Stocks’ Details

Fonterra Shareholders' Fund

Reiterated Farmgate Milk & Earnings Viewpoint: Fonterra Shareholders' Fund (ASX: FSF) is a global leader in dairy exporter, which is involved in shaping the industry in quality and innovation. On 27 February 2020, the company reiterated its estimate for Farmgate Milk Price range at $7.00-7.60 per kgMS. It also reaffirmed its view for FY20 underlying earnings guidance, which lies in the ambit of 15-25 cents per share. Nevertheless, FSF updated the market with a revised forecast of its milk collections for FY20 to be ~1,515 million kgMS, down from the earlier expectation of 1,530 million kgMS. The company remains confident for its Farmgate Milk Price range on the face of current market conditions due to coronavirus impact.

Te Awamutu site Power’s Wood Pellets Instead of Coal: Recently, the company announced its environmental targets demonstrating its commitment to renewable energy as FSF’s Te Awamutu site is set to be coal free, effective from 2020/21. The move will enable the company to save ~84,000 tonnes of carbon emissions each year and will lessen Fonterra’s national coal utilization by roughly 10%. This is an encouraging step to reduce emissions and work towards net zero carbon emissions by 2050.

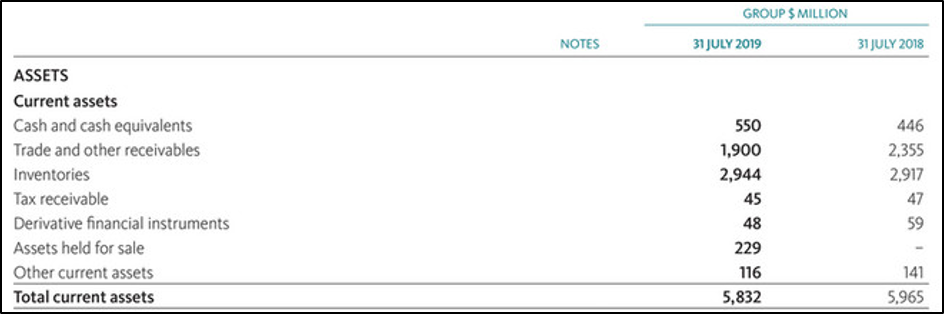

Other Recent Updates: In another update, the company stated that it has completed the sale of its 50% share of DFE Pharma to CVC Strategic Opportunities II. The move will strengthen the company’s balance sheet with cash proceeds of $554 million. At the end of 31 July 2019, the company has cash and cash equivalents of NZ$550 million, with total current assets amounting to NZ$5,832 million.

Stock Recommendation: The stock posted a positive return of ~27.95% in the past six months and is currently trading above the average of its 52-week low and high of $2.940 and $4.440, respectively.The stock has a market capitalisation of $380.71 million, with 110.19 million outstanding shares.Considering the above factors, we recommend a “Buy” rating on the stock at the current market price of $3.740, down 1.579% as on 27 February 2020.

Retail Food Group Limited

NPAT up a Whopping 40.9% Year Over Year: Retail Food Group Limited (ASX: RFG) is a food and beverage company. The company is also engaged in roasting and supplying high-quality coffee products.

