.png)

Stocks’ Details

Praemium Limited

Substantial Increase in NPAT: Praemium Limited (ASX: PPS) provides investment platforms, management, administration and CRM solutions in various countries. As on 4 March 2020, the market capitalisation of the company stood at ~$151.1 million. The company has recently released its interim results for the period ending 31 December 2019, wherein it reported an increase of 12% in net revenue to $24.2 million and a growth of 24% in underlying EBITDA of $7 million. This increase was mainly due to record platform gross inflows of $1.9 billion and an increase in VMA portfolios, Smartim model portfolio FUA and WealthCraft seats. The increase in revenue and EBITDA resulted in NPAT of $1.4 million, up by 122% on the prior period.

.png)

Product Revenue and Underlying EBITDA (Source: Company Reports)

What to Expect: The company has a positive outlook and is excited about the predictive capability of insights and its potential to grow and expand. PPS expects the market share of specialist platforms to grow to 12% in 5 years and hence, will deliver on its strategic initiatives.

Valuation Methodology: Price to Cash Flow Multiple Based Valuation

.png)

Price to Cash Flow Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of PPS is trading very close to its 52-weeks’ low level of $0.320, proffering a decent opportunity for accumulation. During 1H20, EBITDA margin of the company stood at 20.8%, and net margin of the company was 6.1%. Considering the trading levels, decent financial performance and modest outlook, we have valued the stock using price to cash flow based relative valuation method and arrived at a target upside of lower double-digit (in percentage terms). For the said purpose, we have considered OneVue Holdings Ltd (ASX: OVH), EQT Holdings Ltd (ASX: EQT) and Hub24 Ltd (ASX: HUB) as peers. Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.345, down by 6.757% on 4 March 2020.

Rhipe Limited

Strong Growth in Sales: rhipe Limited (ASX: RHP) is engaged in sale and support of subscription software licenses. As on 4 March 2020, the market capitalisation of the company stood at ~$259.21 million. During 1H20, gross sales witnessed an increase of 33% on pcp and stood at $152.7 million, resulting in revenue of $26.6 million, up by 24% on 1H19. This was due to demand for public cloud software and infrastructure, particularly Microsoft Azure and Office365. In the same time span, EBITDA of the company was $7 million, up by 53% on YoY basis. The decent financial and operational performance enabled the Board to declare a fully franked interim dividend of 1.2 cents per share, reflecting an increase of 20% on the prior interim dividend.

.png)

Gross Sales (Source: Company Reports)

Growth Opportunities and Future Expectations: The Board of RHP has estimated guidance for operating profit for FY20 to be approximately $16 million. The company is likely to make an additional investment of up to $0.5m in SmartEncrypt, Dynamics & Support as a Service.

Stock Recommendation: As per ASX, the stock of RHP is trading close to its 52-weeks’ low level of $1.610, offering a decent opportunity for the investors to enter the market. During 1H20, gross margin of the company was 94%, higher than the industry median of 74%. In the same time span, net margin of the company stood at 12.2% as compared to the industry median of 7.2%. Considering the current trading levels, higher margins and decent growth opportunities, we recommend a “Speculative Buy” rating on the stock at the current market price of $1.760, down by 4.865% on 4 March 2020.

EML Payments Limited

Record First Half Revenues: EML Payments Limited (ASX: EML) provides prepaid payment services in Australia, Europe and North America. As on 4 March 2020, the market capitalisation of the company stood at ~$1.15 billion. The company has recently released its interim results for the period ending 31 December 2019, wherein it reported an increase of 60% in gross debit volume (GDV) to $6.62 billion and a growth of 25% in revenue to $59.2 million. This was mainly due to GDV growth from existing customers and constant growth driver including salary packaging, global gaming opportunities, prepaid financial services etc. In the same time span, the company reported a growth of 70% in NPATA to $16 million.

1H20 Financial Highlights (Source: Company Reports)

Future Guidance and Expectations: The company has upgraded its guidance for FY20 and expects revenue in the range of $120 million to $129 million with EBITDA ranging in between $39.5 million to $42.5 million. EML also anticipates NPAT in between of $27.5 million to $30.5 million.

