REA Group Limited

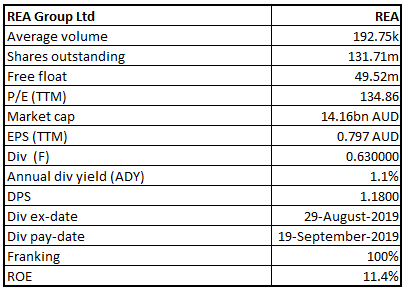

REA Details

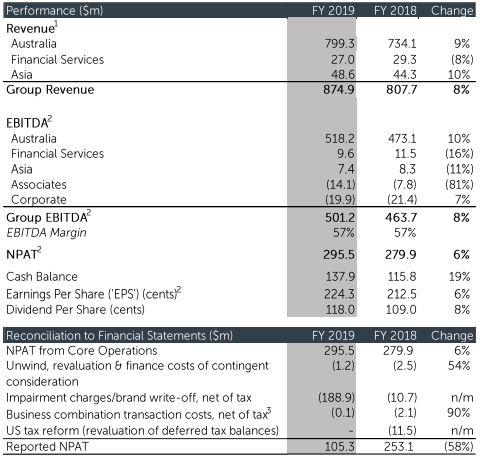

Decent Growth in Revenue: REA Group Limited (ASX: REA) provides property and property-related services on websites and mobile apps throughout Australia and Asia. It has a market capitalisation of A$14.16 Bn as on 26th September 2019. The company recently announced that Tracey Fellows has made a change to its holdings in the company via disposing 9,100 ordinary shares at the consideration of $956,428 on 5th September 2019. Post-change, the number of securities held with Tracey Fellows stood at 7,386 ordinary shares. As per the release dated 9th August 2019, the company updated the market with the results for the year ended 30th June 2019. As per the release, the companyhas delivered growth in challenging market conditions with revenue amounting to $874.9 Mn, reflecting a rise of 8%, due to a rise of 8% in the Australian business. It added that the financial services business delivered revenue amounting to $27.0 Mn, reflecting a decline of 8% as compared to the prior year because of tighter lending conditions as well as subdued property market, which impacted mortgage settlements throughout the industry.

Financial Operating Results (Source: Company Reports)

What to Expect: In the release of FY19 results, the company stated that the listings for 1H FY20 are likely to be lower than 1H FY19because of comparatively favourable listings environment in H1 FY 2019 mainly in Melbourne and Sydney.Therefore, REA anticipates revenue growth to be heavily skewed towards the 2H.

Stock Recommendation:The company stated that the continued revenue growth was achieved despite significant declines in listings and new developments, a clear illustration of the value it delivers to customers and consumers. The Board of the company has declared a fully franked final dividend amounting to 63.0 cps. This brings the total dividend to 118.0 cps for the 2019 financial year, reflecting a rise of 8% on the prior year. On the stock’s performance front, it produced returns of 3.13% and 11.73% in the time period of one month and three months, respectively. Currently, the stock is trading close to its 52-week high levels of $110.480 with PE multiple of 134.86x. Therefore, considering the above-stated facts and current trading levels, we give a “Hold” rating on the stock at the current market price of A$107.400 per share (down 0.074% on 26th September 2019).

.png)

REA Daily Technical Chart (Source: Thomson Reuters)

Ramsay Health Care Limited

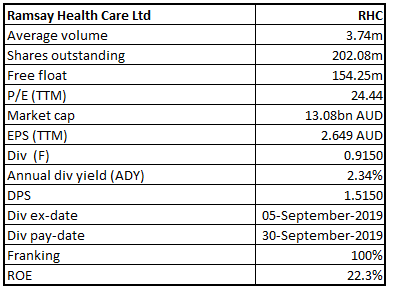

RHC Details

A Brief on Holdings of Paul Ramsay: Ramsay Health Care Limited (ASX: RHC) is a global hospital group, which owns and operates several healthcare facilities throughout Australia, France, Indonesia, Malaysia and the United Kingdom. The market capitalisation of the company stood at A$13.08 Bn as on 26th September 2019. Recently, the company, through a release announced that UBS Group AG and its related bodies corporate ceased to become a substantial holder in the company on 19th September 2019.

