.png)

Stocks’ Details

Woodside Petroleum Ltd

Sale and Purchase Agreement:Woodside Petroleum Ltd (ASX: WPL) is engaged in the operation and management of hydrocarbon exploration. The market capitalisation of the company stood at A$32.76 Bn as on 6th January 2020. Recently, the company, with the help of a release dated 24th December 2019, announced that Woodside Energy Trading Singapore Pte Ltd entered a long-term sale and purchase agreement with Uniper Global Commodities SE. Under the agreement, the company will supply LNG from its global portfolio for a term of 13 years, which would commence in 2021. In the initial stage, the quantity of LNG to be supplied would be up to 0.5 Mtpa, increasing to around 1 Mtpa from 2025.

On the financial front, in Q3 FY19, the company reported sales revenue amounting to $1,164 million, reflecting a rise of 58% as compared to the previous quarter. This is resulted by a 44% increase in production from the previous quarter and stronger realised LNG pricing.

.png)

Record LNG Production (Source: Company Reports)

What to Expect:For 2019, the company is expecting total depreciation and amortisation in the range of $1,650 million – 1,800 million. The company added that its major growth projects are progressing well towards key decision points.

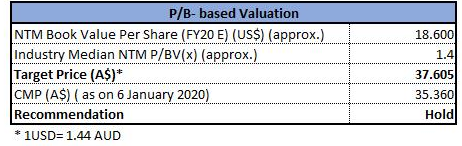

Valuation Methodology:P/BV Multiple Approach

P/BV Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The company has also inked a non-binding letter of agreement with Korea Gas Corporation for determining the feasibility of a green hydrogen pilot project throughout the value chain. We have valued the stock using the P/BV approach and arrived at a target price, which is offering an upside of mid-single digit (in percentage terms). During the span of one month and three months, the stock of WPL has provided returns of 3.24% and 13.00%, respectively. As the market participants are aware, there are ongoing tensions in the middle east due to the drone strike by the US. Therefore, in the light of the recent agreement signed by the company, favorable valuations, and returns in the past months, we maintain a “Hold” rating on the stock at the current market price of A$35.360 per share, up 1.697% on 6th January 2020.

Karoon Energy Ltd

Drilling Update on Peru:Karoon Energy Ltd (ASX: KAR) is engaged in the exploration of oil and gas and has a market capitalisation of A$641.46 Mn as on 6th January 2020. The company recently announced that the Stena Forth Drillship has started the final leg of its mobilisation to Peru ahead of drilling the Marina-1 exploration well in the Block Z-38 Tumbes Basin, Peru. The company added that the Marina prospect has a gross mean prospective resource of 256 million barrels of oil. In another update, the company announced that Credit Suisse Holdings (Australia) Limited, on behalf of Credit Suisse Group AG and its affiliates, has ceased to become a substantial holder in the company on 13th December 2019.

As at 30th September 2019, the cash balance of the company stood at $256 million, which reflects the deposit amounting to US$50 million, which was paid during July 2019 with respect to the SPA (Sale and Purchase Agreement). However, this does not comprise any contribution from the equity raising announced in October 2019.

.png)

Net Cash from Operating Activities (Source: Company Reports)

Decent Returns to Shareholders:As per 2019 Annual Report, the company is strongly focused on delivering on its strategic agenda for the benefit of its shareholders. The priority of the top management of the company with respect to capital management is to attain the best returns for shareholders in the medium to longer term.

Stock Recommendation:The priority of the Board for capital allocation would be first to invest in growth, then debt reduction and dividends to shareholders. However, any excess capital thereafter would be allocated towards the initiatives like share buy-backs or capital returns. Current ratio of the company stood at 41.65x in FY19 as compared to the industry median of 1.21x. This reflects that the company is in a decent position to address its short-term obligations as compared to the broader industry. On TTM basis, its EV/Sales stood at 4.1x and the industry median (Energy) is 25.8x while P/B multiple is 1.2x as compared to industry average (Energy) of 8.4x. Thus, considering the decent liquidity position, stable balance sheet and improvement in key margins, we give a “Hold” recommendation on the stock at the current market price of A$1.260 per share, up 8.621% on 6th January 2020.

Worley Limited

Five-Year Contract:Worley Limited (ASX: WOR) provides professional services to help its customers to meet the changing requirements for energy, chemicals and resources. The market capitalisation of the company stood at A$8.16 Bn as on 6th January 2020. The company, with the help of a release, announced that ExxonMobil Exploration and Production Malaysia Inc. has presented a five-year engineering, procurement and construction management contract to Perunding Ranhill Worley Sdn Bhd, which happens to be a joint venture entity between the Worley group and Ranhill Group Sdn Bhd as well as is the entity which perform services for PRW. As per the terms of the contract, Ranhill Worley would be delivering brownfield asset restoration as well as debottlenecking projects for offshore projects in Malaysia. The following picture provides an idea of revenue and EBITA growth:

.png)

Revenue and EBITA Growth (Source: Company Reports)

Benefits of ECR Acquisition:The company stated that the acquisition of the ECR business has proved as an important strategic step for WOR, doubling the size of the company and placing it as the leader in the dynamic and growing energy, chemicals and resources sector. In FY20, the company anticipates delivering the advantages of the acquisition of ECR which include the realization of cost, margin and revenue synergies.

