Boral Limited (ASX: BLD)

.png)

BLD Details

Potential for Growth: Boral Limited reported a 58% increase in net profit after tax before amortisation and significant items, amounting to $237 million for the half year ending December 2017 as compared to corresponding prior period. During October 2017, the Group disposed the Headwaters Energy business for net proceeds of $16.8 million that included $7.6 million which was received on settlement and $9.2 million will be received in annual instalments from October 2018 to October 2021. No gain or loss was generated on the sale of this business. During the period, $32.1 million of cost was incurred on the integration of the Headwater business into the Boral North American business which forms part of the implementation cost of US$90 million-$100 million that is expected to be incurred in financial year 2018-2019. The Group has unrecognised US tax losses of A$62.5 million. The Group issued US$950 million of senior notes pursuant to Rule 144A and Regulation S under the US Securities Act of 1933. US$450 million notes are due in 2022 and US$500 million senior notes are due in 2028. The Board declared an interim dividend of 12.5 cents per share and this will be paid on 9 March 2018.

.png)

External Revenue Share (Source: Company Reports)

It is expected that the Group will exceed its targeted synergies for the full year with US$18 million of synergy benefits banked in the first half and will exceed US$100 million in four years. It is also expected that the Group will deliver a high single-digit EBITDA growth and a low double-digit EBIT growth in FY 18. The total investment for the infrastructure projects slated to be $16 billion by next year, is a good macro move and is expected to help fundamentally strong stocks including Boral. We recommend to “buy” the stock at the current market price of $7.60

.png)

BLD Daily Chart (Source: Thomson Reuters)

Emeco Holdings Limited (ASX: EHL)

.png)

EHL Details

Improvement in Operational and Financial Performance: The group secured the requisite consent of the holders of its 9.250% senior secured notes that are due in 2022 to certain amendments to the indenture governing its Notes. The Group agreed to a condition that all the bank guarantee sub-limits and cash advance will be removed from the limitation on debt facilities. Minor technical changes will be made to ensure proceeds remaining following completion of various cash sweep offers are treated similarly and not subject to any subsequent sweeps. Since Group agreed to the terms of Indenture in 2017, it improved its operational and financial performance and increased its fleet size and saw improvement in market conditions. This resulted in an increase in the Company’s capital expenditure requirements.

.png)

Fleet Utilisation Trend (Source: Company Reports)

It reduced its leverage from 6.7x in FY 16 prior to the issue of the Notes to 2.6x on a pro forma run rate basis. It is expected that the covenant amendments will allow Emeco to maintain and optimise its larger fleet and will allow to take advantage of the market uptick and growth opportunities. The share prices increased by 92.7% in the past six months and by 3.85% in the past one week (as at February 16, 2018). Looking at the improving credit profile, group’s credit rating outlook by Moody’s has been upgraded to stable from positive. We recommend a “Speculative Buy” at the current price of $0.275

EHL Daily Chart (Source: Thomson Reuters)

Big River Industries Limited (ASX: BRI)

.png)

BRI Details

Acquisition for expanding the business: BRI will announce results for the half year ended 31 December 2017 on 27 February 2018. It has completed the earnings accretive acquisition of Ern Smith Timber & Hardware (Ern Smith), located at Hume in the ACT. Ern Smith has been established for some 50 years and complements the Big River expansion strategy to directly supply the Trade segment of the building and construction industry across Australia. Sales revenue of Ern Smith is in the order of $8m and a further growth is expected through the distribution of related Big River products in this market. The consideration for the acquisition includes the issue of 298,883 shares to the vendor which will align interests and will assist with the integration of the business. Its statutory NPAT was up by 22 per cent on forecasted NPAT. Its focus is on balancing manufacturing and imported plywood to maximise profit while lowering operating costs.

.png)

Diversity in terms of Market and Geography (Source: Company Reports)

Working capital performance has been ahead of the target and the net working capital to sales ratio was 15.8% (on rolling 12-month basis). Looking at the overall scenario, the stock looks “Expensive” at the current market price of $2.26, while being worth a watch.

.png)

BRI Daily Chart (Source: Thomson Reuters)

Brambles Limited (ASX: BXB)

.png)

BXB Details

Strong sales revenue momentum: Bramble’s 1H FY18 sale performance was in line with guidance of mid-single digit growth. It achieved a constant-currency growth of 5% that was primarily driven by strong volume growth in North America, Europe and in Latin America and also by ongoing expansion in IFCO RPC businesses.

.png)

Comparative Analysis (Source: Company Reports)

A material increase in cash flow from operations was seen, by US$98.1 million and reflected both an increase in profitability and improved cash flow management. Return on capital invested was 16.2 % which was down by 0.9 pts at constant currency as compared to the same period in the prior year and included all the HFG joint ventures and cessation of contracts for six months. The Board declared an Interim Dividend of AU14.5 cents per share and this was 30% franked and was in line with 2017 full dividend. Sale of CHEP Recycled was also completed on 14 February 2018 and the proceeds were in line with carrying value and the related cash inflow will be reflected in 2H18. It is expected that FY 18 Underlying Profit growth will be impacted by many factors, for instance, US$23 million of FY 17 Underlying Profit will not recur in FY18 due to the loss of a large Australian RPC contract. An increase in Digital Investment is expected and will be in the range of US$15-17 million in FY18. Looking at these details, the stock is “Expensive” at the current market price of $9.74

