Insurance Australia Group Limited

.png)

IAG Details

Providing service to a huge customer base: Insurance Australia Group Limited (ASX: IAG) has established a strong Product & Services Platform that caters to 8.5 million direct customers. The group is also targeting to simplify its business and report at least $250 million reduction in the controllable costs post FY19 (reducing the cost base to $2.25 billion from $2.5 billion). Meanwhile, IAG informed the ASX that they have changed their registered head office address and postal address. The group posted strong profit growth of 23.5 per cent to $551 Mn in 1HFY18. This was mainly driven by rate increases in commercial and consumer line, and volume growth in the motor division. Cash net profit after tax (Cash NPAT) grew by 31.5 per cent to $630 million, while cash return on equity (RoE) increased 430 bps over the same period.

.png)

1HFY18 Result Highlights (Source: Company Reports)

Based on the robust performance in 1HFY18, the Board of Directors declared fully franked interim dividend of 14.0 cents per share which was paid on March 29, 2018, representing a pay-out ratio of 52.5% of cash earnings and dividend rise of 7.7% as compared to previous corresponding period. Looking at historical dividend performance, the company is expected to maintain its dividend pay-out ratio in the range of 60%-80% of cash earnings on a full year basis. Meanwhile, IAG stock has risen 29.60 per cent in the past one year as on June 07, 2018 and is trading close to 52-week higher level. Hence, we maintain our “Hold” recommendation on the stock at the current price of $ 8.010, in view of the expected full financial year performance.

.png)

IAG Daily Chart (Source: Thomson Reuters)

Commonwealth Bank of Australia

.png)

CBA details

CBA Agreed to Pay Civil Penalty of $700 Mn: Commonwealth Bank of Australia (ASX: CBA) has entered into an agreement with AUSTRAC (Australian Transaction Reports and Analysis Centre) to resolve the civil proceedings commenced by AUSTRAC in the Federal Court of Australia in August 2017. Under the terms of the agreement, the Group will have to pay a civil penalty (of $700 million) against non-compliance of its anti-money laundering and counter-terrorism financing (AML/CTF) laws in order to resolve Federal Court proceedings. Both parties will together approach the Federal Court of Australia seeking orders to this effect. It is expected that a hearing on penalty will be arranged in the coming months. If the court agreed on the aforesaid penalty, then this will be a largest-ever civil penalty in Australian corporate history. However, this action will send a strong message to other players within the same industry that serious non-compliance with the AML/CTF Act will not be tolerated anymore. Beside this, CBA has committed to building on the significant changes made in recent years as part of a comprehensive program to improve operational risk management and compliance at the bank. To date, the group has spent more than $400 Mn on the systems, processes, and people relating to AML/CTF compliance and will continue to prioritize investment in this area. These important steps are part of the large and energetic effort to become a better, stronger bank resulting into gaining trust of its customers, staff, regulators and shareholders. On the other hand, CBA made a provision of about $375 Mn as an estimated penalty in the first half of the year as the bank realised that the proceedings were complex and ongoing, and the ultimate penalty determined by the Court could be higher or lower than the amount provided for.

.png)

Q3FY18 Key Highlights (Source: Company Reports)

Meanwhile, the stock has fallen 12.30% in past six months and further down by 4.74% in the past one month as on June 07, 2018. Hence, we maintain our “Expensive” recommendation on the stock at the current price of $ 69.370, considering civil penalty to pay $700 Mn to Federal Court which can impact the bottom line of the company for the full year.

.png)

CBA Daily Chart (Source: Thomson Reuters)

Suncorp Group Limited

.png)

SUN Details

Enhancing customer experience: Suncorp Group Limited (ASX: SUN) has recently posted its quarterly update as at 31 March 2018 wherein total lending marginally increased by 0.9 per cent over the quarter, representing a moderation in growth compared to the first half of the financial year and contributing to the financial year-to-date growth of 5.4%. Further, the management stated that this result reflects its commitment to responsible and sustainable lending practices, as well as its focus on enhancing customer experience to drive growth. Moreover, moderate growth in the home lending portfolio of $361 Mn or 0.8% for the quarter, was achieved through its consistent price and service offerings. We expect that the group will continue to drive sustainable, profitable growth through increased investment in its digital self-service and payment capabilities to better meet customer needs. This includes the recent introduction of two digital wallets, as well as new self-service security features.

