.png)

Stocks’ Details

Freedom Foods Group Limited

Accelerated Efforts towards Growth:Freedom Foods Group Limited (ASX: FNP) is engaged in the manufacturing and sale of consumer staples, such as cereal, snacks, dairy, etc. In a recent announcement, the company updated that Campbell Nicholas now stands as the sole Company Secretary of the company, after the resignation of Amber Stanley as joint Company Secretary.

1HFY20 Results: During the six months ended 31st December 2019, the company reported sales amounting to $277.1 million, up 32.6% on the prior corresponding half. Operating EBITDA went up by 55.7% to $32.7 million. Growth during the half was supported by increased marketing expenditure, introduction of new product formats, growth in key branded categories and channels, etc. The Board declared an interim dividend amounting to 2.25 cents per share to be paid on 22nd May 2020.

.png)

Growth in Sales and EBITDA (Source: Company Reports)

Outlook: Going forward, the company expects its key brands to be the drivers of growth, along with an additional contribution from new product revenue streams from the Nutritionals capability. The company is looking forward to further improvements in working capital and operating cashflow in the second half, with an improvement of $36.5 million in operating cash flow already reported in the first half.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation

.png)

Price to Earnings Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company corrected by 12.01% in the last three months and is currently trading close to its 52-week low level of $3.950. The company is placed among the top growth drivers for branded sales in Australian grocery. It is continuously engaged in driving sales through new product development, with $7.6 million invested in the first half. Moreover, it is one of the largest dairy milk producers in Australia, with an expected production of 190 million litres by the end of FY21 from a significant expansion in capacity. We have valued the stock using a Price to Earnings based relative valuation method and arrived at a target price of lower double-digit growth (in percentage terms). For the said purposes, we have considered Bega Cheese Ltd (ASX: BGA), Blackmores Ltd (ASX: BKL), A2 Milk Company Ltd (ASX: A2M), etc., as peers.Hence, we give a “Buy” recommendation on the stock at the current market price of $4.080, down 5.991% on 12th March 2020.

HUB24 Limited

1HFY20 Dividend up by 75%: HUB24 Limited (ASX: HUB) is engaged in the provision of investment and superannuation portfolio administration services, provision of licensee services, software license and IT consulting services. In a recent announcement, the company notified that Credit Suisse Holdings (Australia) Limited increased its voting power from 5.37% to 6.88%. In another update, the company announced the appointment of Debbie Last as the interim CFO and Joint Company Secretary.

First Half Results: During the first half ended 31st December 2019, the company reported platform segment revenue of $35 million, up 38% on the prior corresponding half. Underlying EBITDA for the segment went up by 73% to $13.8 million.Dividend, for the half, came in at 3.5 cents per share, representing an increase of 75% on pcp. During the half, the company reported record net inflows from new and existing clients as a result of market-leading technology and a customer-oriented approach to business.

.png)

Platform Segment Results (Source: Company Reports)

Valuation Methodology:EV/EBITDA Multiple Based Relative Valuation

.png)

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company corrected by 26.90% in the last three months and is currently trading close to its 52-week low level of $6.800. The company is targeting for Funds under Administration in the range of $22 billion - $26 billion in FY21, on the back of continued focus on innovation, strong financial growth, and expansion of market share. We have valued the stock using EV/Sales based relative valuation method and have arrived at a target price with low double-digit upside in percentage terms. Hence, we give a “Buy” recommendation on the stock at the current market price of $6.860, down 8.533% on 12th March 2020.

Synlait Milk Limited

Dairyworks to Contribute ~$2 million to FY20 NPAT:Synlait Milk Limited (ASX: SM1) is a supplier of dairy products to primarily milk-based health and nutrition companies. The company has recently received approval from the Overseas Investment Office for the purchase of shares in Dairyworks Limited. This will provide a push to the company’s Everyday Dairy strategy, providing new opportunities in the sector and a diversified earnings base for shareholders.

