.png)

Stocks’ Details

Webjet Limited

Response Towards a Media Speculation:Webjet Limited (ASX: WEB) provides full range of online travel booking service for flights, hotels, car hire, cruises, tours etc. The market capitalisation of the company stood at A$1.58 Bn as on 11th December 2019. Recently, the company via a release responded towards a recent media speculation which was related to the expressions of interest in the company. It was mentioned that its objective is to create value for its shareholders and from time to time it considers acquisition interest in the business. WEB continues to be focused on executing its growth strategy.

In FY19, customers made 5.5 million travel bookings with the company throughout the globe, which helped the company in generating nearly $4 Bn in TTV. Revenues of the company amounted to $366.4 Mn, with EBITDA of $124.6 Mn and net profit after tax stood at $81.3 Mn before acquisition amortisation.

.png)

EBITDA by Business (Source: Company Reports)

Opportunities for Profitable Growth:For WebBeds, the company continue to witness significant opportunities for profitable growth throughout all regions. With respect to WebBeds, it was further added that WEB continues to look for attractive acquisition opportunities in order to supplement its existing businesses. However, for Online Republic, the company is continuing with its current strategy to focus on higher TTV margins as well as lower acquisition costs.

Valuation Methodology: P/E Based Valuation

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation:In financial year 2019, the company has implemented a new strategy concentrating on targeting profitable bookings growth with increased margins and lower acquisition costs. Earnings per share of the company stood at 63.3 cps (before AA), reflecting a rise of 31% as compared to the previous year. The Board of the company has declared full-year dividend amounting to 22 cps, with a rise of 10% against the previous year. We have valued the stock using relative valuation method (P/E valuation multiple) and have arrived at the target price which is offering an upside of lower double digit (in percentage terms).Therefore, considering the company’s decent performance in FY19, favorable business prospects and increased final dividend, we give a “Buy” recommendation on the stock at the current market price of A$12.780 per share, up 9.605% on 11th December 2019. It looks like the upside is primarily due to response towards a media speculation.

Super Retail Group Limited

Decent Performance in FY19:Super Retail Group Limited (ASX: SUL) is involved in the operations of specialty retail stores in the automotive, tools, leisure and sports categories. The market capitalisation of the company stood at A$1.98 Bn as on 11th December 2019. The company, through a release dated 9th December 2019, announced that its registered office and principal place of business has been changed to Super Retail Group Limited, 6 Coulthards Avenue, Strathpine QLD 4501. Despite relatively subdued economic conditions, the company delivered a solid result for the financial year 2019, where it achieved total sales growth of 5.4% and witnessed growth in LFL sales throughout all four divisions. This revenue growth was translated into a 7.0% increase in Segment EBITDA, a 3.9% increase in Segment EBIT as well as a rise of 5.0% in normalised net profit after tax.

.png)

Cash Flow and Uses (Source: Company Reports)

Specific Focus on Brands:The company would be leveraging its strong position in the upcoming years with a specific focus on building brands that are as powerful as the products it sells, greater digitisation, supply chain integration and a seamless omni-retail experience. The company is well positioned to grow its market share and create value for its shareholders as it has right strategy in place as well as an experienced management team which is focused on executing the strategy.

Valuation Methodology: P/E Based Valuation

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation:The company’s primary focus would be on achieving organic growth in its existing brands as well as optimising returns to shareholders via disciplined allocation of capital. Earnings growth of the company and strong cash flow generation has enabled the group to (1) Invest capital for growth, (2) Maintain a consistent dividend payout ratio, and (3) Reduce gearing. We have valued the stock using P/E valuation multiple and have arrived at the target price that is giving an upside of mid-single digit (in percentage terms). Therefore, considering the opportunity to decrease debt by around $50 million per annum, strong financial position and Portfolio of highly cash generative businesses, we maintain a “Hold” rating on the stock at the current market price of A$9.950 per share, down 0.896% on 11th December 2019.

Bapcor Limited

Acquisition of Two New Businesses:Bapcor Limited (ASX: BAP) is engaged in the distribution of automotive aftermarket parts and has a market capitalisation of A$1.83 Bn as on 11th December 2019. The company via a release dated 1st November 2019 announced that it has inked agreements to purchase Truckline and Diesel Drive. Truckline is a Heavy commercial truck spare parts business having 22 branches throughout Australia. The release also stated that Diesel Drive is a business which specialises in the sale of Japanese commercial truck spare parts. The purchase price of both businesses stood at around $48 Mn, which would be financed via the existing debt facilities. The businesses are anticipated to achieve a return on investment of at least 15% and enhance earnings per share in the first full year of operation, i.e., FY2021. The below picture depicts an idea of CAGR growth in revenue:

.png)

CAGR Growth (Source: Company Reports)

Uniquely Placed to Provide Aftermarket Parts: The company is exceptionally placed to provide aftermarket parts for all forms of road transport.The company’s strategy is to continue to expand its business reach as well as product offerings. BAP would also be targeting to optimise the benefits of its network and vertically integrated structure via increased intercompany sourcing and operating efficiencies.

