.png)

Stocks’ Details

1300 SMILES Limited

Update on Impact of Coronavirus: 1300 SMILES Limited (ASX: ONT) provides dental surgeries and practice management to self-employed dentists. As on 19 March 2020, the market capitalization of the company stood at $132.36 million. The company has recently stated that it has not been affected by the outbreak of COVID 19 and is taking required measures to protect the public from harm and to improve the quality of health care.

Positive Underlying Results: The company has recently released its interim results for the period ending 31 December 2019, wherein it stated positive underlying results, reflecting the company’s growing business. During 1H20, OTC revenue of the company went up by 7% to $32.1 million, and NPAT witnessed a growth of 6.8% to $4.4 million. The decent financial and operational performance of the company has enabled the Board to declare an interim dividend of 13.25 cents per share which is to be paid on 27 March 2020.

.png)

Half Year Revenue (Source: Company Reports)

What to Expect: The company is expecting continued profitable expansion and is focusing on delivering the best results achievable. It is also aiming to deliver the best returns to shareholders. The company’s mining activity is moving in a positive direction and hence is underpinning the steady growth of operations in several regional centres.

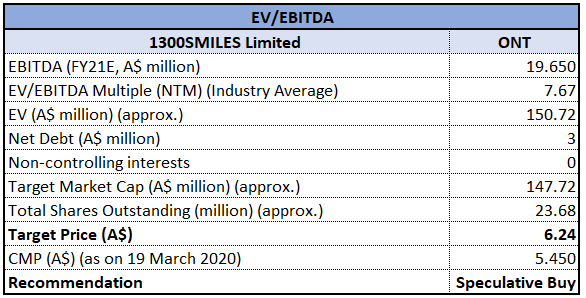

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation

EV/EBITDA Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of ONT is inclined close to its 52-weeks’ low level of $4.8, proffering a decent opportunity for accumulation. During 1H20, gross margin of the company stood at 87.7%, higher than the industry median of 36.7%. In the same time span, EBITDA margin of the company stood at 38.1% as compared to the industry median of 10.8%. Considering the current trading levels, improvement in margins and future expectations, we have valued the stock using EV/EBITDA multiple based relative valuation method and arrived at a target price offering an upside of lower double-digit (in percentage terms). Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $5.450, down by 0.909% on 19 March 2020.

Medical Developments International Limited

COVID-19 Impact on MVP: Medical Developments International Limited (ASX: MVP) is a pharmaceutical drug company which manufactures and distributes pharmaceutical drug and medical and veterinary equipment. As on 19 March 2020, the market capitalization of the company stood at $324.1 million. The company has recently stated that the potential negative impact of the COVID 19 virus on its business appears limited. It has built stock to cater for an anticipated increase in sales throughout CY20 and is avoiding any non-essential travel.

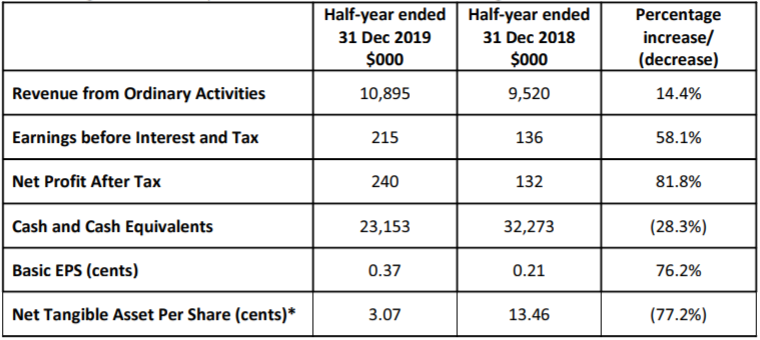

Significant Growth in Revenue and Profit: The company has recently released its half-year results for the period ending 31 December 2019, wherein it reported an increase of 14.4% in revenue to $10.8 million and a growth of 81.8% in net profit after tax of $240k. This resulted in an increase in EPS by 76.2% to 0.37 cents. The decent financial and operational performance of the company enabled the Board to declare a fully franked interim dividend of 2 cents per share which is to be paid on 17 April 2020.

1H20 Financial Highlights (Source: Company Reports)

Future Expectations and Growth Opportunities: The company expects to roll out Penthrox® in remaining European Union countries, Mexico, Iran, Jordan, South Korea and Thailand. Over the next few years, the company will advance its manufacturing processes and is expected to deliver strong growth.

