Stocks’ Details

ResMed Inc

SaaS Grew Exponentially:ResMed Inc(ASX: RMD) is engaged in the business of medical devices with cloud-based software applications. The company recently announced an ordinary dividend of USD 0.037 per security for RMD - CDI 10:1 FOREIGN EXEMPT NYSE, for which the ex-date was May 8, 2019 and payment date is June 13, 2019. The company recently updated that it has issued Chess Depository Instruments (CDI) of 1,433,459,720 at the average issue price for stock options at US$4.65.

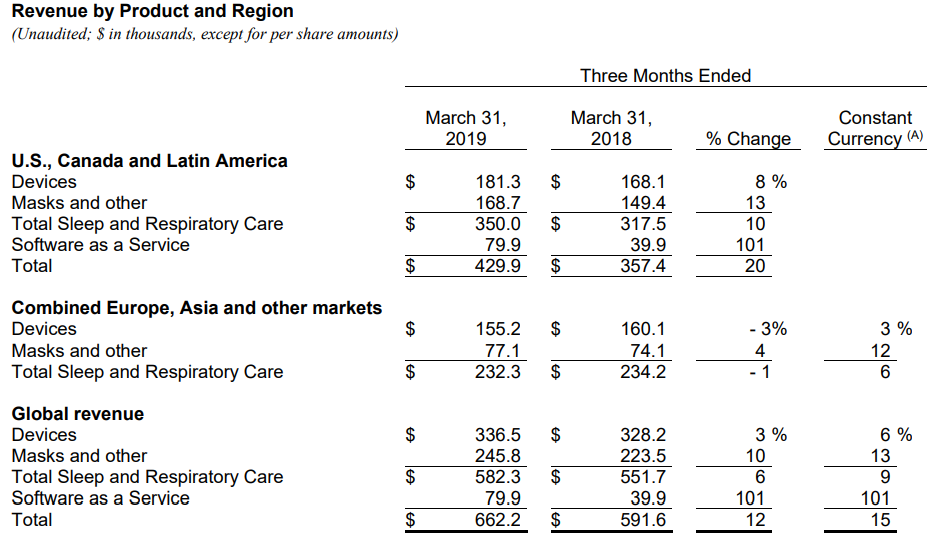

Financial Performance in 3QFY19:The company witnessed strong top-line growth across all the segments with a solid contribution from recently acquired SaaS companies and growth in international device sales. Revenue in the U.S., Canada, and Latin America, excluding Software as a Service (SaaS) recorded a pcp growth of 10%, driven by excellent revenue across mask and device product portfolios.

SaaS in the U.S., Canada, and Latin America posted a growth of 101%, on the back of continued growth in Brightree service offerings and incremental contribution from the acquisition of MatrixCare. Revenue from Combined Europe, Asia and other markets recorded a pcp growth of 6% (Constant Currency). GAAP diluted EPS (earnings per share) saw a decrease of 4%, largely driven by the impact of recent acquisitions, increased interest and income tax expense.

Non-GAAP diluted EPS was 3% lower on pcp. Cash flow from operations for the period came in at $139.6 million as compared to net income of $105.4 million in the quarter. Gross margin increased to 59.2% in 3QFY19 against 58.2% in 3QFY18, mainly due to higher margin contribution from MatrixCare.

Segment Wise- Revenue Break-up (Source: Company Reports)

Stock Recommendation:Looking at the price performance, the stock has gained ~19% in the last 1-year. Stock is trading close to its life-time high level. At the current market price of $17.110, the stock is available at price to earnings multiple of 37.560x. The company has been developing its business through acquisitions of innovative products. Considering the organic growth of the business, geographic expansion, research and development efforts, healthy gross margin along with the historical price movement, we give a “Hold” recommendation on the stock at the current market price of $17.110 per share (up 3.134% on 11 June 2019).

Magellan Financial Group Limited

Strong Performance Driven by Growth in FUM:Magellan Financial Group Limited (ASX: MFG) is engaged in the management of funds for offering international investment funds to high net worth and retail investors and institutional investors.

