Macquarie Group Limited (ASX: MQG)

.png)

MQG Details

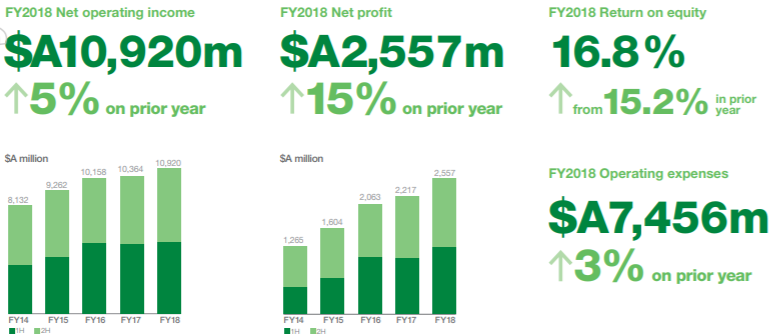

Trading at higher levels: Macquarie Group Limited is listed in Australia and is regulated by the Australian Prudential Regulation Authority (APRA), the Australian banking regulator, as a non-operating holding company of Macquarie Bank Limited (MBL), which is an authorised deposit-taking institution (ADI). For FY18, the Group delivered a record $2.56 billion annual profit, which was up 15% on prior year. Net operating income of $A10,920 million for the year ended 31 March 2018 increased 5% from $A10,364 million in the prior year. Increases in fee and commission income, equity accounted income and reduced charges for provisions were partially offset by impairments and lower investment income. Total operating expenses of $A7,456 million for the year ended 31 March 2018 increased 3% from $A7,260 million in the prior year. Income tax expense for the year ended 31 March 2018 was $A883 million, a 2% increase from $A868 million in the prior year. Net interest and trading income of $A1,182 million for the year ended 31 March 2018 increased 13% from $A1,049 million in the prior year primarily due to a 6% growth in average Australian loan portfolio volumes and a 7% growth in average BFS deposits. Investment income totalled $A1,233 million for the year ended 31 March 2018, a decrease of 13% from $A1,424 million in the prior year.

Overview of Financial Performance (Source: Company Reports)

Full Year Earnings per share ($7.58) was up by 15 per cent as compared to FY17. Net operating lease income of $A929 million for the year ended 31 March 2018 increased 3% from $A904 million in the prior year due to improved underlying income from the Aviation, Energy and Technology portfolios. Net interest and trading income from credit, interest rates and foreign exchange related activities of $A508 million for the year ended 31 March 2018 decreased 18% from $A621 million in the prior year. Revenues were impacted by sustained low volatility and tighter credit spreads in interest rate and credit products. Debt issued at amortised cost of $A53.7 billion at 31 March 2018 increased 6% from $A50.8 billion at 31 March 2017, mainly driven by Treasury’s funding and liquidity management activities which included issuance of long-term debt and US commercial paper. In the past six months, the stock price was up by 8.6 per cent but was followed by a slight dip in the last few days. After the announcement of the FY18 results, the stock edged slightly up on May 04, 2018. Therefore, the stock looks “Expensive” at the current market price of $108.01.

.PNG)

MQG Daily Chart (Source: Thomson Reuters)

Magellan Financial Group Limited (ASX: MFG)

MFG Details

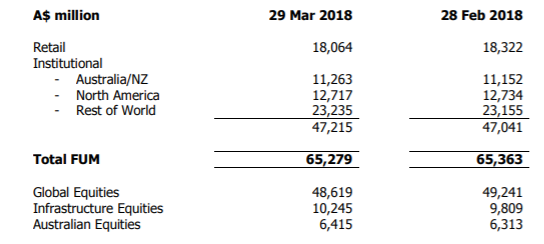

Strategic Acquisitions: In March, Magellan experienced net inflows of $648 million, which included net retail outflows of $20 million and net institutional inflows of $668 million. The Group announced the termination of its three-year partnership with Cricket Australia as the naming rights sponsor of the Australian Men’s Domestic Test Series. The three-year partnership that Magellan signed with Cricket Australia in August 2017, which commenced with the recent Ashes Series, was based on shared values and reputations of integrity, leadership, dedication and an unwavering customer-first culture. A conspiracy by the leadership of the Australian Men’s Test Cricket Team which broke the rules with a clear intention to gain an unfair advantage during the third test in South Africa was against its integrity. Meanwhile, the Group issued 3,856,748 fully paid ordinary shares at a consideration of $27.225 per share and the main purpose of the issue was to raise funds for the acquisition of Airlie Funds Management Pty Limited.

