.png)

Stocks’ Details

Hub24 Limited

Revenues up 12% Year over Year in 1HFY20: Hub24 Limited (ASX: HUB) offers investment and superannuation portfolio administration services and licensee services to financial advisers. Recently, HUB appointed Ms Debbie Last as its interim Chief Financial Officer (CFO) and Joint Company Secretary. Ms Debbie has an expertise of 25 years in the financial services sector. In another update, the company announced that Credit Suisse Holdings Limited has become a substantial holder of the company with a voting power of 5.37%.

A Look at Operational Results for 1HFY20: The company announced its results for the half year ended 31 December 2019, wherein it reported operating revenue of $52.7 million, an increase of 12% year over year. The company recorded a rise of 73% in its underlying net profit after tax, that came in at $5.4 million and a growth of 71% in underlying group EBITDA to $11.7 million in 1HFY20. In the same time span, the company reported record net inflows of $2.5 billion. HUB’s leading technology, product leadership and customer focus were key positives. The board declared an unfranked interim dividend of 3.5 cents per share, reflecting an increase of 75% on 1HFY19.

.png)

1HFY20 Financial Metrics (Source: Company Reports)

What to Expect: The company has increased its staff to grow its capability for distribution and hence is targeting FUA in the range of $22 to $26 billion for FY21. The company is expecting significant growth in financial results and expects to deliver higher shareholder value in the forthcoming years.

Valuation Methodology: EV/Sales Multiple Based Relative Valuation

.png)

EV/Sales Multiple Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock has a market capitalisation of $548.02 million. The company has a PE multiple of 54.36x, with an annual dividend yield of 0.7%. As per ASX, the stock of HUB is trading very close to its 52-weeks low level of $8.660, proffering a decent opportunity for accumulation. Thus, considering the trading levels, decent financial performance, improvement in key margins and a modest outlook, we have valued the stock using EV/Sales based relative valuation approach and have arrived at a target price offering an upside of lower double-digit (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $8.760, up by 0.459% on 5 March 2020.

SeaLink Travel Group Limited

Revenues up ~4.6% Year Over Year: SeaLink Travel Group Limited (ASX: SLK) is engaged in providing tourism and transport services. Recently, the company stated that one of its Directors, named Fiona Hele, has acquired 5,672 ordinary shares for a consideration of $4.40 per share.

Managerial Changes: On 26 February 2020, SKL announced that Andrew McEvoy has stepped down from the post of non-executive director and Chairman of the Board of SeaLink, in order to take up an international executive role overseas, effective from 30 June 2020.

H1FY20 Financial Highlights for the Period ended 31 December 2019: The company reported operating revenue for the period at $132.9 million, up 4.6% year over year on the back of robust growth in Captain Cook Cruises, NSW & WA businesses. Underlying NPAT came in at $13.6 million, up 3.8% year over year. The company’s underlying EBIT stood at $18.3 million, up 1.7% year over year. Net operating cash inflow for the period stood at $25.2 million, as compared to $28.9 million in the prior corresponding period.

.png)

1HFY20 Financial Metrics (Source: Company Reports)

Outlook: Going forward, the company expects to capitalise on Transit Systems Group integration opportunities. The company also remains on track to focus on domestic tourism to lessen coronavirus impact. For 2HFY20, the company expects reduction in EBITDA of $5 million, owing to the combined impact of bushfires and coronavirus outbreak on the business.

Valuation Methodology: P/BV Multiple Based Valuation

.png)

P/BV Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock has a market capitalisation of $906.36 million. The company has a PE multiple of 26.43x, with an annual dividend yield of 3.61%. As per ASX, the stock of SLK is trading below the average of its 52-weeks low and high of $3.368 and $5.310, respectively, proffering a decent opportunity for accumulation. Thus, considering the trading levels, we have valued the stock using P/B based relative valuation approach and have arrived at a target price with an upside of lower double-digit (in percentage terms). For the purpose, we have taken peers like Corporate Travel Management Ltd (ASX: CTD), Flight Centre Travel Group Ltd (ASX: FLT) and Village Roadshow Ltd (ASX: VRL). Hence, we recommend a “Buy” rating on the stock at the current market price of $4.23, up by 1.928% on 05 March 2020.

Synlait Milk Limited

Strong Growth in Consumer-Packaged Infant Formula Unit a Key Catalyst: Synlait Milk Limited (ASX: SM1) is a dairy manufacturer, which aims to supply higher value dairy products to primary milk-based health and nutrition companies. The company is set to report its first half FY20 results on 19th March 2020.

SM1 Updates FY20 Viewpoint: Recently, the company provided an update for its FY20 outlook, wherein SM1 predicts FY20 NPAT to be in the range of $70 million and $85 million. As per the previous guidance, SM1 had forecasted profits to grow in FY20 at the similar rate to FY19 over FY18. Nevertheless, current outlook now indicates that this rate of growth will not be attained partly on the back of lower than expected infant base powder sales and lactoferrin prices being more volatile. However, SM1 expects robust growth within the consumer-packaged infant formula segment. At the end of FY19, total net debt amounted to $333.6 million, as compared to $114.9 million at the end of FY18.