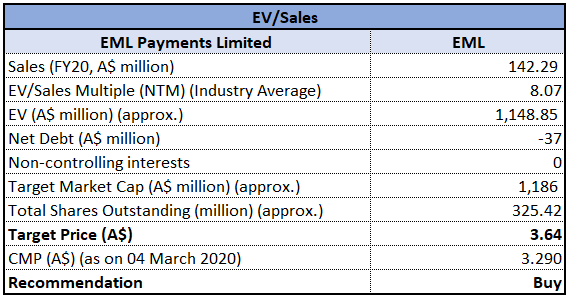

Valuation Methodology: EV/Sales Multiple Based Valuation

EV/Sales Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: During 1H20, gross margin of the company stood at 75.7%, slightly higher than the industry median of 74%. In the same time span, current ratio of the company went up to 1.55x, up from 1.05x in the previous half. This indicates that the company is liquid enough to pay off its current liabilities using its current assets. Considering the improvement in margins, FY20 guidance and decent financial performance, we have valued the stock using EV/Sales multiple based relative valuation and arrived at a target upside of lower double-digit (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $3.290, down by 6.534% on 4 March 2020.

RXP Services Limited

Strong Operating Cash Flow: RXP Services Limited (ASX: RXP) provides digital consulting services. As on 4 March 2020, the market capitalisation of the company stood at ~$65.24 million. The company has released its half-year reports wherein it reported a revenue of $65.1 million, which was largely impacted by deferral of significant government projects and lower sales conversion. In the same time span, the company reported underlying EBITDA of $6.7 million and a strong operating cash flow of $6.7 million. The company has also declared a fully franked interim dividend of 1 cps which is expected to be paid on 10 April 2020.

1H20 Financial and Operational Highlights (Source: Company Reports)

Key Priorities: The company had a tough first half, but the recent wins and pipeline positions the company for a stronger second half with increased revenue and earnings. RXP anticipates delivering an underlying EBITDA which is largely in line with FY19. It is prioritising to strengthen its HCD capabilities in Sydney and enhancing its AI space.

Stock Recommendation: As per ASX, the stock of RXP is trading close to its 52-weeks’ low level of $0.370, proffering a decent opportunity for accumulation. During 1H20, gross margin of the company stood at 93.6%, higher than the industry median of 74%. In the same time span, the company reported a stable balance sheet with Debt/Equity ratio of 0.26x, lower than the industry median of 0.5x. On the TTM basis, the stock is trading at an EV/EBITDA multiple of 4.9x, lower than the industry median (Industrials) of 6.3x. Considering the trading levels, higher gross margin and growth opportunities, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.375, down by 7.407% on 4 March 2020.

Xref Limited

Record First Half Sales and Increase in Revenue: Xref Limited (ASX: XF1) is engaged in the development of human resources technology that automates the candidate reference process for employers. As on 4 March 2020, the market capitalisation of the company stood at ~$38.28 million. During 1H20, the company reported record first-half credit sales of $4.6 million and an increase in revenue by 20% to $3.42 million. This indicates that the company is focusing on growth and is supporting its goal of reaching cash flow break-even by the end of FY20. In the same time span, credit usage was $4.4 million, up by 29% on 1H19 and cash receipts totalled to $6 million.

1H20 Financial Performance (Source: Company Reports)

Growth Opportunities: The company is focused on reaching cash flow break-even by the end of FY20 and is introducing platform and feature updates at a steady rate. The company will continue to expand its growth in international markets both via direct and integration partnerships and is prioritising client adoption and is focusing on expenditure.

Stock Recommendation: As per ASX, the stock of XF1 is trading close to its 52-week low of $0.175, proffering a decent opportunity for the investors to enter the market. Over the span of 4 years from FY15 to FY19, the company witnessed a substantial improvement in EBITDA margin and net margin. On the TTM Basis, the stock is trading at an EV/Sales multiple of 4.3x, lower than the industry average (Industrials) of 30.2x. Considering the current trading levels, improvement in margins and lower EV/Sales multiple, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.210, down by 2.326% on 4 March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...