.png)

Stocks’ Details

Healius Limited

Chairman’s Address to Shareholders:Healius Limited (ASX: HLS) is a provider of medical, para-medical and related services. It also works as a day surgery operator. The market capitalisation of the company stood at A$1.94 Bn as on 25th November 2019. The Chairman of the company stated that the group’s revenue witnessed a rise of around 6% to $1.8 billion and underlying net profit after tax was up 6.5% to $93 million in FY19. The company treats the following main initiatives as non-underlying: (1) The transformation program in Medical Centres called Leapfrog, (2) Core technology upgrades in Pathology and Imaging, and (3) Corporate infrastructure renewal program.

.png)

Group Results (Source: Company Reports)

What to Expect:For FY20, it anticipates underlying net profit after tax in the range of $94 million and $102 million, before any changes from the implementation of AASB 16 on leases and subject to any unforeseen circumstances. It added that the continuation of the strong trading conditions in Pathology in Q1 would be the most important factor in the successful delivery of the forecast.

Stock Recommendation:HLS remains focused on managing the level of debts and strives to balance an optimal gearing ratio with capital needs and dividends. The stock of HLS has EV to sales multiple of 1.4x in comparison to the industry median (Healthcare) of 9.4x on TTM basis. HLS has EV to EBITDA multiple of 9.9x against the industry median (Healthcare Providers & Services) of 10.0x on TTM basis. In the span of three months, the stock of HLS provided returns of 1.63% and 27.87% on YTD basis. Therefore, considering the valuation metrics, its focus towards managing the debt levels and others, we maintain a “Hold” rating on the stock at the current market price of A$3.040 per share, down 2.564% on 25th November 2019.

Mayne Pharma Group Limited

A 4% Decline in EBITDA:Mayne Pharma Group Limited (ASX: MYX) develops, manufactures and markets branded and generic pharmaceutical products globally. The market capitalisation of the company stood at A$813.09 Mn as on 25th November 2019. At the Annual General Meeting of 2019, key personnel of MYX addressed the shareholders and pointed out the performance of FY19, wherein revenue witnessed a fall of 1% on pcp basis, at $525 Mn. However, gross profit stood at $290 Mn, reflecting a rise of 13% on pcp. The company witnessed a decline of 4% in EBITDA to $112 Mn. MYX also saw a decline of 20% on pcp in underlying EBITDA, at $131 Mn.

EBITDA was impacted by greater investment in commercial infrastructure in order to support the recent brand launches of TOLSURA and LEXETTE and additional brand research and development spend, which is not generally capitalised.

.png)

Key Financials (Source: Company Reports)

Future Guidance:For FY20, MYX anticipates stronger results driven by the recent specialty brand launches of TOLSURA and LEXETTE; growth of the generic and proprietary dermatology and women’s health portfolios; and accelerated growth of Metrics Contract Services, driven byadditional headcount.

Stock Recommendation:The stock of MYX has EV to EBITDA multiple of 9.4x as compared to the industry average (Pharmaceuticals) of 4.1x on TTM basis. The stock of MYX delivered negative returns of 15.65% and 17.09% in the time frame of one month and six months, respectively. Moreover, the company is expected to announce its half-year results on February 19, 2020, a key event to watch out for. Thus, in the light of the recent price movement, current trading levels and stretched valuations, we have a watch stance on the stock at the current market price of A$0.460 per share, down 5.155% on 25th November 2019, taking cues from the recent release related to the AGM 2019.

Volpara Health Technologies Limited

Acquisition of MRS:Volpara Health Technologies Limited (ASX: VHT) develops digital health solutions in order to enable personalised breast cancer screening software applications and has a market capitalisation of A$390.33 Mn on 25th November 2019. Recently, the company updated the market participants with results for the half-year ended 30th September 2019 and stated that in June 2019, it acquired MRS Systems, Inc. for a consideration of NZ$23 Mn. During 1HFY20, it successfully undertook a capital raising of A$55 Mn. The company made a substantial investment in research and development with the launch of a major new product suite at the upcoming RSNA trade show in Chicago in December.

.png)

Operating Expenses (Source: Company Reports)

Future Prospects:The company’s focus for FY20 revolves around increasing ARR to NZ$17.1 Mn by the end of FY20. The company is focusing on increasing the market share to more than 27% of US women having a Group product applied on their images and data.