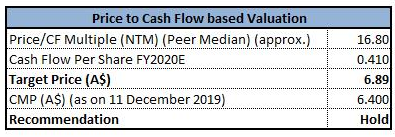

Valuation Methodology: Price to Cash Flow Valuation Multiple

Price to Cash Flow Valuation Multiple (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation:The company is building for the future by undertaking significant technology as well as infrastructure investments in the areas of warehousing, retail point of sale and information technology. The company has been looking for appropriate opportunities in order to enhance its business which deliver shareholder value, while being in line with the strategy as well as disciplined acquisition criteria. We have valued the stock using Price to Cash Flow valuation multiple, which is offering target price which is giving an upside of of lower-single digit (in percentage terms). Hence, considering the decent performance in FY19, acquisition of new businesses, CAGR growth of 42% and 18% in NPAT and dividends during time span of FY15-FY19, respectively, we maintain a “Hold” rating on the stock at the current market price of A$6.400 per share, down 0.621% on 11th December 2019.

Lovisa Holdings Limited

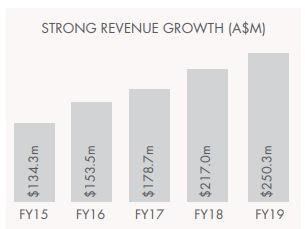

Continuation of Solid Performance:Lovisa Holdings Limited (ASX: LOV) is in the retail sale of fashion jewellery and accessories. The market capitalisation of the company stood at A$1.27 Bn as on 11th December 2019. The company has experienced continuation of solid performance in FY19 as there was new store growth, largely in the UK, US and French markets. The company has delivered growth of 15.3% in top line sales despite the challenge of facing a small negative comparable store sales result for the first time since the company listed. The cash flow of company was strong with operating cash conversion at 107% as it continues to manage its working capital well in the face of the continuing investment into stocking out new stores.

Revenue Growth (Source: Company Reports)

Focused on Growth Strategies:The company is focused on continuing to invest in support of its growth strategy, which meant that overall support costs have increased. LOV would continue to focus on maintaining the right balance between the speed of its new store rollout, and diligence in site selection to ensure every new store meets its investment hurdles.

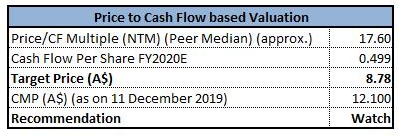

Valuation Methodology: Price to Cash Flow Valuation Multiple

Price to Cash Flow Valuation Multiple (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The company declared a fully franked final dividend amounting to 15 cps, this brought the full year dividend to 33 cents per share. LOV’s balance sheet remains strong and reflects the significant investment made during the year into the rollout of stores. We have valued the stock using Price to Cash Flow based valuation and have arrived at the target price, indicating that the stock price might witness a fall, moving forward. Therefore, we have a watch stance on the stock at the current price of A$12.100 per share, up 0.666% on December 11, 2019.

Kathmandu Holdings Limited

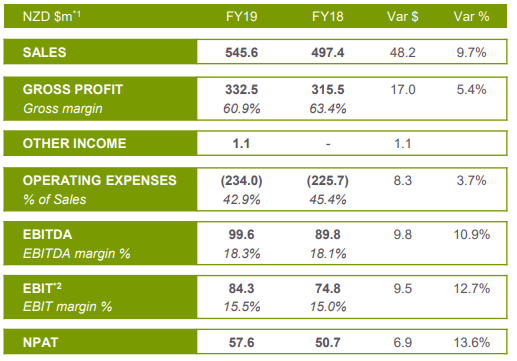

Strong Sales Growth:Kathmandu Holdings Limited (ASX: KMD) happens to be a retailer of clothing and equipment for travel as well as adventure and has a market capitalisation of A$863.46 Mn as on 11th December 2019. The company recently announced that Jarden Partners Limited has made a change to holdings in the company and the current voting power stands at 10.712% as compared to the previous voting power of 12.021%. The company reported a strong FY19 with strong sales growth, mainly via online channels and from Oboz, and well controlled operating expenses helped the combined business to witness record profits.

Financial Performance (Source: Company Reports)

Focus on Growing the Core Markets:The company is well placed to deliver on the next level of growth opportunities. The company would be focusing on growing the core markets of Australia and New Zealand. It would also continue to enhance experience of the customers via digital.

Valuation Methodology: P/E Based Valuation

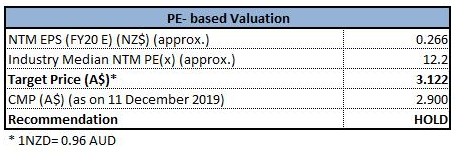

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation:The company would focus towards extending the market leadership in primary product categories, while also accelerating the growth with regards to other high potential categories. The Board of directors of the company have declared a final dividend amounting to NZ 12 cps, which, with an interim dividend of NZ 4 cents per share makes a record payout of NZ 16 cps, reflecting a rise of NZ 1 cps against last year. During the span of one month and three months, the stock of KMD has delivered returns of 6.55% and 25.87%, respectively. We have valued the stock using P/E multiple approach and have arrived at the target price which is offering upside of mid-single digit (in percentage terms). Thus, taking into account favorable metrics and decent returns in the past period, we give a “Hold” recommendation on the stock at the current market price of A$2.900 per share, down 1.024% on 11th November 2019.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...