.png)

Portfolio Composition (Source: Company Reports)

Due to rise in competition within the industry, the company’s operating targets are unchanged. In order to do this, the group is still targeting a banking cost to income ratio of around 50%, subject to regulatory reform costs, and its Net Interest Margin will be around 1.80% to 1.90% for FY19. Further, the Board of Directors declared a fully franked interim dividend of 33 cents per share, representing a dividend payout ratio of 90.1% of cash earning. After payment of the dividend, the franking account balance will be $158 Mn. The Group is well capitalized with $381 million in CET1 capital held above its operating targets. Suncorp remains committed to returning excess capital to shareholders. Moreover, the Board expects to maintain a dividend payout ratio of 60% - 80% of cash earnings and return surplus capital to shareholders. Meanwhile, the stock price was up by 3.87 per cent in the past five days and SUN is trading at slightly high levels. Hence, we put a “Hold” recommendation on the stock at the current market price of $14.030.

.png)

SUN Daily Chart (Source: Thomson Reuters)

Transurban Group

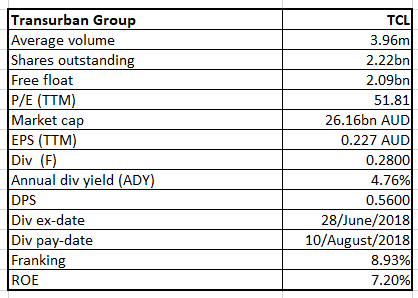

TCL Details

Healthy Performance: Transurban Group (ASX: TCL) informed the market that the group reached its financial close on its acquisition of the A25 toll road asset as the company announced earlier to acquire 100% of equity interest in the A25 for C$840 Mn. The management expects that this acquisition marks an important step for the business as it establishes its second market in North America. The Group will assume responsibility for the management and operations of the A25 after the financial close, which is targeted for Q4 FY18, subject to an Investment Canada Act approval. In the past five years, the group has invested more than $16 billion into enhancing urban road networks across Australia and the Greater Washington Area to give people more transport options.

.png)

North American Opportunities (Source: Company Reports)

On the financial front, the group has recorded Proportional toll revenue growth of 10.5% in 1HFY18 and this amounted to $1,176 Mn as compared to the previous corresponding period (pcp). Toll revenue surged up in view of traffic growth and toll price escalation during the same period. EBITDA stood at $911 Mn, showing a growth of 10.3% on Year-On-Year (YoY) basis along with EBITDA margin recorded at 75.4%, gaining by 70bps. Statutory PAT is at $331 Mn, showing strong growth of 276.1% on YoY basis at the back of favourable movements in net finance costs and non-cash income tax benefits. Based on robust performance in first half, the management guidance on distribution has been around 56.0 cps for the full year which is reflected as a growth of 8.7% over FY17. Meanwhile, the stock prices were down by 4.95 per cent in the past six months (as at June 07, 2018) and TCL is trading slightly above the 52-week lowest level. Hence, we maintain our “Buy” recommendation on the stock at the current market price of $ 11.67, based on group’s strong financial performance, network expansion plan, disciplined investment approach, increasing traffic growth across the networks, and North American Opportunity.

.png)

TCL Daily Chart (Source: Thomson Reuters)

Telstra Corporation Limited

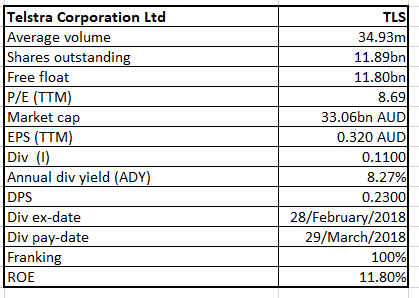

TLS Details

Uncertainty around FY18 Dividend guidance: After enjoying a market leading position in the telecom sector, Telstra Corporation Limited (ASX: TLS) has been on a downturn lately. Many experts also discuss about a possible split of the business. Meanwhile, the group is working on cost reduction initiatives and this along with step change of technology to 5G may help the group. Though earnings gap owing to nbn is what investors are worried about along with rise in competition from players like TPG Telecom, TLS has reaffirmed its FY18 total dividend to be 22 cents per share fully franked including ordinary and special dividend. The group maintains a dividend policy to pay a fully franked dividend of between 70% to 90% of underlying earnings from FY18. Additionally, the group intends to return in the order of 75% of future net one-off nbn receipts to shareholders over time through fully franked special dividends. All in all, the long-term growth or even sustenance of dividends would depend on the arrival of 5G, other investments and impact from nbn.Further, the group reaffirmed FY18 guidance and expects income of $27.6 Bn to $29.5 Bn for the full year while EBITDA is expected in the range of $10.1 Bn to $10.6 Bn after absorbing incremental restructuring costs for the same period. During the first half, the group enhanced its cyber securities services with the opening of two new Security Operations Centres in Melbourne and Sydney and further, they have planned to open another Security Operations Centre in London. This will help build a new growth opportunity in the core business in the upcoming period. In the past one year, the stock has declined by 37.04% and is trading at its 52-week low levels. As of now, we give a “Hold” recommendation on the stock at the current market price of $ 2.770, considering intense competition and recent outages in its network across Australia.

.png)

TLS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...