Stock Recommendation:VHT would continue to innovate and iterate its product suite with the now expanded engineering and sciences teams. Gross margin of the company stood at 88.7% in 1H FY 2020, reflecting a rise of 5.3% on the YoY basis. The stock of VHT delivered returns of 8.16% and 18.54% in the span of one month and three months, respectively. Therefore, taking into account, the company’s focus on accelerating the sales growth, increasing ARPU, respectable improvement in key margins, we recommend a “Hold” rating on the stock at the current market price of A$1.740 per share, down 2.793% on 25th November 2019.

Kazia Therapeutics Limited

Interim Data from Phase II Study Of GDC-0084: Kazia Therapeutics Limited (ASX: KZA) partners with the world’s leading researchers and drug developers to bring forward a diversified portfolio of new cancer therapies. The market capitalisation of the company stood at A$31.75 Mn as on 25th November 2019. Recently, the company has shared interim data from its ongoing phase II study of GDC-0084 in glioblastoma, which is the most common and most aggressive form of primary brain cancer. The median progression-free survival (PFS) was calculated at 8.4 months, which reflects that GDC-0084 might delay the progression of glioblastoma. It was mentioned in the release that the median overall survival could not yet be calculated because of insufficient death events on the study. However, 75% of evaluable patients remained alive at analysis cut-off date.

Financial Highlights (Source: Company Reports)

Future Prospects:As per 2019 Annual Report, the company’s aspiration is to take GDC-0084 forward into a registrational clinical trial, which will commence in the calendar year 2020. This trial would be designed to secure an FDA approval, allowing GDC-0084 to become a commercial product, potentially within the upcoming few years.

Stock Recommendation:The company recently announced that it has completed the placement of 10 million new fully paid ordinary shares in the company to institutional, professional, and sophisticated investors in Australia and internationally, at a price of A$0.40 per new share by raising an amount of A$4.0 million. The stock of KZA has EV to sales multiple of 17.8x in comparison to the industry median (Healthcare) of 9.4x on TTM basis. As per the ASX, the stock of KZA is trading close to its 52-week high of A$0.800. The company has scheduled to conduct its extraordinary shareholders meeting on 19th December 2019, wherein, it might discuss its growth prospects and core business activities, which could help the company to gain traction in the market. Thus, we advise investors to wait and look out for further growth catalysts. Therefore, we have a watch stance on the stock at the current market price of A$0.730 per share, up 65.909% on 25th November 2019, primarily due to the release of interim data from phase II study of GDC-0084.

Next Science Limited

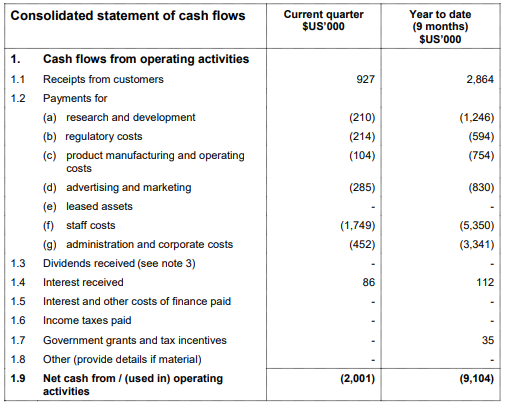

A Look at Q3 FY19 Results:Next Science Limited (ASX: NXS) is involved in commercialising and developing its Xbio technology, which is a non-toxic technology with proven efficacy in eradicating biofilm-based and free-floating bacteria, in a range of products for the treatment of biofilm-based infections. The market capitalisation of the company stood at A$449.84 Mn as on 25th November 2019. The company recently announced its results for Q3 FY19, wherein it was mentioned that NXS has completed the treatment of around 100,000 patients using XbioTM products, which are available in more than 1,200 US hospitals, reflecting a rise of 150 hospitals in Q3.

Cash Flows (Source: Company Reports)

Future Guidance:The company’s outlook for 2020 revolves around (1) Driving sales growth for existing products with its partners in the US, (2) Expanding the existing product sales with entry into new geographic markets, and (3) Launch of four new products in the US, i.e., Surgical Disinfectant, Surgical Rinse, Middle Ear Wash and Sinus Wash.

Stock Recommendation:On the valuation front, the stock of NXS has EV to sales multiple of 34.0x in comparison to the industry median (Pharmaceuticals) of 10.8x on TTM basis. The stock of NXS generated returns of -9.39% and -11.62% in the time period of one month and three months, respectively. Thus, considering the negative returns in last months and other aforesaid facts, we have a watch stance on the stock at the current market price of A$2.400 per share, down 4.382% on 25th November 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...