With the market downfall as seen on March 23, 2018 at the back of the US-China trade policies’ issues that have moved the equities across the globe, one sector that witnessed slump apart from mining and banking sectors was the Industrial Sector. The downfall for different stocks in the sector was noted to vary from 1% to about 3% (with S&P AUST ASX200 Industrial Index dipping about 1.53%), while some stocks in the sector still have a long-term potential despite these headwinds.

Transurban Group (ASX: TCL)

.png)

TCL Details

An effective move in alignment to the long-term strategy: Transurban entered into an agreement with Macquarie Infrastructure Partners to acquire 100 per cent of the equity interests in A25, located in the Montreal metropolitan area for a consideration of CAD 840 million and transaction cost will amount to CAD 18 million. It is expected that Transurban will assume responsibility for the management and operations of A25 after the financial close (Q4 FY18) while the transaction is subject to approval from Investment Canada Act.This takeover is in line with Transurban’s strategy that is to focus on heavily congested, urban areas with strong demographics.

.png)

Strategy Highlights (Source: Company Reports)

It will leverage its core capabilities and existing assets in North America. It’s average annual daily traffic growth for FY17 was 4 per cent and EBITDA margins were almost around 70 per cent.The stock prices were down by 4.45 per cent in the past one week and we recommend to “buy” this stock at the current market price of $11.05, given the long-term potential and its capability of being a good defensive stock.

.png)

TCL Daily Chart (Source: Thomson Reuters)

Sydney Airport (ASX: SYD)

.png)

SYD Details

Investing for Growth:The consistent strong growth of international passengers was an important driver for the NSW and for Australian economies; and with respect to tourism, NSW is the second largest exporter and largest employer.Sydney Airport has been playing an important role in driving NSW’s growth. The Group has invested approximately $4.3 billion since 2002 to facilitate the passenger growth and will continue to invest in infrastructure that will deliver efficient capacity, an improved airport experience and customer satisfaction.

.png)

Traffic Performance in February 18 (Source: Company Reports)

In February, its international passenger increase was driven by a 6.4 per cent growth in capacity and by a 0.7 percentage point increase in load factors; whereas, domestic passenger growth of 3.8 per cent was driven by a 0.5 per cent of increase in capacity and by a 2.6 percentage point improvement in load factors as compared to the prior corresponding period.It launched Baidu maps (a popular Chinese mobile navigation service) and hosted a number of exciting in-terminal performances.The prices were down by 8.15 per cent in the past six months but were up by 3.48 per cent in the past one month and the stock still seems to be “Expensive” at the current market price of $6.45, with domestic trend not gearing as per expectations and market dynamics changing a bit at international level.

.png)

SYD Daily Chart (Source: Thomson Reuters)

Downer EDI Limited (ASX: DOW)

.png)

DOW Details

Unfavourable Supreme Court Proceedings: Downer has been recently disappointed by the unfavourable decision received from the New South Wales Supreme Court in respect to a claim that was commenced by the Group against John Holland Pty Ltd and others. Downer’s claim was related to identification of ground subsidence at some locations at Auburn and about appropriate construction and longevity as per contract design of the drainage systemprovided by John Holland Pty Ltd. This is now expected to lead to an impact of $25 million as individual significant item for FY18 based on legal and other costs.

.png)

Half Year Performance (Source: Company Reports)

The Company is currently reviewing the steps required in relation to the Court’s decision. On the other hand, the group was awarded a contract at Blackwater coal mine lately. Given the short comings, the stock was down 5.4% in last three months, as at March 22, 2018. We give an “Expensive” recommendation on the stock at the current price of $6.53

.png)

DOW Daily Chart (Source: Thomson Reuters)

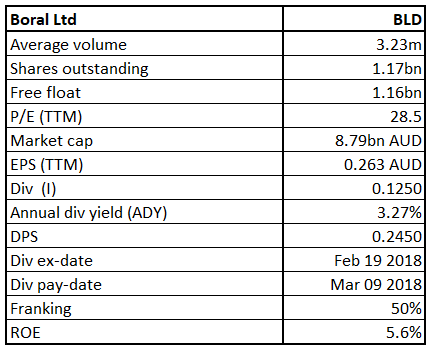

Boral Limited (ASX: BLD)