Valuation Methodology: EV/Sales Multiple Approach

.png)

EV/Sales Valuation Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:WOR is currently a globally significant company and known as one of the leading exporters of high-value services of Australia. As per the key personnel of the company, the current medium-term picture continues to reflect the global energy transition would open opportunities throughout all markets that it serves. Debt to equity of the company stood at 0.36x in FY19 as compared to 0.45x in FY18. We have valued the stock using EV/Sales multiple approach and arrived at a target price, which is offering an upside of mid-single digit (in percentage terms). As a result of tensions in the middle east, the rise in prices of crude oil has been witnessed and there are expectations that the increased prices might hamper the oil supplies. Therefore, considering the deleveraged balance sheet, decent outlook and recent contract awarded to the joint venture, we maintain a “Hold” rating on the stock at the current market price of A$15.980 per share, up 1.848% on 6th January 2020.

Buru Energy Limited

Oil Production Stood at ~86,000 bbls: Buru Energy Limited (ASX: BRU) is engaged in exploration, development and production of petroleum. Recently, the company informed about the agreement with Roc Oil (Canning) Pty Limited for Roc to withdraw from its current 50% interest in Canning Basin exploration permits EP 428, EP 436 and EP 391.

Q3FY19 Cash Flow highlights for the Period ended 30 September 2019: BRU reported its quarterly cash flow activities, wherein the company reported that net cash used in operating activities stood at $11.855 million and net cash used in investing activities was $0.182 million.The company reported cash and cash equivalents of $46.690 million as on 30th September 2019.

.png)

Net Cash Used in Operating Activities (Source: Company Reports)

The company reported ~86,000 bbls (gross) of oil production during Q3FY19 at an average of ~940bopd including well offline time. The company reported oil sales of ~75,000 barrels (gross) during the same time frame.

Guidance:As per the cash flow guidance for Q4FY19, the company expects exploration costs of $7.7 million, while development expenses is expected to be at $7.3 million. The company expects net cash inflow from production amounting to $2.2 million. The company expects Alcoa repayment during the next quarter is likely to be at $2.7 million. The company is expecting a cash outflow amounting to $16.7 million in the quarter ended December 2019.

Stock Recommendation:The stock of BRU is quoting at $0.175 with a market capitalisation of ~$71.29 million. The stock is quoting at the lower band of its 52-week trading range of $0.165 and $0.360. The company reported continuation of work at Blina Oilfield, which includes the testing of the Upper Yellowdrum zone and the deeper Nullara producing zone. At the current market price, the stock is trading at a P/B multiple of 0.8x on TTM basis as compared to the industry median (Oil & Gas) of 1.4x. Its EV/Sales multiple is 1.5x and industry median (Oil & Gas) of 17.4x. Considering the trading levels, business prospects and discounted valuations, we recommend a ‘Speculative Buy’ on the stock at the current market price of $0.175 per share, up 6.061% as on 06 January 2020.

Orocobre Limited

Q1FY20 Operational Highlights for the Period ended 30 September 2019: Orocobre Limited (ASX: ORE) is engaged in production and exploration of minerals and focuses on developing Lithium/Potash resources in Argentina. ORE announced its quarterly results (Q1 FY 2020), wherein the company reported production of 3,093 tonnes as compared to 2,293 tonnes in Q1FY19. The company added that product sales stood at 3,108 tonnes of lithium carbonate involving an average price amounting to US$7,111/tonne on the FOB basis as well as total sales revenue amounting to US$22.1 million. However, average price received during Q1 FY 2020 fell by 13% QoQ. Gross cash margin, during the quarter, came in at US$2,226 per tonne, down 40% on Q-o-Q basis.

.png)

Operating Highlights (Source: Company Reports)

Guidance:For the quarter ended December 2019, the company stated that indicative weighted average price of lithium carbonate sales is anticipated to be around US$5,400/tonne FOB, subject to achieving the planned shipping schedule. The company stated that market conditions are soft and ORE has made a decision to meet the current pricing in order to ensure the retention of market share.

Stock Recommendation: The stock of ORE is quoting at $2.840 and has a market capitalisation of ~$738.31 million. The stock has generated returns of 13.25% and 16.53% in three months and one month, respectively. ORE has a strong balance sheet, while the business continues to focus on reducing the cost of production and aims to maintain the position as one of the lowest cost producers of lithium chemicals. The stock is available at price to book value of 0.8x on TTM basis as compared to the industry median (Basic Materials) of 1.6x. Its EV/Sales is 5.8x and industry median (Chemicals) stood at 35.5x on TTM basis. Considering the trading levels, lower valuations and business prospects, we recommend a ‘Buy’ rating on the stock at the current market price of $2.840 per share, up 0.709% as on 6th January 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...