a trading revenues growth of 4.9% on a year over year basis to $2.4 billion for the first half of 2015. The group’s Australian business volumes rose driven by its investments on pricing to regain its competition in the market. Net profit rose 2.6% yoy to $187.3 million in 1H15, while the earnings per share (EPS) slightly rose by 0.9% yoy to 24.1 cents per share. The group declared a fully franked interim dividend of 20 cents, representing a payout of 83.0% for the first half of 2015 net profit. Meanwhile, the revenue growth during the period indicates that CCL is on track to achieve mid-single-digit growth in earnings per share for the coming few years. Management also reiterated that Coca-Cola Amatil is also on track to achieve a three year cost savings target of over $100 million. CCL would be using these savings to invest in brand building, revenue management and marketing initiatives.

Improving transactions in Australia (Source: Company Reports)

-

Scaling up to tap the Indonesia market: CCL has been aggressively investing in Indonesia market to tap the rising consumer purchasing power. Although, first half growth was slower than estimated, CCL has been positioning itself by offering broader range of products. TCCC (The Coca Cola Company- parent of CCL) infused USD 500 million into the Indonesia market by acquiring a 29.4% equity interest in CCA Indonesia.

Dividend Numbers (Source - ASX)

Dividend Numbers (Source - ASX)

-

Outlook: CCL stock has been correcting since it touched a one year peak price of $11 in the month of April, as investors were concerned if the group would be able to meet its earnings estimates given the tough market conditions, heavy competition and changing consumers’ preferences for healthy beverages. However, the recent first half of 2015 performance offered some respite. CCL has a dividend yield of 4.8%, and delivered a return on average equity of over 15.9%. Moreover, growing Indonesia & Alcoholic business penetration might offer support to the stock in the coming months. Based on the foregoing, we give a “BUY” on CCL at the current price of $8.56.

CCL Daily Chart (Source - Thomson Reuters)

Carsales.Com

CCL Daily Chart (Source - Thomson Reuters)

Carsales.Com

-

Growth across all the Segments: Carsales.Com Ltd (ASX:CAR) witnessed an outstanding revenue growth of 32% to $311.8 million for the fiscal year of 2015, as compared to $235.6 million in fiscal year of 2014. The data & research and International segments revenue rose 14% yoy and 11% yoy respectively. The online advertising revenues, which is the group’s core business improved by 6% yoy to $216.5 million in 2015 financial year. Meanwhile, the firm’s Asia-focused automotive portals, iCar Asia Ltd (ASX: ICQ) delivered an outstanding results, generating 140% jump in revenues for the six months ending June 30 2015.

.png)

International Portfolio (Source: Company Reports)

-

Ongoing focus in international business: CAR is concentrating to developing its international business models in Korea and Brazil, which would improve its earnings in these areas. CAR acquired SoloAutos in Mexico and SK ENCARSALES.COM, as well as purchased a stake in Webmotors, which would contribute to the group’s international performance for themedium to longer term. Moreover, Carsales remains among the most preferred online destination in buying as well as selling cars in Australia. CAR believes that its investments in Stratton, tyresales and Auto Inspect would start delivering in the coming fiscal years

CAR Dividend Numbers (Source - ASX)

CAR Dividend Numbers (Source - ASX)

-

Stock performance: Despite delivering a modest FY15 performance, the shares have been under pressure, posting a decline of over 7.6% in the last four weeks, due to moderate performance of its core online advertising revenues. However, we believe that the recent correction is a perfect opportunity to investors to enter the stock, given its strong growth potential especially from its international markets. The stock is also trading at reasonable valuations and delivered a return on equity of around 49.9%. Having a dividend yield of 3.6%, Investors should not miss this high value growth stock. We give a “BUY” recommendation to the stock at the current price of $9.90.

.png) CAR Daily Chart (Source - Thomson Reuters)

IOOF Holdings

CAR Daily Chart (Source - Thomson Reuters)

IOOF Holdings

-

Fairfax press Accusations: The shares of IOOF Holdings Limited (ASX: IFL) tumbled more than 18% in the last three months, on the back of Fairfaxpress accusations. Moreover Fairfax Media might even pose pressure onthe federal government to conduct a royal commission into the sector. Investors have been selling the stock, as any possible action from Fairfax would lead to action lawsuits as well as huge compensation payments. Additionally, there might be a tighter government regulation.

IFL Dividend Numbers (Source - ASX)

IFL Dividend Numbers (Source - ASX)

-

Decent fourth quarter performance: IOOF saw positive as well as improved flows across all of its operating segments during the fourth quarter of FY15. However, 0.5% decrease on FUMAS against the prior quarter have offset the positive flows. FUMA reached $123.6 billion as at June 2015, while FUMAS stood at $153.1 billion. Organic growth within IOOF platforms delivered a positive net flow of $467 million during the fourth quarter leading o the total net flows to $1.7 billion for FY15, against $1.4 billion in FY14. IOOF’s advice business saw $707 million of net flows and $2.2 billion of net flows for the year, Meanwhile IOOF witnessed over 20% yoy growth in net flows across all of its core platforms

IFL Daily Chart (Source - Thomson Reuters)

IFL Daily Chart (Source - Thomson Reuters)

-

Stock performance: We view the recent sell of as a buying oppurtunity as the the group has been receiving positive net flows over the last ten quarters. We believe that the Fairfax allegation news have already been factored in the stock. IFL has a solid dividend yield of 5.7% and delivered returns on average equity of 12.6%. With the growing savings by people, the group’s products would continue to be in demand. Accordingly, Investors can consider buying IFL at current price of $8.96.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...