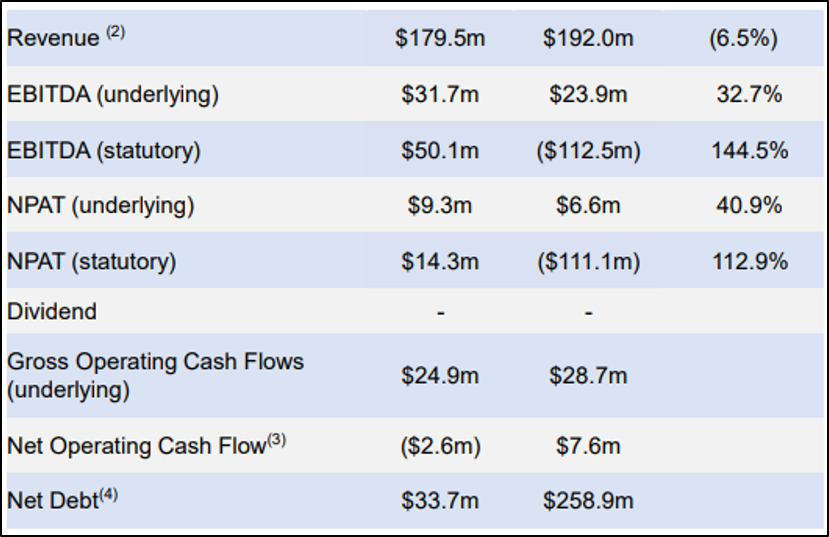

1HFY20 Key Highlights for the Period Ended 31 December 2019: The company reported revenue for the period at $179.5 million, down from $192 million reported in 1HFY19. Underlying NPAT came in at $9.3 million, up 40.9% year over year. The company’s underlying EBITDA stood at $31.7 million, as compared to $23.9 million reported in 1HFY19. Ongoing stabilisation of franchise operations along with anticipated franchise store rationalisation were key positives for the period. Net operating cash outflow for the period stood at $2.6 million, with total net debt amounting to $33.7 million.

1HFY20 Key Financial Metrics (Source: Company Reports)

Outlook: For FY2020, the company expects underlying EBITDA to be in the range of $42 million to $46 million. For 1HFY20, the company expects recapitalisation to offer financial stability.

Stock Recommendation: As per ASX, the stock is trading close to its 52-week low level of $0.090. As on 27 February 2020, the company’s market capitalisation stands at ~$196.97 million, with 2.12 billion outstanding shares. Based on the current trading levels, growth in margins and aforesaid facts, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.098 per share, up 5.376% as on 27 February 2020.

Mosaic Brands Limited

Underlying EBITDA Increased 12.4% Year over Year: Mosaic Brands Limited (ASX: MOZ), formerly known as Noni B Limited, is involved in the retailing of women’s apparel and accessories. As on 27 February 2020, market capitalisation of the company stood at $130.21 million. Recently, the company announced that Wilson Asset Management Group is ceased to be a substantial holder in MOZ, effective from 25 February 2020. In another update, the company stated that Perpetual Limited and its related bodies corporate, one of the substantial holdersin the company, has increased its voting power from 10.25% to 12.80%

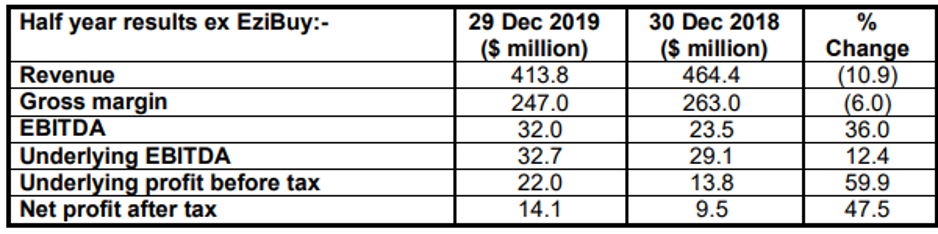

1HFY20 Key Highlights for the Period Ended 29 December 2019: The company’s revenue for 1HFY20 came in at $413.8 million, down from $464.4 million reported in 1HFY19. NPAT for the period amounted to $14.1 million, up 47.5% year over year. The company’s underlying EBITDA stood at $32.7 million, as compared to $29.1 million reported in 1HFY19, indicating successful implementation of company’s strategies and focus on prioritising gross margin over sales. Operating cash inflow for the period stood at $12.5 million, with net cash amounting to $4.5 million.

1HFY20 Key Financial Metrics (Source: Company Reports)

Outlook: The company expects material shortfall on its previously guided EBITDA of $75 million on the back of first half result along with continued uncertainty relating to impact of the bushfires and COVID-19 outbreak.