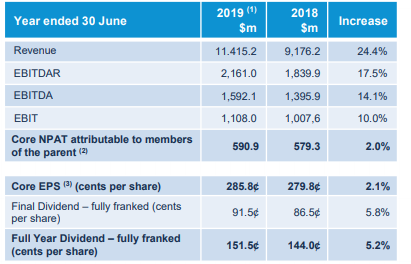

As per the release dated 17th September 2019, the company announced that Paul Ramsay Holdings Pty Limited has wrapped up the underwritten block trade sale of 22 million shares in Ramsay to institutional investors at the consideration of $61.80 per share.The following picture depicts an idea of the key numbers:

Group Performance in FY19 (Source: Company Reports)

Future Prospects:The company has adopted new lease accounting standard AASB16, which became effective from 1 July 2019. It added that there would be no impact on net cash flow, debt covenants and debt facility headroom by the adoption of the standard. However, it would have a significant non cash impact on the consolidated income statement and consolidated statement of financial position for FY20.

Stock Recommendation:The return on equity of the company stood at 22.3% in FY19 as compared to the industry median of 11.9%. This implies that RHC is providing better returns to shareholders as compared to the broader industry. It reported a net margin of 5.0% against the industry median of 3.6%, which reflects that the company has better capabilities to convert its top-line into bottom-line when compared to the industry. Currently, the stock is trading slightly below the average of 52 weeks high and low levels of $74.12 and $51.89, respectively with reasonable PE multiple of 24.44x and an annual dividend yield of 2.34%. Hence, considering the above-stated facts, we give a “Buy” recommendation on the stock at the current market price of A$64.030 per share (down 1.097% on 26th September 2019).

RHC Daily Technical Chart (Source: Thomson Reuters)

Transurban Group

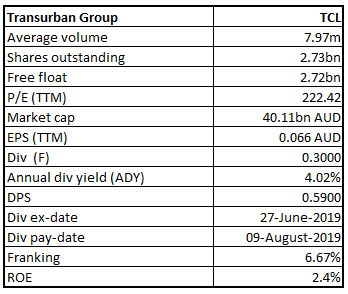

TCL Details

Completed Share Purchase Plan: Transurban Group (ASX: TCL) is owner, operator and developer of electronic toll roads and intelligent transport systems. It has a market capitalisation of A$40.11 Bn as on 26th September 2019. Recently, the company announced that Louis Scott Charlton has made a change to its holdings in the company via acquiring 1,025 stapled securities at the price of $14.64 per security on 6th September 2019. As per the release dated 4th September 2019, the company announced that it has wrapped up the security purchase plan following the closing of the SPP on 30 August 2019.

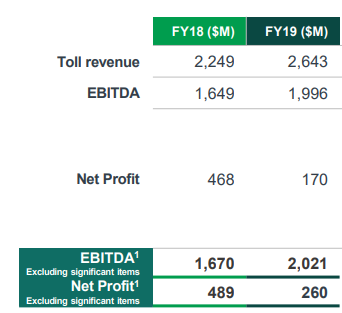

The SPP raised a total of $312 Mn, with around 21.3 million SPP securities to be issued at an issue price of $14.64 per security.TCL has also completed $500 million ‘pro-rata’ institutional placement. The proceeds raised from the Placement and the SPP would be used to finance the acquisition of the remaining 34.62% interest in M5 West. The following provides an idea of statutory results of the company:

Statutory Results (Source: Company Reports)

Future Aspects: The near-term priorities include to (1) Deliver committed projects, (2) Maximise the performance of operations, and (3) Enhance customer and community offerings. The company gave distribution guidance of 62.0 cps for FY20, which includes 4.0 cps fully franked.

Stock Recommendation: The company stated that its continued focus on delivery and execution has seen the opening of new capacity on four major projects over the year, delivering valuable travel-time savings for customers. On the stock performance front, it produced returns of 14.04% and 30.20% in the past six months and one year, respectively. Currently, the stock is trading slightly towards its 52 weeks high price of $16.06 with PE multiple of 222.42x and an annual dividend yield of 4.02%. Thus, considering the above-stated facts and current trading levels, we give a “Hold” rating on the stock at the current market price of A$14.630 per share (down 0.341% on 26th September 2019).

