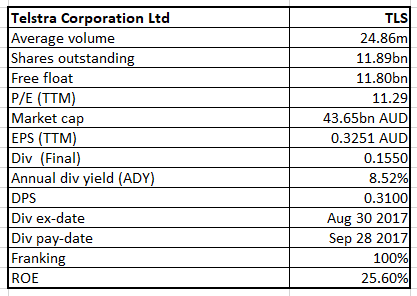

Telstra Corporation Ltd (ASX: TLS)

TLS Details

Half year to witness an impact from Ooyala update: Telstra has recently announced that its first-half result will be impacted by about $273 million at the back of a non-cash impairment and writing off the value of its US intelligent video business, Ooyala to zero. TLS had increased its share of 9% in Ooyala from 2012 to 98% in 2014, however, the woes of the business underperforming amidst challenging conditions were being realised since 2016 with an initial impairment announced in that year. The group’s turnaround efforts on this business were not as successful as expected. While this adds to the growing competition and other issues from nbn, TLS still has the potential given efforts at a larger scale. In December, the group had revised FY2018 guidance as a result of the impact of nbn co.'s announcement to cease sales on hybrid fibre co-axial (HFC) technology for six to nine months from 11 December 2017, as well as nbn co.’s Corporate Plan 2018, wherein the total income was flagged to be $27.6b to $29.5b ($0.7b reduction), EBITDA to be $10.1b to $10.6b ($0.6b reduction), and free cash flow to be $4.2b to $4.7b ($0.2b reduction) with operating output retained as is with a reaffirmation in dividend of 22 cents for fiscal year 2018. On the other hand, the group expects a modest positive financial impact of the delay over the full year nbn roll-out. Most of the shortcomings are already factored in the stock price, which edged a little up on February 02, 2018 despite the news. The valuation scenario is still attractive, and we have a “Buy” on the stock at the current price of $3.67

.png)

TLS Daily Chart (Source: Thomson Reports)

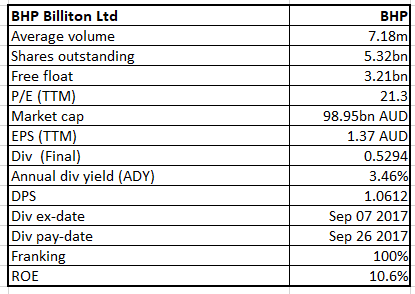

BHP Billiton Ltd (ASX: BHP)

BHP Details

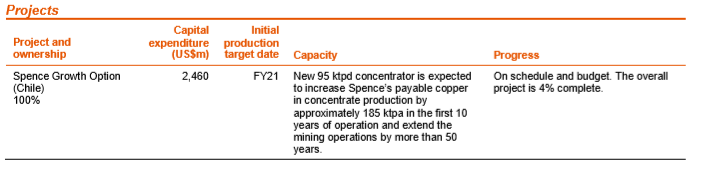

To benefit from commodity scenario: With bullish momentum turning up on commodities, including iron ore, BHP Billiton Ltd like other mining and energy firms moved up about 0.5% on February 02, 2018. The group has been putting efforts on cost management along with bringing a lot of discipline. While the consensus earnings for 2019 have been indicated to be below 2018 levels, the group still has potential to grow given the growth projects in hand (considering approval of an investment of US$2.5bn for the development of the Spence Growth Option). Meanwhile, full year production and unit cost guidance has been maintained for Petroleum, Copper, Iron Ore and Energy Coal; and the group reported a record annualised production rate of 284 Mt (100 per cent basis) at Western Australia Iron Ore (WAIO) for the December 2017 quarter. On the other hand, production guidance for Metallurgical Coal was reduced to between 41 and 43 Mt as a result of challenging roof conditions at Broadmeadow. Nonetheless, given the momentum of the wider portfolio during the second quarter of 2018 with incremental production from latent capacity projects in iron ore and copper, BHP expects a stronger second half operating performance leading to a 6% volume growth for the full year. Meanwhile, the group has earmarked a total of US$181m in further financial support for the Renova Foundation and Samarco until 30 June 2018.

Spence Growth Project (Source: Company Reports)

BHP Stock has risen 17% in last six months (as at February 01, 2018) and is trading at slightly high levels. We give a “Hold” at the current price of $30.81, looking at the potential.

.png)

BHP Daily Chart (Source: Thomson Reports)

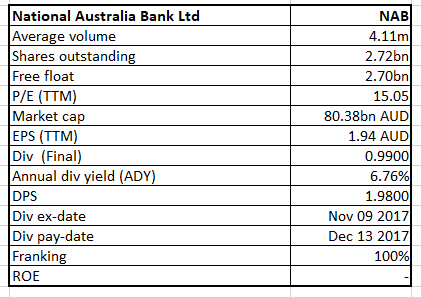

National Australia Bank Limited (ASX: NAB)