Stock Recommendation: As per ASX, the stock of MOZ is trading close to its 52-week low of $1.270, offering a decent opportunity for investors for accumulation.The stock of MOZ hasprice to earnings multiple of 16.01x, and an annual dividend yield of 10.78%. On the TTM Basis, the stock of MOZ is trading at an EV/Sales multiple of 0.2x, lower than the industry median (Consumer Cyclicals) of 1.4x. The stock is available at EV/EBITDA multiple of 2.5x, lower than the industry median (Consumer Cyclicals) of 8.5x. Considering the aforesaid facts and current trading levels, we recommend a “Speculative Buy” rating on the stock at the current market price of $1.270, down by 5.576% on 27 February 2020, due to the impact of the bushfires and COVID-19 outbreak on its outlook.

Synlait Milk Limited

Revenues Exceeded $1 Bn in FY19: Synlait Milk Limited (ASX: SM1) is a dairy manufacturer, which aims to supply higher value dairy products to leading milk-based health and nutrition companies. Recently, the company informed the market that 33,666 Performance Share Rights have lapsed as of 31st January 2020. Notably, the company is set to report its first-half FY20 results on 19th March 2020.

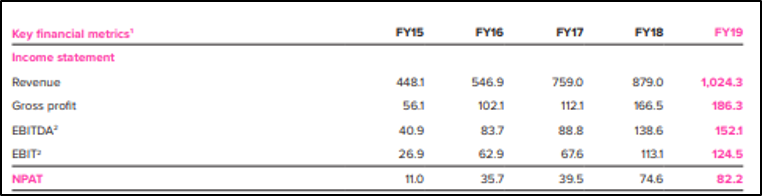

SM1 Updates FY20 Outlook: On 13th February 2020, the company provided an update for its FY20 outlook. The company now expects FY20 earnings to be in the band of $70 million and $85 million net profit after tax. As per the prior guidance the company had projected profits to grow in FY20, with the similar rate to FY19 over FY18. However, current outlook now suggests that this rate of growth will not be achieved partly due to lower than expected infant base powder sales and lactoferrin prices being more volatile. Nevertheless, SM1 expects robust growth within the consumer-packaged infant formula segment. For FY19, revenues exceeded $1 billion, representing an increase of 17% year over year to $1024.3 million.

FY19 Sales Highlight (Source: Company Reports)

Guidance for HY20: The company anticipates NPAT to be in the band of $26.5 million to $28.5 million for HY20, as compared to $37.3 million NPAT reported in HY19. SM1’s HY20 outlook will be obstructed by higher incremental interest, enhanced SG&A costs associated with the Pokeno and advanced liquid dairy packaging facilities along with lower sales volumes.

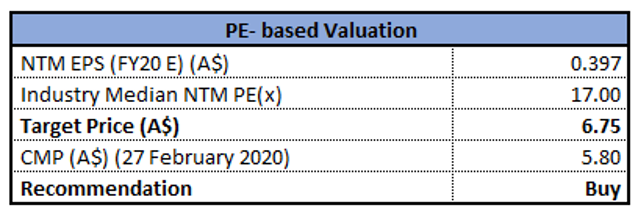

Valuation Methodology: P/E Based Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock of SM1 is trading close to its 52-week low of $5.760, proffering a decent opportunity for accumulation. Synlait continues to invest in long-term strategic opportunities and remains on track to develop and offer new opportunities to existing and prospective customers. We have valued the stock using P/E based relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). Thus, considering the current trading levels and long-term strategy, we give a “Buy” recommendation on the stock at the current market price of $5.80 per share, down 1.528% on 27 February 2020.

Flight Centre Travel Group Limited

Group TTV up 11.2% in 1HFY20: A travel retail company, Flight Centre Travel Group Limited (ASX: FLT) has exposure in both the leisure and corporate travel sectors. The company operates as a tour operator, hotel management, and destination management company. Recently, the company announced that it will distribute a dividend of $0.40 per share, with an ex-date of March 26, 2020 and payment date of April 17, 2020.