.png)

TCL Daily Technical Chart (Source: Thomson Reuters)

BHP Group Limited

BHP Details

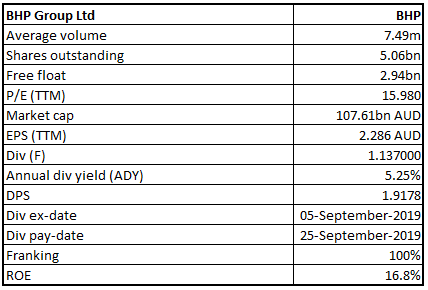

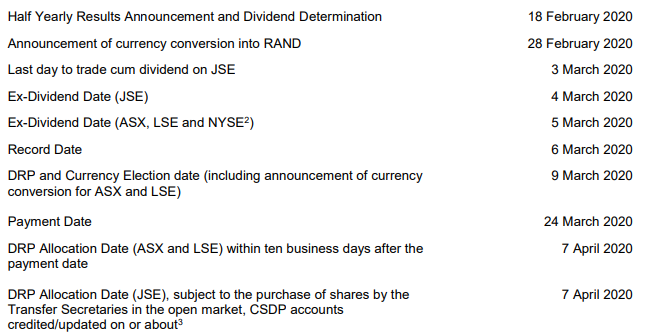

Dividend Date Announced: BHP Group Limited (ASX: BHP) is into minerals exploration, production and processing (particularly coal, iron ore, copper and manganese ore) and hydrocarbon exploration, production and refining. The market capitalisation of the company stood at A$107.61 billion as on 26th September 2019. Recently, the company has announced its interim dividend record date on 6th March 2020 and payment date on 24th March 2020. The company will announce its half yearly results and dividend determination on 18th February 2020.

2020 Interim Dividend (Source: Company Reports)

FY19 Highlights: In FY19, the company’s financial performance from continuing operations were strong. Higher prices and solid underlying performance contributed to EBITDA of US$23 billion at a margin of 53 percent. Underlying attributable profit was US$9.5 billion. The company generated strong operating cash flows consistently and delivered a further US$17 billion in FY19. The company used this cash to pay down debts, deliver record cash returns to shareholders and to progress attractive growth projects. The Board decided to give a dividend of 78 US cents per share as final dividend.

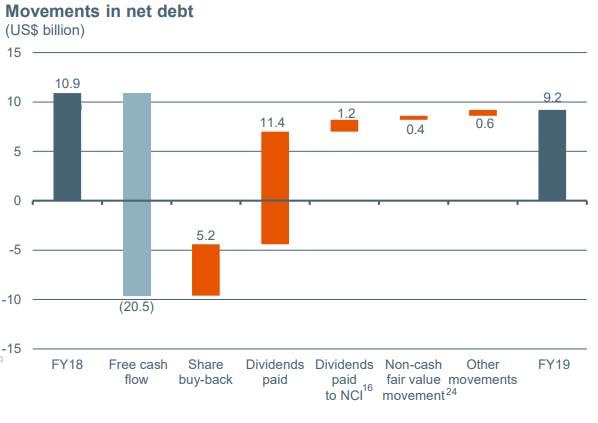

Movements in Net Debt (Source: Company Reports)

In July 2019, the company announced a five-year US$400 million Climate Investment Program to find the best technologies, investments and solutions to reduce greenhouse gas emissions across the value chain.

Stock performance:On the stock’s performance front, it produced returns of -11.42% and -1.62% in three and six months, respectively. Currently, the stock is trading slightly towards its 52-week high level of $42.33 with P/E multiple of 15.980x and an annual dividend yield of 5.25%. Hence, considering the aforesaid facts coupled with uncertainties in a global trade war and current trading levels, we give a “Hold” rating on the stock at the current market price of A$36.500 per share (down 0.082% on 26 September 2019).