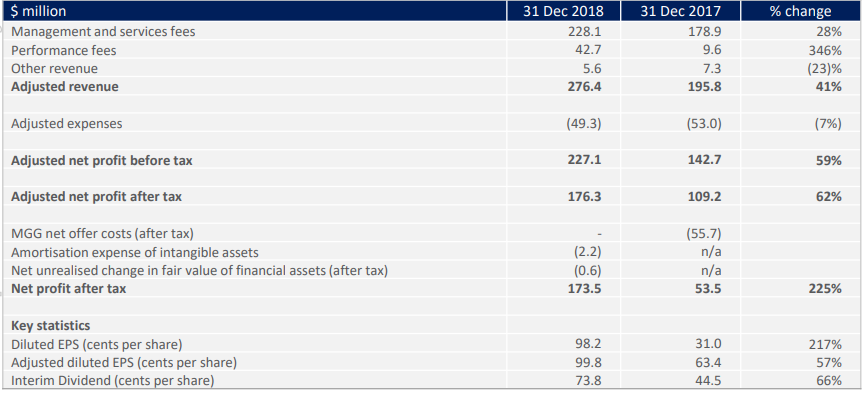

Funds Under Management:As on 31 May 2019, total FUM in Retail amounted to A$ 21,973 million and FUM under Institutional category amounted to A$ 60,786 million.

Financial Highlights: During 1HFY19, Average FUM increased by 35% to $72.1 billion. Retail net inflows during the period amounted to $475 million. The Institutional business also maintained a strong position with $51.8 billion FUM from more than 140 clients. Net Tangible Assets amounted to $534.2 million and Investment Assets stood at $451.4 million.

Interim Results (Source: Company Reports)

Expenses for 2019: Total Group expenses in the financial year 2019 are expected to be approximately $105 million, excluding non-cash amortisation and expense related to Magellan Global Trust Unit Purchase Plan. The company has been aiming to earn satisfactory returns for the shareholders.

Stock Performance: The company’s stock has a price earnings multiple of 24.220x and yielded positive returns of 3.99% and 27.59% over a period of 1 month and 3 months, respectively. Considering the stock performance along with a decent performance during 1H19 in terms of growth in FUM, revenue and profit, robust increase in dividend and a healthy balance sheet position, the company is well positioned to generate good results for its shareholders in the near future. However, the stock is trading closer to its 52-week higher levels. Hence, we give an “Expensive” rating on the stock at the current market price of $47.380 per share (up 3.382% on 11 June 2019).

Commonwealth Bank of Australia

Balance Sheet Strengthened Further:Commonwealth Bank of Australia (ASX: CBA) is one of the leading banks in Australia, providing a wide range of financial services including funds management, superannuation, life insurance, general insurance, etc. The Bank recently updated that it has become an initial substantial holder for Infomedia Limited with total voting rights of 5.05%. The bank updated that 2.00% 5-year Covered Bonds have been suspended from quotation as on 30 May 2019. The Notes will be finally removed from Official Quotation with effect from the close of business on 19n June 2019.

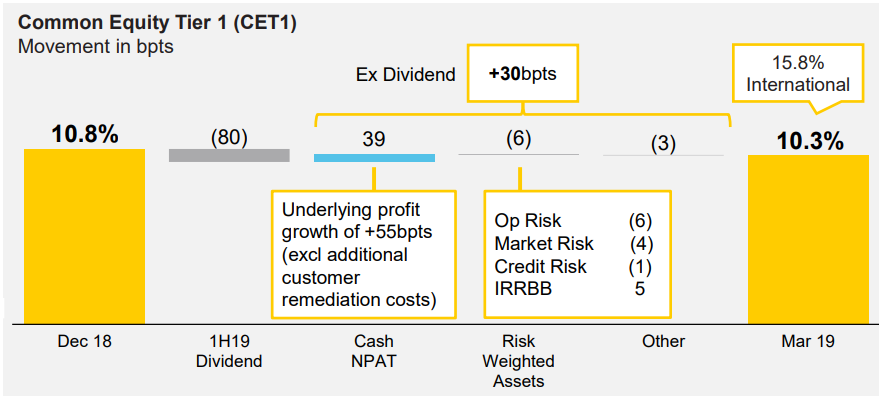

Financial Performance in 3QFY19:Net interest income (NII) witnessed a fall of 3%, on the back of the impact of two fewer days in the quarter. On a day-weighted basis, NII remained flat. Unaudited statutory net profit came in at $1.75 billion in 3QFY19 with cash net profit at $1.70 billion. Capital and balance sheet remained strong, with the Common Equity Tier 1 (capital) ratio at 10.3%. The credit quality remained sound with loan impairment expense of $314 million in the 3QFY19.

CET1 (Source: Company Reports)

Bank’s leverage ratio stood at 5.4% at 31 March 2019 on an APRA basis and 6.2% on an internationally comparable basis.