Stock Recommendation: As per ASX, the stock of MVP gave a return of 1.49% in the past six months and is trading very close to its 52-weeks’ low level of $4.070. During 1H20, EBITDA margin and net margin witnessed a YoY improvement and stood at 15.6% and 2.2%, up 14% and 1.4%, respectively from pcp. In the same time span, current ratio of the company stood at 3.74x, higher than the industry median of 1.94x. Considering the returns, current trading levels, improvement in margins and decent outlook, we recommend a “Hold” rating on the stock at the current market price of $4.270, down by 10.482% on 19 March 2020.

Compumedics Limited

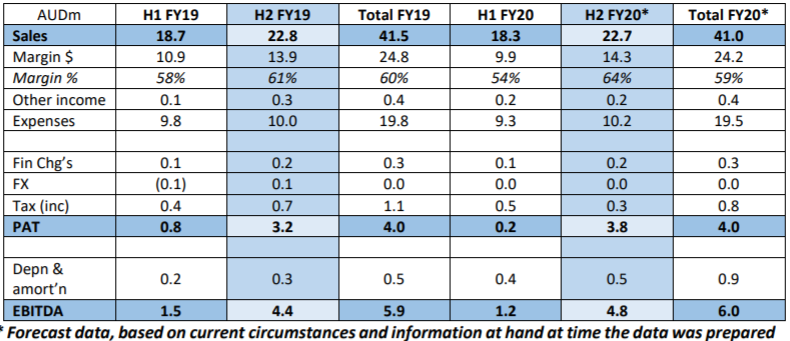

Progress in Technological Opportunities: Compumedics Limited (ASX: CMP) is engaged in the development and commercialization of technology in computer-based patient monitoring and diagnostic systems. As on 19 March 2020, the market capitalization of the company stood at $70.87 million. The company has released its interim results for the period ending 31 December 2019, wherein it reported revenue of $18.3 million, representing a 2% decrease over the pcp of $18.7 million. The shortfall in sales in the US and a decline in gross margin resulted in a slight decline in EBITDA to $1.2 million. However, the company continued to progress in several other technology opportunities and is focusing on several initiatives to underpin both current and future growth.

Growth Opportunities: The company is focused on several initiatives in order to drive future growth. It has rolled out a new product platform which will expand its addressable markets. The company has identified key growth opportunities to deliver an increase in revenues and earnings in the current financial year. CMP expects its full-year sales to be in the range of $40-42 million, EBITDA in between $5.5-6.5 million and NPAT in the range of $4 to $5 million.

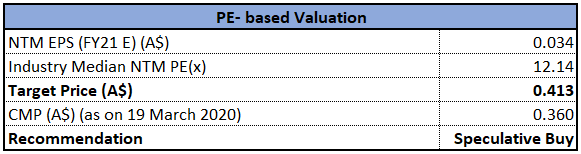

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation

Price to Earnings Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of CMP is inclined close to its 52-weeks’ low level of $0.325, proffering a decent opportunity to enter the market. During 1H20, EBITDA margin witnessed an increase on the previous year and stood at 8.8%, up from 7.6% in 1H19. In the same time span, Debt/Equity ratio of the company stood at 0.14x, lower than the industry median of 0.3x. Considering the trading levels, improvement in EBITDA margin and decent growth opportunities, we have valued the stock using the price to earnings based valuation approach and have arrived at a target price offering an upside of lower double-digit (in percentage terms). Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.36 on 19 March 2020.

OncoSil Medical Ltd

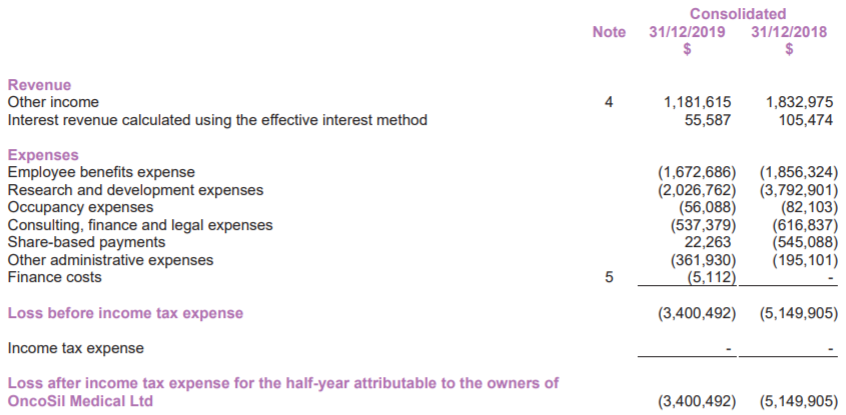

FDA Grants Breakthrough Device Designation: OncoSil Medical Ltd (ASX: OSL) is engaged in the development of its lead product candidate, OncoSilTM localized radiation therapy for the treatment of pancreatic cancer. As on 19 March 2020, the market capitalization of the company stood at $58.03 million. The company has recently announced that OncoSil™ device has been granted Breakthrough Device Designation by the FDA for the treatment of pancreatic cancer along with systemic chemotherapy.