Funds Under Management for March (Source: Company Reports)

Magellan has had an extremely busy and productive first half of FY18 and the Group completed the $1.57 billion of initial public offering of the Magellan Global Trust, the largest closed end fund raising in Australian history and announced two strategic acquisitions; Frontier Partners in the United States and Airlie Funds Management. The interim dividend increased by 16% to 44.5 cents. The Group aims to earn satisfactory returns for its shareholders and the Board has established a pre-tax return hurdle of 10% per annum over the business cycle for the Principal Investments which to date it has achieved. The stock was down by 10 per cent in the last three months, followed by a rise of 3.8 per cent in the last week. By looking at the overall performance, we give a “Buy” recommendation at the current market price of $24.18.

.PNG)

MFG Daily Chart (Source: Thomson Reuters)

WAM Capital Limited (ASX: WAM)

WAM Details

Committed to pay fully franked dividends: WAM Global Limited has exceeded the $16.5 million minimum offer proceeds in its strictly limited $550 million initial public offer capital raising, which opened on 2 May 2018. A $165 million priority allocation, representing 30% of the total proceeds from the offer, is available to the Wilson Asset Management Family which consisted of $150 million priority allocation to shareholders of one or more of WAM Capital, WAM Leaders, WAM Microcap, WAM Research, WAM Active and Century Australia and a $15 million priority allocation to past shareholders of the companies listed.

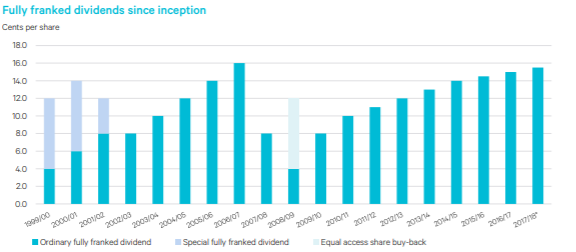

Dividend Trend (Source: Company Reports)

WAM Global will provide shareholders with strong risk-adjusted returns derived from a portfolio of undervalued international growth companies using Wilson Asset Management’s proven investment strategy. The Company intends to undertake a placement of the DRP shortfall at the price of $2.35 per share and issuing new shares at a premium to the Company’s net tangible assets (NTA) will increase the NTA per share to the benefit of all shareholders. The Board announced a fully franked interim dividend of 7.75 cents per share, an increase of 3.3% on the previous year. The dividend reinvestment plan will operate at a 2.5% discount. Domestically, the Royal Commission into financial services continued to cause issues for the major banks, further dragging on the Index. The stock price was down slightly in the last six months while we maintain a “Hold” recommendation at the current market price of $2.38.

.PNG)

WAM Daily Chart (Source: Thomson Reuters)

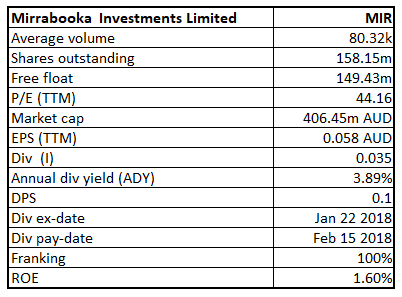

Mirrabooka Investments Limited (ASX: MIR)

MIR Details

Looking for opportunities: Mirrabooka is an investment manager with exposure to mid and small-cap companies. It aims to provide medium to long term investment gains through holding core investments in selected small and medium sized companies (companies which fall outside the S&P/ASX 50 Leaders Index) and to provide attractive dividend returns to shareholders from these investments. The size of the portfolio on 30 April 2018 was $390.6 million with a management cost of 0.62 per cent without any performance fees and whereas on 31 March 2018, the same was $381.3 million. The Group released its financial results for the period ending 31 December 17 and reported a Profit of $5.5 million, representing an increase of 39.8% on the previous corresponding period. This increase was primarily due to the contribution of the trading and option portfolios, which delivered a profit of $2.2 million this half year versus a small loss in the previous corresponding period last year.