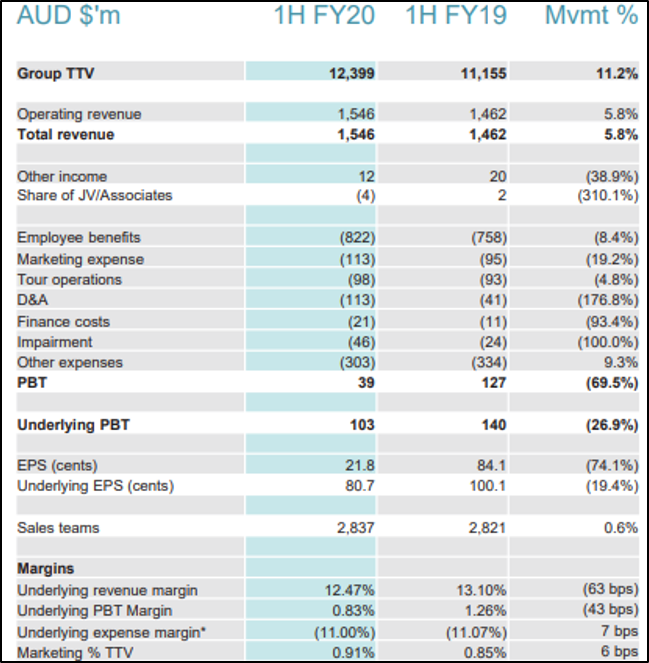

1HFY20 Key Highlights for the Period Ended 31 December 2019: FLT announced its 1HFY20 operational results, wherein the company reported total revenue at $1,546 million, up 5.8% on y-o-y basis. Revenues were aided by improved total transaction value (TTV) across all geographic segments, essentially on the back of corporate brands. The business reported TTV of $12,399 million as compared to $11,155 million in 1HFY19, reporting an 11.2% increase on a y-o-y basis. FLT reported an underlying PBT of $103 million as compared to $140 million in 1HFY19. The company reported cash outflows from operating activities at $136 million in 1HFY20.

1HFY20 Income Statement Highlights (Source: Company Reports)

Outlook: The company is now expecting its underlying PBT for FY20 to be in the range of $240 million & $300 million (previous guidance $310 million & $350 million). The company lowered its FY20 PBT outlook on the back of COVID-19 impact.

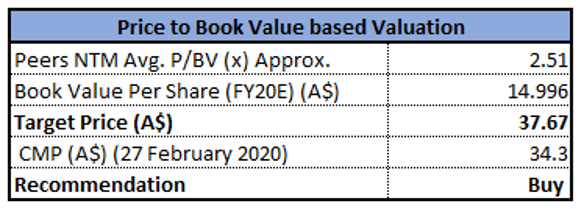

Valuation Methodology:Price to Book Value Based valuation

Price to Book Value based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock is trading at $34.30 with a market capitalization of ~$3.54 billion. Currently, the stock is trading near to its 52-week low of $33.550. The stock has generated a negative return of ~25% in the last six months. The company remains focused on increasing its investment in technology and prioritising on cost reduction initiatives. Considering the current trading levels, improved TTV and business prospects, we have valued the stock using Price to Book Value based relative valuation method. For the said purpose, we have considered peers like Corporate Travel Management Ltd (ASX: CTD), Qantas Airways Ltd (ASX: QAN), Webjet Ltd (ASX: WEB), etc., and arrived at a target price of higher single-digit upside (in percentage terms). Hence, we give a ‘Buy’ recommendation on the stock at the current market price of $34.30, down 2% as on 27 February 2020.

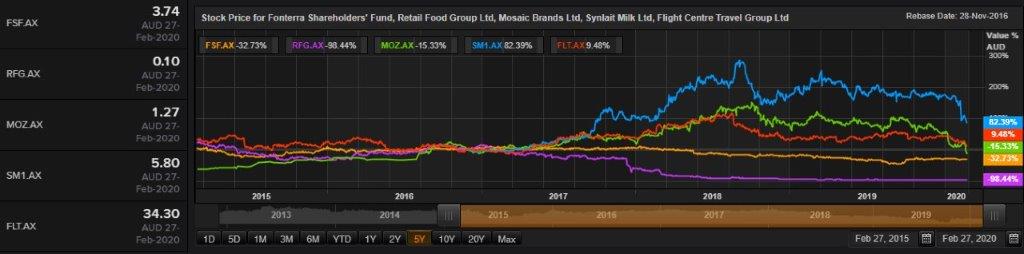

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

.jpg)

Please wait processing your request...

Please wait processing your request...