The company has released its interim results for the period ending 31 December 2019, wherein it reported income and interest revenue of $1.23 million and cash equivalents and financial assets of $6.8 million.

1H20 Financial Highlights (Source: Company Reports)

What to Expect: The progress towards achieving CE Mark for OncoSil™ device will enable future commercial sales in the European Union, Australia/New Zealand and certain parts of Asia. The company expects the ongoing progress in manufacturing capabilities, supply chain and sales and marketing infrastructure to support both planned commercial and clinical activities.

Stock Recommendation: As per ASX, the stock of OSL is going through a volatile phase with a 57.89% return in the past six months but a negative return of 29.41% in the last one month. Over the span of 3 years, the company has witnessed an improvement in EBITDA margin and net margin. The company also witnessed an improvement in ROE in the past two years. On the TTM basis, the stock is trading at a price to book value multiple of 10.4x, higher than the industry average (healthcare) of 3.2x. Considering the volatility in returns, improvement in margins and progress in manufacturing capabilities, we suggest investors to keep an eye on the stock and have a watch stance at the current market price of $0.110, down by 8.333% on 19 March 2020.

Neuroscientific Biopharmaceuticals Ltd

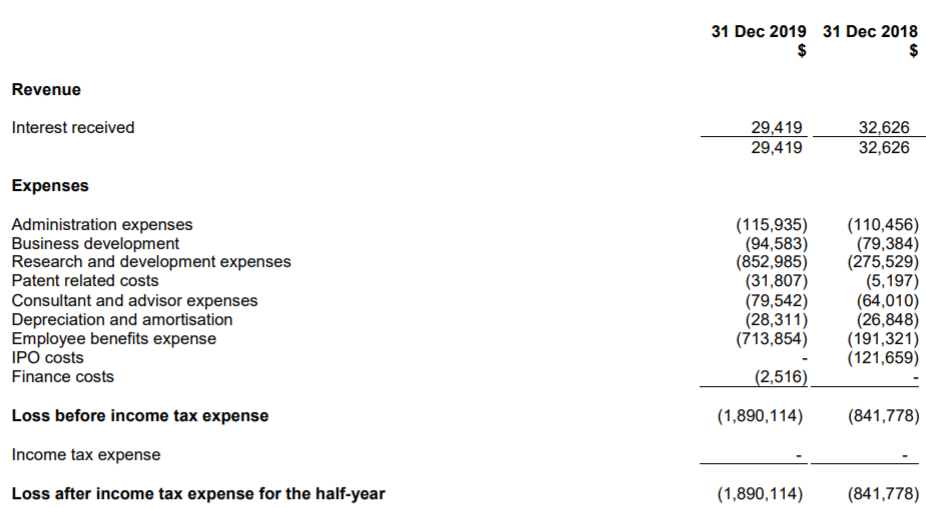

Positive Results in MS Study: Neuroscientific Biopharmaceuticals Ltd (ASX: NSB) is engaged in the development of diagnostic and therapeutic treatments for neurodegenerative diseases through preclinical studies of patented technologies. As on 19 March 2020, the market capitalization of the company stood at $11.37 million. The company has recently reported positive results of a preclinical study of its lead drug candidate EmtinB in an in vitro model for Multiple sclerosis (MS).

The company has recently released its interim results for the period ending 31 December 2019, wherein it reported a loss of $1.89 million with a cash balance of $4.17 million.

1H20 Financial Highlights (Source: Company Reports)

Stock Recommendation: As per ASX, the stock of NSB gave a negative return of 5.71% in the past one year and a negative return of 17.5% in the last three months. During 1H20, Assets/Equity ratio of the company stood at 1.02x, lower than the industry median of 1.47x. In the same time span, the company witnessed a decline in EBITDA margin and net margin. Considering the negative returns, lower Assets/Equity ratio and positive results in MS study, we suggest investors to closely track the stock and have a watch stance at the current market price of $0.170, up by 3.03% on 19 March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...