Ramsay Health Care Limited

.png)

RHC Details

Downgraded FY18 EPS Guidance: Ramsay Health Care Limited (ASX: RHC) is the sixth largest private hospital operator in the world and provides health care services to public and private patients. It serves a range of healthcare needs comprising of day surgery procedures and complex surgeries, psychiatric care and rehabilitation services. It runs around 230 hospitals and day surgery facilities with approximately 25,000 beds across the world. The company posted a decent set of result for the six months to 31 December 2017 wherein the group’s NPAT increased by 7.5% and amounted to $288 Mn in 1HFY18 as compared prior corresponding period (pcp). As a result, EPS grew by 7.8% on pcp basis and stood at 139 cps. Further, the group’s brownfield development programmes are in progress and reflect the high demand for healthcare services. For that, the group has approved $146 Mn capex in the first half of the year. Of which, $57 Mn worth of brownfields have been completed and RHC is set to open $147 Mn worth of developments in the second half FY18 and $156 Mn in the first half of FY19. We expect that the brownfield capacity expansion will drive the top-line growth in the forthcoming years.

.png)

Core NPAT and Core EPS (Source: Company Reports)

In the meantime, the group has reviewed the carrying value of its assets and after looking at the Group’s performance of its UK hospitals in the current challenging environment, it reported its statutory financial statements for the full year and will perceive a charge of £70 Mn (A$125 Mn) net of tax, consisting of an onerous lease provision and asset write-downs related to certain UK sites. Further, the management believes that these provisions and impairments are non-cash in nature and will have no impact on Ramsay’s debt facilities or compliance with its debt facility covenants. Based on the downturn in NHS volumes in Ramsay’s UK business, the group has downgraded its FY18 Core EPS estimate and expects it to be around 7% against the previous guidance of 8% to 10%. While the stock has fallen 23.36 per cent in the past six months and currently trades close to 52-week low level, we maintain our “Hold” recommendation on the stock at the current market price of $ 53.92, considering the aforesaid facts along with short term headwinds related to lower growth rates in procedural work and inpatient admission in Australia operation in the recent months.

.png)

RHC Daily Chart (Source: Thomson Reuters)

CSL Limited

.png)

CSL Details

Decent Outlook: CSL Limited (ASX: CSL) is the blue-chip company with the market capitalization of 89.26 Bn as of July 10, 2018. The company posted reported revenue growth of 11% to $4,147 Mn in 1HFY18 as compared to the prior corresponding period (pcp). NPAT registered growth of 31% YoY on a constant currency basis. As a result, EPS stood at 2.33 cents per share during the first half of the year on the constant currency basis. Based on first half year performance and robust outlook of its product mix portfolio, particularly immunoglobulin products such as Idelvion and Haegarda, the group has lifted its profit guidance for FY18 in the range of US$1,680 Mn and US$1,710 Mn at constant currency basis as compared to the previous guidance which was around $1,550 to $1,600 Mn USD at constant currency basis, representing circa 17% to 20% earnings growth for full year as compared to previous year. RoE and RoIC substantially increased by 1350 bps and 610 bps to 31.0% and 13.5%, respectively in 1HFY18 from the previous six months.

.png)

Strong 1HFY18 Performance (Source: Company Reports)

Meanwhile, the share price was up by 39 per cent in the past six months and by 3.20 per cent in the last one month as at July 09, 2018. It’s now trading at PE of 44.320x, and we maintain our “Expensive” recommendation on the stock at the current market price of $195.860, despite the decent outlook of its product mix portfolio across the market.

.png)

CSL Daily Chart (Source: Thomson Reuters)

Sonic Healthcare Limited

.png)

SHL Details

Synergistic Acquisition of Pathologie Trier: Sonic Healthcare Limited (ASX: SHL) has recently announced the acquisition of Pathologie Trier with the objective of expanding global team including doctors and staff. Pathologie Trier is one of the largest anatomical pathology practices in Germany. It has annual revenue of around Euro 20 Mn and employs ~160 staff, including 24 pathologists. The group operates four laboratories in three West German cities, being Trier, Dusseldorf and Duren, with the latter two laboratories strategically located within large hospital facilities. The initial acquisition price was funded in Euro from its existing debt facilities, while 25 per cent of the total purchase price is subject to a 3-year revenue based earnout provision. The underlying return on invested capital (ROIC) exceeds Sonic’s cost of capital, and the transaction is earnings per share (EPS) accretive by 1% to 1.5%. ROIC and EPS accretion will gradually rise at the back of the deal. On the other hand, the Vanguard group became the substantial holder of SHL since 20 June 2018 by holding 5.004 per cent of the voting power. Moreover, Veritas Asset Management LLP changed its substantial holding from 8.15 per cent to 6.43 per cent since 14 June 2018. Meanwhile,the share price was up by 8.76 per cent in the past three months and by 3.92 per cent in the last one month as at July 09, 2018. The stock price is almost touching the all-time high of $25.770. Hence, we maintain our “Expensive” recommendation on the stock at the current market price of $25.230, considering that the aforesaid catalysts are already factored in the price.