Financial Guidance: FY20 net profit after tax is expected to be in the range of $70 million - $85 million. The acquisition of Dairyworks is expected to contribute an amount of ~$4 million to EBITDA and ~$2 million to NPAT, after borrowing costs and depreciation. 1HFY20 NPAT is expected in the range of $26.5 million - $28.5 million, driven by an increase in sales of consumer-packaged infant formula volumes that increased by 21% in FY19.

.png)

Sales Volumes (Source: Company Reports)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation

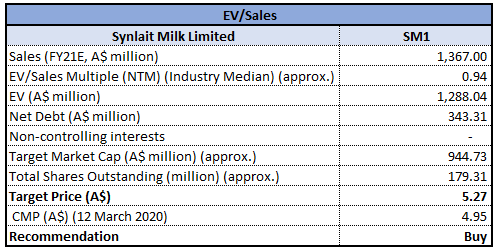

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company corrected by 43.76% in the last three months and is currently trading close to its 52-week low level of $4.640. The company is focused on driving long-term earnings growth through strategic opportunities that may initially involve additional costs. It has a strong customer pipeline with significant capacity across the manufacturing and packaging facilities, that are expected to act as key catalysts for future growth. We have valued the stock using EV/Sales based relative valuation method and have arrived at a target price with single-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $4.950, up 1.643% on 12th March 2020.

iCar Asia Limited

Strong Growth across All Countries:iCar Asia Limited (ASX: ICQ) is engaged in the development of internet-based automotive portals in South East Asia.

Financial Results for the Year Ended 31st December 2019: Revenue for the period stood at $14.8 million, representing an increase of 28% on the previous year. The company reported a significant decrease in full-year proforma EBITDA loss, which stood at $5.5 million in 2019 as compared to $10 million in 2018. The company reported strong results across all three countries of operation, including Malaysia, Thailand and Indonesia.

.png)

2019 Results (Source: Company Reports)

Outlook: With continuous improvement in performance across all countries, the company is set to attain a cashflow positive position by 2HFY20. Revenue in 2020 is expected to grow by more than 50%, with New Car revenue growing on the back of increased media activity and events. The company acquired the Carmudi Indonesia business in November 2019, with revenue synergies expected to be realised from 2H 2020.

Stock Recommendation: The stock of the company corrected by 20% in the last three months and is currently trading close to the average of its 52-week trading range of $0.115 - $0.480. The stock is available at an EV/Sales multiple of 7.5x, as compared to the industry average of 14.4x. Considering the above factors along with the performance in 2019, anticipated synergies from acquisition and progress across all areas of operations, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.280, down 6.667% on 12th March 2020.

Praemium Limited

Record Results in 1HFY20:Praemium Limited (ASX: PPS) is a global provider of technology platforms for managed accounts, investment administration and financial planning.

First Half Performance: During the first half, the company’s Funds under Administration crossed the $20 billion mark for the first time. Platform FUA increased by 30% in CY19. Underlying EBITDA stood at a record level of $7 million, representing an increase of 37% on the prior corresponding half. NPAT increased by 122% to $1.4 million.

.png)

Revenue & EBITDA (Source: Company Reports)

Valuation Methodology:Price to Earnings Multiple Based Relative Valuation

.png)

Price to Earnings Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company corrected by 39.58% in the last three months and is currently trading close to its 52-week low level of $0.265. Going forward, the company is expected to derive benefits from the upgradation to a fully integrated managed accounts platform to ensure enhanced client experience, improved performance in the international business, and increasing popularity of the Virtual Managed Accounts (VMA) administration service. We have valued the stock using Price to Earnings based relative valuation method and for the purpose, have taken the peer group - OneVue Holdings Ltd (ASX: OVH), EQT Holdings Ltd (ASX: EQT) and Hub24 Ltd (ASX: HUB). As a result, we have arrived at a target price with lower double-digit upside (in percentage terms). Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.270, down 6.897% on 12th March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...