NAB Details

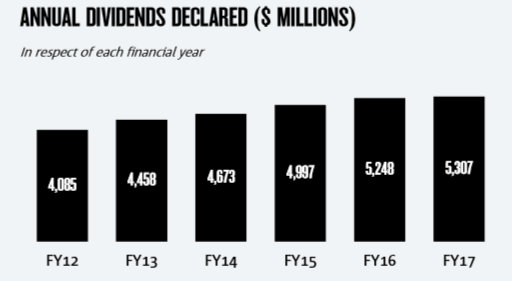

Increased investments for long-term goals: It has been reported that NAB has cut down its 2018 outlook for house prices given the recent Sydney housing market’s deteriorating scenario. It has been reported that NAB Residential Property Index Q4 2017 has led the bank’s capital city house price growth forecast to just 0.7% for 2018 from earlier mentioned 3.4%. This has come at the back of stricter lending credit rules. On the other hand, the bank’s $1.5 billion increased investment over the next three years with a focus on uplifting innovation and capabilities will help in long-term. NAB aims to have increased revenue from higher customer retention and targeted market share gains. In accordance with the plans, NAB expects FY18 expenses to grow 5-8%, with expenses then targeted to remain broadly flat over FY19-20. Therefore, FY18 dividends will be maintained at the FY17 level, subject to no material change in the external environment and satisfactory Group financial performance.

Annual Dividends (Source: Company Reports)

Nonetheless, the group aims to have Net Promoter Score to be positive with cost-to-income ratio towards 35% while becoming #1 ROE of Australian major banks with top quartile employee engagement. The group will be releasing its 1Q FY18 results on February 08, 2018. We maintain a “Buy” at the current price of $29.56

.png)

NAB Daily Chart (Source: Thomson Reports)

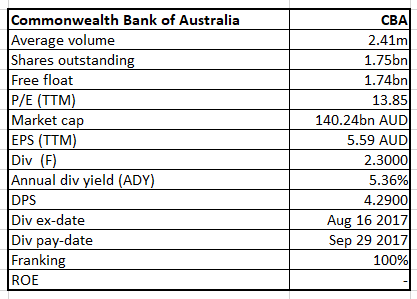

Commonwealth Bank of Australia (ASX: CBA)

CBA Details

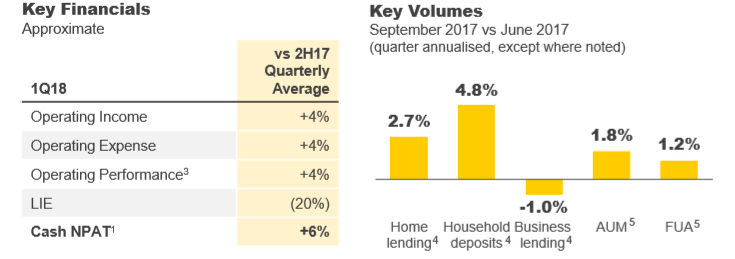

Reputational and regulatory matters encircling the bank: Responding to the amended statement of claim from AUSTRAC wherein an additional 100 alleged contraventions have been pleaded entailing 6 further allegations concerning risk assessments in relation to Intelligent Deposit Machines (IDMs), 56 allegations concerning suspicious matter reports (SMRs) and 38 allegations of concerning ongoing customer due diligence, Commonwealth Bank updated the market about a new risk assessment in relation to IDMs already undertaken in October 2017 and further controls introduced in November 2017. CBA has not specifically commented on many allegations; however, the bank clarified that AUSTRAC has accepted its filed SMRs in relation to the customer engaged with regards to the 38 allegations.

Quarterly Performance (Source: Company Reports)

While the group’s FY17 net profit rose to $9.9 billion, and the strength of earnings enabled the Board to announce an increased total dividend of $4.29, the performance has been camouflaged by many reputational and regulatory matters. For 1Q 18, operating income grew by 4% but at the same time, expense growth was 4% owing to provisions for estimates of future project costs associated with regulatory actions and compliance programs. We give an “Expensive” recommendation on the stock at the current price of $80.79

.png)

CBA Daily Chart (Source: Thomson Reports)

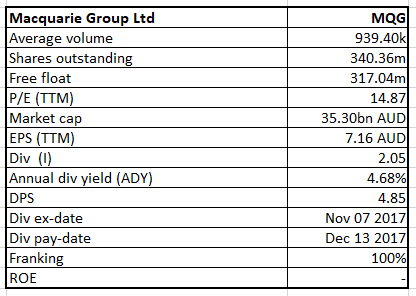

Macquarie Group Ltd (ASX: MQG)

MQG Details

High price run-up: Macquarie Group’s stock has crossed the mark of $100 with a 19.5% rise in stock price over the last six months (as at February 01, 2018). Group’s profit attributable to ordinary equity holders of $A1,248 million for the half-year ended 30 September 2017 increased 19% from $A1,050 million in the prior corresponding period (pcp) and increased 7% from $A1,167 million in the prior period. The interim dividend declared was 205 cents, compared tom 190 cents in pcp. Group’s Asset Management business looks to be well positioned for organic growth with several strongly performing products and an efficient operating platform, while Corporate and Asset Finance business is focussed on asset acquisitions and realisations, subject to market conditions, with funding from asset securitisations. Given the price run-up, we believe that the stock is “Expensive” at the current price of $104.99

.png)

MQG Daily Chart (Source: Thomson Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...