.png)

SHL Daily Chart (Source: Thomson Reuters)

Healthscope Limited

.png)

HSO Details

Increasing diagnostic imaging market – a key driver of Business: Healthscope Limited (ASX: HSO) is a leading private healthcare provider in Australia with 43 hospitals as well as a market leading international pathology operation across New Zealand, Malaysia, Singapore, and Vietnam. The group recorded revenue growth of 4.9% in 1HFY18 as compared to prior corresponding period. However, statutory NPAT from continuing operations was down by 12.8% and amounted to $1,222.2 Mn in 1HFY18 due to completion and maturing brownfield hospital expansions. However, the group expects Hospital Operating EBITDA for FY18 to be between $340 million and $345 million as compared with FY17 Hospital Operating EBITDA of $359.4 million with some softness in demand scenario. Nonetheless, the group is targeting Hospital Operating EBITDA growth of at least 10% in FY19. Currently, the group focuses on to expand its operational capabilities to capitalize on the upcoming opportunities. Hence, we expect that the group may benefit from rapidly growing diagnostic imaging market and increasing elderly population.

.png)

1HFY18 Operating EBITDA Contribution (Source: Company Reports)

On the other hand, The Vanguard group, Inc became the substantial holder of the group since 5 July 2018 by holding 5.008 per cent of the voting power. Meanwhile, HSO stock has risen 16.58% in three months as on July 09, 2018 and trading towards the higher level. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $ 2.210.

.png)

HSO Daily Chart (Source: Thomson Reuters)

Volpara Health Technologies Limited

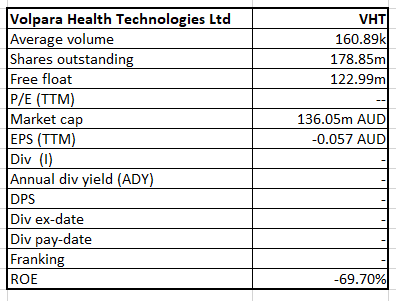

VHT Details

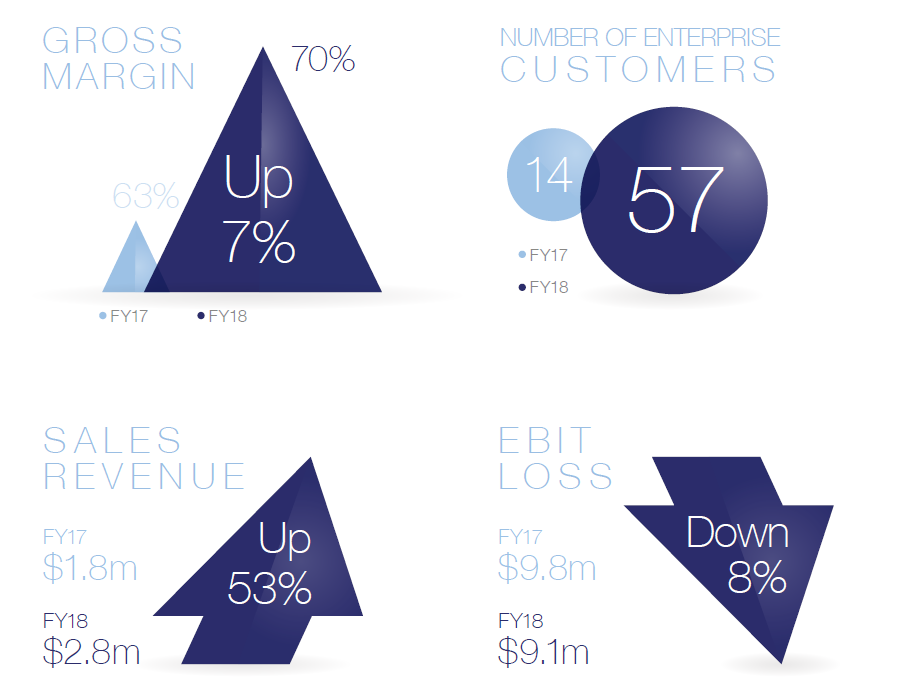

Robust FY18 Performance: Volpara Health Technologies Limited (ASX: VHT) reported its FY18 year to be a very successful year in terms of advancing its mission to help detect breast cancer early and hence increase success rates in dealing with this growing global health problem. During the year, the group recorded Annual Recurring Revenue (ARR) growth of 223% and amounted to $NZ$ 3.6 Mn as compared to previous year. Moreover, total contract value (TCV) exceeded NZ$11.2 Mn, up 173 per cent on the prior period’s NZ$4.1 Mn. Based on solid topline growth, net loss dropped from NZ$9.5Mn to NZ$8.8Mn, a decrease of 8% on YoY basis.

FY18 Highlights (Source: Company Reports)

During the period, the group has expanded its sales team with four members, taking the team to 11, with the desire of growing up to 20 members by the end of March 2019. We expect that these new hires and existing members will generate the leads thus resulting into volume growth of the company.As of now, the stock is trading at a higher level and looks “Expensive” at $ 0.765, and its better if one can wait and watch for further developments.

.png)

VHT Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...