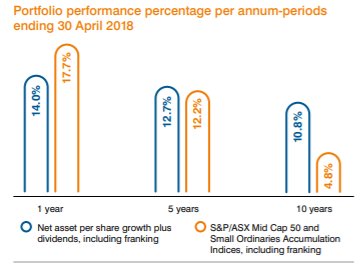

Portfolio Performance as on 30 April 2018 (Source: Company Reports)

Dividends and distributions received decreased by 2.2% but the major difference was the increased contribution from the trading and options portfolios during the half, which showed a combined profit before tax of $2.2 million compared to a loss of $11,000 in the previous corresponding period. Mirrabooka continues to see heightened investment risks from elevated earnings multiples in its market. Its approach will be to continue to focus on long term investments in quality companies with a defendable competitive advantage and to be wary of paying extreme prices. In this context, it will be patient with its cash position which is approximately 10% of the portfolio, awaiting opportunities that future market volatility may provide. The share price declined by 2.28 per cent in the last six months. We give a “Speculative Buy” recommendation at the current market price of $2.58.

MIR Daily Chart (Source: Thomson Reuters)

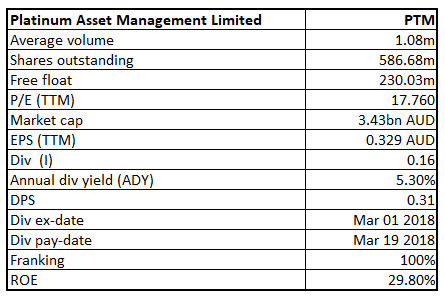

Platinum Asset Management Limited (ASX: PTM)

PTM Details

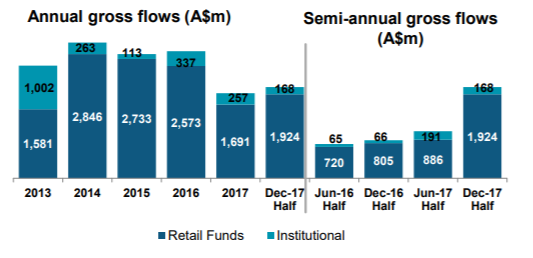

Decrease in net inflows: The Group issued 636,428 Deferred Rights under the Company’s Deferred Bonus Plan (Plan) to receive an equivalent number of the Company’s shares and upon exercise of the Deferred Rights, employees will receive ordinary shares in the Company. Recently, one of its director AJ Loveridge, having a direct interest in the Company acquired 400 ordinary shares from the market and now he holds 22,000 ordinary shares. In March, Platinum experienced net outflows of $150m, with one large client partly reducing their account by $234m, and other net inflows totalling $84m (February 2018: $93m). Further, the funds under management decreased to $27,245.9 m from $27,728.7 m as at February 2018.

Average and Semi-annual gross flow performance (Source: Company Reports)

The Group released its financial results ending on 31 December 17 and observed that Expenses were generally well controlled, with the 14% increase in non-staff costs mostly attributable to product development and marketing related initiatives. New US distribution arrangement was commenced with initial roadshows to prospective US institutional clients scheduled. The business is well placed and has a strong position in Australian retail market and new offshore initiatives provided a platform for growth over the medium term. A small number of large Platinum Trust Fund investors (FuM $1.1b) were elected to switch to a performance fee during the Dec-17 half and no other large-scale switches are anticipated at this time. The share price was declining by 29.4 per cent in the past three months, followed by a rise of 3.5 per cent in the past one week. The stock looks “Expensive” at the current market price of $5.84, given the prevailing softness in funds under management and lack of potential catalysts.

.PNG)

PTM Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...