.png)

BXB Daily Chart (Source: Thomson Reuters)

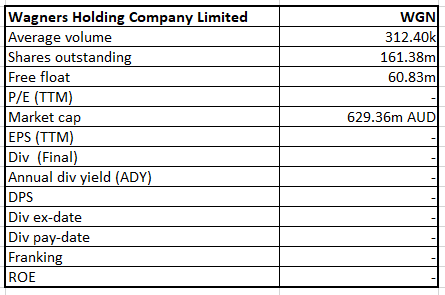

Wagners Holding Company Limited (ASX: WGN)

WGN Details

Funding potential construction: WGN will announce its half-year results on 21 February 2018. Recently Bennelong Funds Management Group Pty Ltd became the substantial holder of WGN by holding 8,114,934 securities with 5.0286% of voting power. The Group was recently covered in media in relation to funding for an airport to service fly in fly out workers who are associated with the Carmichael Coal Mine and this will be a potential construction. The Company confirmed that it has entered into negotiations with the mine owner, Adani. Wagners success has been largely due to the support of its local community and it remains committed to the creation of jobs and economic growth of all regional areas whether through this project or others. While we recommend to wait for the results, we give an “Expensive” recommendation at the current price of $3.88

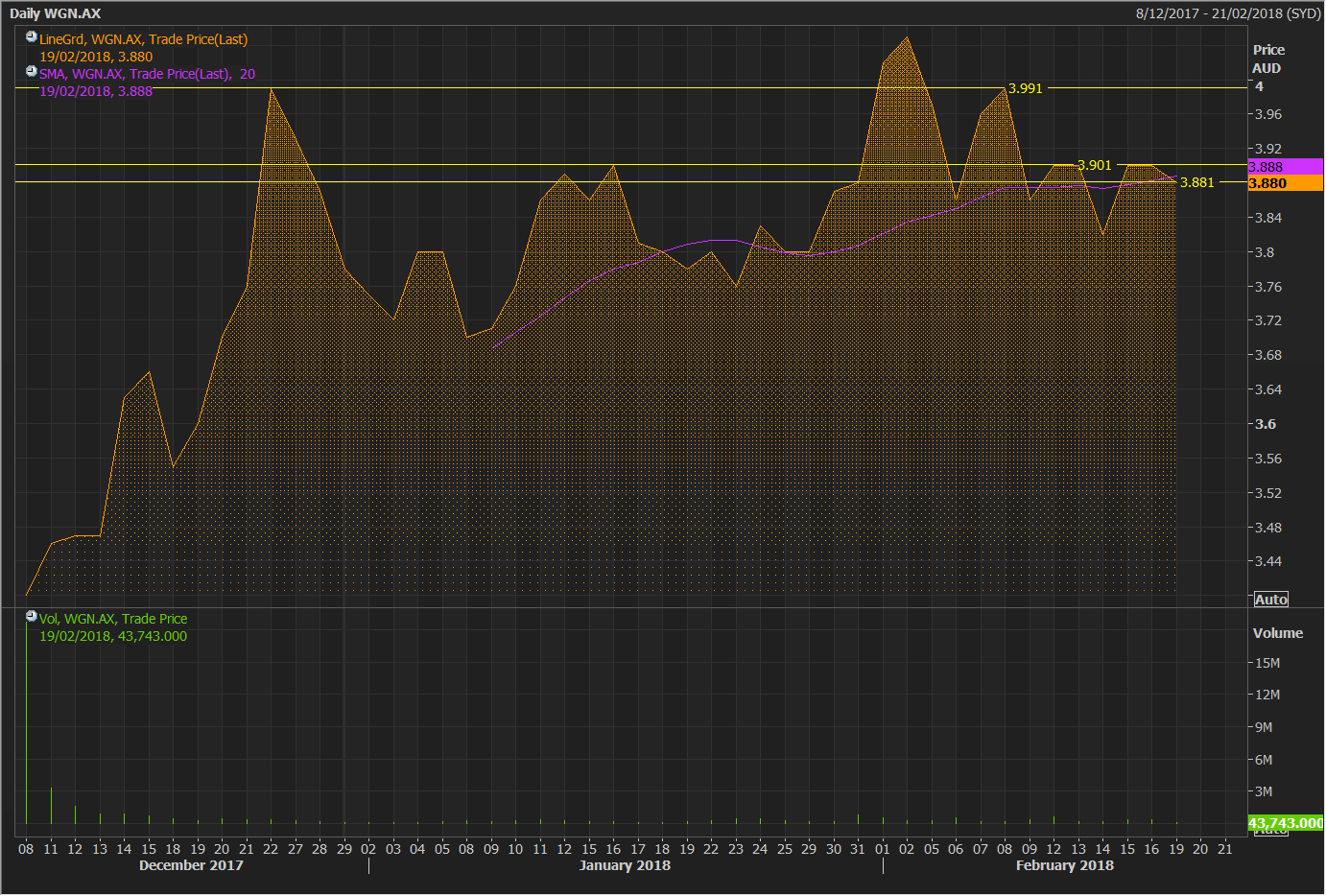

WGN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...