.png)

Debt (Source: Company Reports)

What to Expect for HY20:The company expects NPAT to be in the ambit of $26.5 million to $28.5 million for HY20, as compared to $37.3 million reported in HY19. SM1’s HY20 outlook will be impeded by increased SG&A costs associated with the Pokeno and advanced liquid dairy packaging facilities, incremental interest as well as lower sales volumes.

Valuation Methodology: P/E Based Valuation

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock of SM1 is trading close to its 52-week low level of $5.090, proffering a decent opportunity for accumulation. Synlait remains on track to invest in long-term strategic prospects and take necessary steps to develop and offer new opportunities to existing and potential customers. The stock has a market capitalisation of $970.05 million, with a PE multiple of 12.32x. We have valued the stock using P/E based relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). Thus, considering the current trading levels and long-term strategy, we give a “Buy” recommendation on the stock at the current market price of $5.53 per share, up by 2.218% on 5 March 2020.

amaysim Australia Limited

Higher Mobile Subscriber Growth in 1HFY20 is a Key Positive: amaysim Australia Limited (ASX: AYS) is engaged in providing mobile services in Australia and has a market capitalisation of $92.96 Mn as on 5 March 2020.

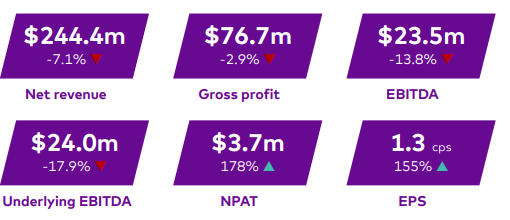

1HFY20 Key Financial Highlights for the Period Ended 31 December 2019: During the period, the company generated net revenue of $244.4 million, down 7.1% on pcp, due to lower Average Revenue per Subscriber (ARPU) across the mobile and energy business units. Underlying EBITDA for the period came in at $24 million, down 17.9% on a year over year basis. Net profit after tax from continuing operations amounted to $3.7 million, up a whopping 178% year over year. The company witnessed growth in mobile subscribers in 1HFY20.

1HFY20 Financial Metrics (Source: Company Reports)

Outlook: FY20 underlying EBITDA is expected to be in the range of $33 million - $39 million, on a New GAAP basis. The company remains on track to grow its mobile business in 2HFY20 and will also continue to reinvest in marketing initiatives to drive continued and commercially sustainable growth.

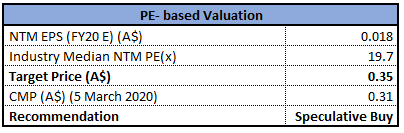

Valuation Methodology: P/E Multiple Based Relative Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to its 52-week low level of $0.870. The company is well funded to capitalise on its growth opportunities in the near-term. Considering the aforesaid facts, we have valued the stock using one relative valuation method, i.e., P/E based multiple and arrived at a target price with lower double-digit upside (in % terms). Hence, looking at the current trading levels and business prospects, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.310, down 1.587% as on 5 March 2020.

Bionomics Limited

Completed the Sale of Neurofit SAS and PC SAS: Bionomics Limited (ASX: BNO) is engaged in developing new and innovative treatments for cancer and diseases of the central nervous system. On 3 March 2020, the company announced that it has completed the sale of its two wholly owned subsidiaries, Neurofit SAS and PC SAS to Domain Therapeutics for a consideration of €1,790,028.97.

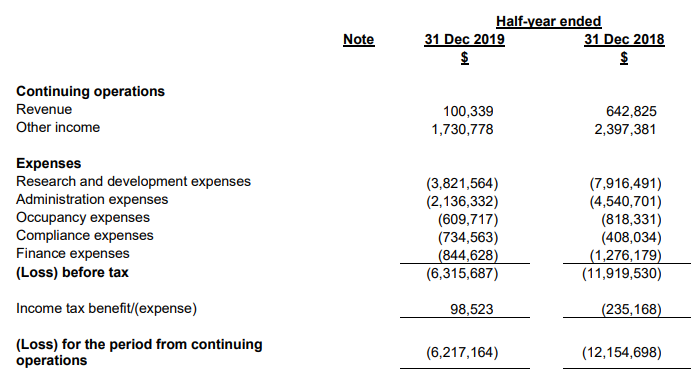

1HFY20 Key Financial Highlights for the Period Ended 31 December 2019: During the period, the company’s revenue and other incomefrom continuing operations came in at of $1.8 million, down from $3 million reported in the year-ago period.Loss after tax from continuing operations for the period came in at $6.2 million, down from $12.2 million reported in the year-ago quarter. The company exited the period with cash and cash equivalents of $8.6 million, with total borrowings amounting to ~$12.60 million. Net operating cash outflow for the period stood at $122.5K.

1HFY20 Key Highlights (Source: Company Reports)

Outlook: The company expects to additionally enhance the prototype tablet formulation to optimize the formulation for a 2nd Phase 2b clinical trial and anticipates building BNC210 tablets for clinical trial in healthy volunteers.

Stock Recommendation: As per ASX, the stock of BNO gave a return of ~36.11% in the past six months and is inclined towards its 52-week low level of $0.031. On TTM basis, its EV/Sales ratio stood at 2.1x and the industry median (Healthcare) is 9.3x, while its P/B multiple is 2.4x as compared to the industry average (Healthcare) of 3.8x. Hence, looking at the current trading levels and business prospects, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.050, up 2.041% as on 5 March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...