BHP Daily Technical Chart (Source: Thomson Reuters)

Australia and New Zealand Banking Group Limited

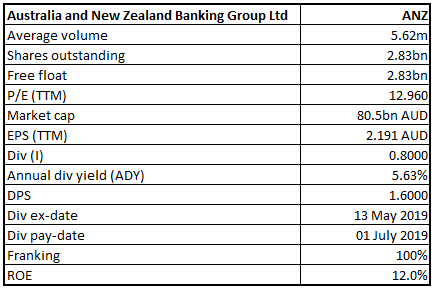

ANZ Details

ANZ to Focus on Institutional and Large Corporate Banking: Australia and New Zealand Banking Group Limited (ASX: ANZ) provides banking and financial products and services to individual and business customers. The market capitalisation of the bank stood at A$80.5 billion as on 26th September 2019.

ANZ announced that it has completed the sale of its Retail, Commercial and Small-Medium Sized Enterprise (or SME) banking businesses in Papua New Guinea to Kina Bank. This will allow ANZ to focus on its Institutional and Large Corporate banking business in the country.

Change in Company Secretary: Ken Adams has been appointed as the Company Secretary of ANZ. And, Bob Santamaria and John Priestley have ceased to be Company Secretaries of the bank.On May 21, 2019, ANZ announced the appointment of Mr Adams as the New Group General Counsel commencing from August 19, 2019 with Mr Santamaria retiring from ANZ on 30th September 2019.

ANZ Sells its Stake in ANZ Royal: ANZ has completed the sale of its 55% stake in Cambodian joint-venture ANZ Royal Bank to J Trust,which is in line with ANZ’s strategy to simplify its business and operate wholly-owned Institutional businesses in the region.

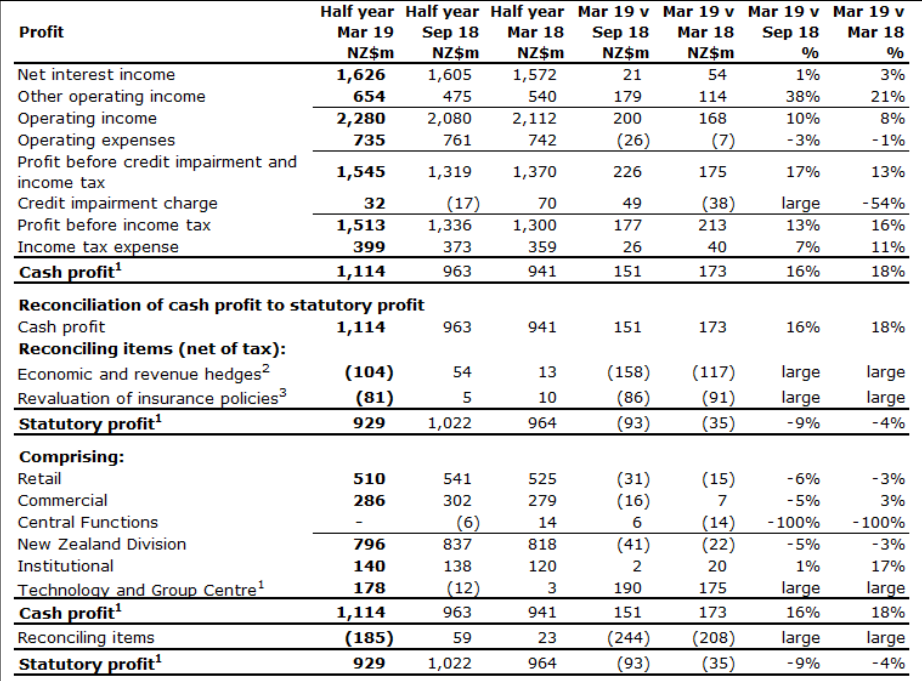

ANZ New Zealand Half Yearly Results: ANZ Bank NZ reported a statutory net profit after tax of NZ$929 million for the six months to 31st March 2019, which is a decrease of 4% on the corresponding half in the 2018 financial year. Cash NPAT was up by 18% to NZ$1,114 million, because of one-off transactions, which included the sale of life insurance company OnePath Life (NZ) Limited and a 25% share in Paymark Limited.

Financial Information (Source: Company Reports)

Stock Recommendation:The stock produced returns of -0.18% and 9.57% in the time period of three months and six months, respectively. Currently, the stock is trading close to 52-week high price of $29.30 with PE multiple of 12.96x and an annual dividend yield of 5.63%. Hence, in view of aforesaid facts and current trading levels, we give a “Hold” recommendation on the stock at the current market price of A$28.400 per share.

.png)

ANZ Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...