BLD Details

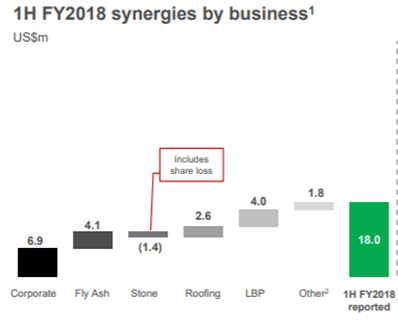

Earnings growth: Boral’s EBITDA (excluding property) was up by 15 per cent for 1HFY18 and was driven by growth in construction material businesses. Revenue was underpinned by continued growth in Sheetrock and by pricing gains and higher on-board revenue. It achieved synergies (from Headwaters acquisition) of about US$18 million at the moment, and expects to exceed synergies of about US$35 million in FY18.On the other hand, the Net Interest Coverage for 1H18 was about 6.3 times which was down from 7.8 times in 1H17.

Synergies Trend (Source: Company Reports)

It is expected that Boral Australia will generate a high-single digit EBITDA growth and a low double-digit EBIT growth in 2018 and group’s dividend pay-out policy will be between 50-70% of its earnings before significant items but will be subject to the Company’s Financial position. The stock performed well so far and was up by 14.7 per cent in the past six months; and given the potential in terms of the infrastructure trends, we maintain a “Buy” recommendation at the current market price of $7.40

.png)

BLD Daily Chart (Source: Thomson Reuters)

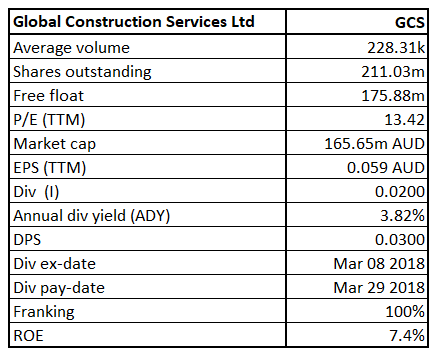

Global Construction Services Limited (ASX: GCS)

GCS Details

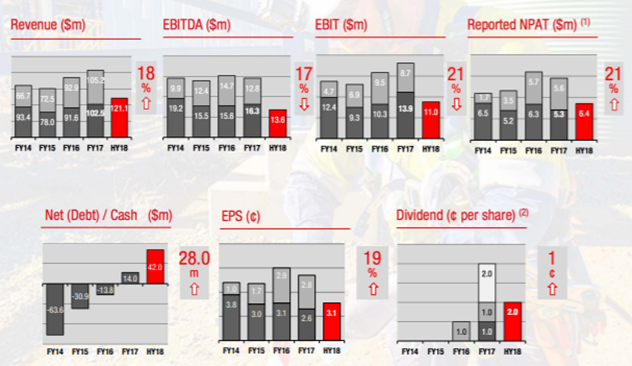

Maintains a strong potential:Down 3.2% on March 23, 2018, the group has been hammered with the overall market downfall. As per the March quarterly rebalance of S&P/ASX Indices, GCS was added to All Ordinaries effective March 19, 2018. Further, Lanyon Asset Management Pty Ltd has a holding of 40,114,938 securities with 19.01 per cent of interest. Meanwhile, Mr Carlo Genovesi announced his retirement from the position of CFO and Mr Nigel Land was appointed in place of Carlo in the month of March 18. Apart from these updates, the group delivered good results for the first half of 2018 and declared a fully franked interim dividend of 2.0 cents per share which will be payable on 29 March 2018.Revenue and reported NPAT were up by 18.1 per cent and by 21.3 per cent and amounted to $121.1 million and $6.4 million, respectively, as compared to corresponding period in the prior year.

Financial Performance for 1H18 (Source: Company Reports)

The strong balance sheet provides flexibility which will produce organic growth, capital management and optimise funding for the acquisition. Further, contribution from East Coast is expected to boost the stock. The stock prices were up by 12.14 per cent in the past six months but were down by 7.7 per cent in the past one week. The stock is a “Speculative Buy” at the current price of $0.76

GCS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...