Leverage Ratio (Source: Company Reports)

Stock Recommendation:At the current market price of $80.950, annual dividend yield for the stock stands at 5.39% with the market capitalization of ~$141.62 billion. Looking at the historical price performance, the stock has gained ~15.5% in the last 1-year and ~7% in the last 1-month. Considering the sustained volume growth, better credit quality, strong funding and liquidity positions with customer deposit funding at 69%, Net Stable Funding Ratio (NSFR) at 113% and other factors, we recommend a “Hold” rating on the stock at the current market price of $80.950 per share (up 1.188% on 11 June 2019).

Ramsay Health Care Limited

Ramsay remains a market leader in Australia:Ramsay Health Care Limited (ASX: RHC) is an operator of private hospitals. In a recent announcement to the exchange, the company notified that Bruce Soden, Finance Director and CFO stepped down from his role during the second half of the year.

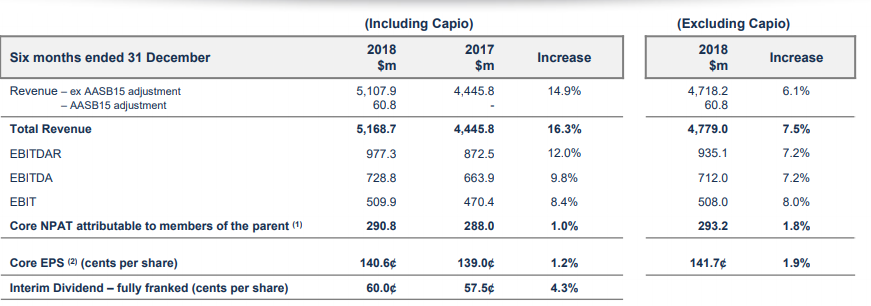

For the half year ended 31 December 2018, the group revenue was reported at $5.1 billion, up 14.9% on pcp and EBITDA amounted to $728.6 million, up 9.8% on pcp, excluding Capio Revenue and EBITDA.

Core net profit after tax amounted to $290.8 million, reporting an increase of 1%. Excluding Capio acquisition, the value stood at $293.2 million, displaying an increase of 1.8%.The company declared an interim dividend of 60 cents (fully franked), which increased 4.3% on the pcp.

While performance in Australia was driven by growth in volume and ongoing focus on operational efficiencies, performance in UK was not that pleasing. Overall, the company remained on track to deliver on its guidance for FY19.

Group Performance in 1HFY19 (Source: Company Reports)

Outlook:Ramsay remains a market leader in Australia with the diversity of its portfolio. The company stated that the long term outlook for the sector is positive. As a result, Ramsay reaffirmed FY19 Core EPS growth of up to 2%, including Capio.

Stock Performance: The company’s stock yielded positive returns of 9.93% and 10.55% over a period of 1 month and 3 months, respectively. Currently, it has a P/E ratio of 35.510x and a market capitalisation of $14.25 billion. 1HFY19 saw an overall decent performance with performance in line with the strategies. The company expanded its global footprints and witnessed decent growth in revenue and profits. Considering the above factors, we give a “Hold” recommendation on the stock at the current market price of $71.460 per share (up 1.319% on 11 June 2019).

Metcash Limited

Second Largest Player in Liquor and Hardware Segments: Metcash Limited (ASX: MTS) is a leading wholesale distribution and marketing company. On 07 June 2019, the company released a notice on change of interests of substantial holder wherein Pendal Group Limited’s voting power was reduced from 11.52% to 10.40%. Earlier in June, Metcash inked a deal with Drakes Supermarkets to supply its stores in Queensland for further five years following the expiry of its existing supply agreement on June 2, 2019.

In a strategy update to the exchange, the company informed about its current position with respect to its divisions – Food, Liquor and Hardware. The company’s Australian Liquor Markets (ALM) is the second largest player in the Australian liquor market. The Food segment has faced significant headwinds in the past 5 years due to intense competition, deflation and roll out of value formats. Year to date total food sales were marginally higher than pcp. With respect to Hardware, the company added that the construction activity has softened but still it is at solid levels.

Current position in various business segments (Source: Company Reports)

Stock Performance: The shares of the company yielded returns of 7.34% and 11.64% over a period of 1 month and 3 months, respectively. The company has been able to report decent sales and earnings growth and is currently accelerating towards growth through its successful strategies. With its strategic framework, the company has been able to deliver significant synergies and is pursuing an attractive growth initiative in the future. Keeping in mind the above factors, we give a “Hold” recommendation on the stock at the current market price of $3.170 per share (up 3.257% on 11 June 2019).

(3).png)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...