.png)

Stocks’ Details

Suncorp Group Limited

Strong Rise in Group NPAT: Suncorp Group Limited (ASX: SUN) is involved in the provisioning of banking, wealth, insurance and other financial solutions. The market capitalisation of the company stood at $14.44 Bn as on 6th March 2020. For 1H FY20, the group reported net profit after tax amounting to $642 Mn with a rise of 156.8% over pcp. This includes the profit after tax of $293 Mn from the divestment of Capital S.M.A.R.T and ACM Parts to AMA Group Limited. This reflects improved unit trajectory in consumer lines flowing from the creation of virtual brand teams as well as targeted marketing campaigns.

For the same period, the Board declared fully franked interim dividend of 26 cents per share. Five years (FY15-FY19) average dividend yield of SUN stood at 5.33% with the annual dividend yield of 6.11% at the current market price of $11.230 per share.

.png)

Financial Metrics (Source: Company Reports)

Focus for Remaining FY20:In 2H FY20, the focus of SUN primarily revolves around improving the performance of its core businesses and leveraging its investment in digital and data. For, FY20 the company anticipates NIM (Net Interest Margin) in the ambit of 1.85% - 1.95%.

Valuation Methodology: P/BV Multiple Based Valuation

.png)

P/BV Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: SUN is planning to maintain an ordinary dividend payout ratio policy of 60-80% of cash earnings. During 1H FY20, the group experienced strong GWP (Gross Written Premium) growth in New Zealand, which was fueled by the direct and partner channels. We have valued the stock using P/BV based relative valuation approach and arrived at a target price, which is offering an upside of high single digit (in percentage terms). Therefore, considering the strong growth in GWP and consistent payment of dividend, we give a “Buy” recommendation on the stock at the current market price of $11.200 per share, down by 2.183% on 6th March 2020.

Super Retail Group Limited

Decent Growth in Topline: Super Retail Group Limited (ASX: SUL) operates specialty retail stores in the automotive, tools, leisure and sports categories. The market capitalisation of the company stood at $1.56 Bn as on 6th March 2020. Recently, Director Sally Anne Majella Pitkin has made a change to holdings in the company on 4th March 2020 by acquiring 5,000 ordinary shares at the consideration of $40,042.34. Even with the impact of bushfires and drought on the peak trading period, the company managed to deliver total sales amounting to $1.44 billion during 1H FY20, reflecting the growth of 2.9% on pcp.

The group declared fully franked interim dividend of 21.5 cents per share, which is in-line with the pcp. The annual dividend yield of the company stood at 6.34% at the current market price of $7.660 per share, which is higher than the industry median (Consumer Cyclicals) of 4.8% on TTM basis.

.png)

Group Results (Source: Company Reports)

Focus on Organic Growth: The company is focused on organic growth and capital discipline. Its focus area includes group sourcing optimisation as well as 5-year supply chain strategy.

Valuation Methodology: P/BV Multiple Based Valuation

.png)

P/BV Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: SUN attained strong gross margin momentum in the Q2 FY20. Moreover, the company reported a strong operating cash flow of $239.1 million, which is supporting a reduction of $42.2 million in net debt. We have valued the stock using P/E based-relative valuation approach and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Thus, considering the strong gross margin momentum, growth in top-line and valuation, we give a “Buy” recommendation on the stock at the current market price of $7.660 per share, down by 2.915% on 6th March 2020.

Event Hospitality and Entertainment Ltd

Decent Set of Financials in 1H FY20: Event Hospitality and Entertainment Ltd (ASX: EVT) is involved into motion picture exhibition and operates various hotels and restaurants. Group reported a growth of 2% to $524 million in revenue from continuing operations during 1H FY20. Its statutory net profit after tax, including discontinued operations stood at $93.6 million, up 38.7% on pcp. These results have been underpinned by strong results from the Entertainment group with adjusted profit growth of 7.4%; continued strong results from the Hotels division in a more competitive market; and a good result from Thredbo in spite of less favourable ski conditions.

Fully franked interim dividend for the period was 21 cents per share. The annual dividend yield of the company stood at 4.88% at the market price of $10.230 per share along, with a five-year average dividend yield (FY15-FY19) of 3.80%.

.png)

Financial Overview (Source: Company Reports)

Impact on Hotel Division: Due to coronavirus outbreak, the Hotels division would be impacted by the Government travel restrictions and suspended airline services. For the same division, the company is expecting earnings for March 2020 in the range of $2 million to $3 million.

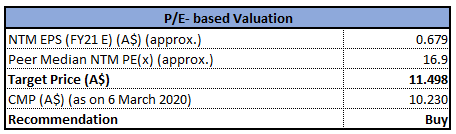

Valuation Methodology: P/E Multiple Based Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The company reported a rise of 30% in normalised profit of New Zealand circuit. The company expects total consideration of €186.9 million from the sale of German division, which includes an earn-out of €56.9 million. We have valued the stock using P/E based relative valuation approach, and for the purpose, we have taken peers such as Ardent Leisure Group Ltd (ASX: ALG), Village Roadshow Ltd (ASX: VRL), Crown Resorts Ltd (ASX: CWN) etc., and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Therefore, in light of the growth in statutory net profit after tax, and performance of New Zealand Circuit, we give a “Buy” recommendation on the stock at the current market price of $10.230 per share, down by 4.034% on 6th March 2020.

Bank of Queensland Limited

Refreshed Five-Year Strategy: Bank of Queensland Limited (ASX: BOQ) is a well-known bank of Australia with a market capitalisation of $3.28 Bn as on 6th March 2020. Recently, the bank refreshed its five-year strategy, which includes maintaining a strong financial and risk position, with attractive returns, creating a simple and intuitive business, with strong execution capability, becoming a digital bank of the future with a personal touch etc.BOQ is continuing its capital investment of around $100 million per annum before reducing to around $80 million in FY23 and $60 million in FY24.

For FY19, the bank declared a total dividend of 65 cents per share. Atthe current market price of $6.930 per share, the annual dividend yield stood at 9.730% as compared to 5.4% of industry average (Banking Services) on TTM basis.

Financial Metrics (Source: Company Reports)

Target for Growth in Dividend: The Bank is aiming sustainable growth in EPS and dividends beyond FY21. It is targeting a dividend payout ratio in the range of 70%-80% of cash earnings. The banks expect cash earnings of FY20 to be 4% to 6% lower than FY19.

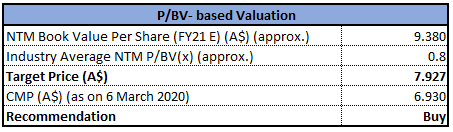

Valuation Methodology: P/BV Multiple Based Valuation

P/BV Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The bank would be focused on quality lending, as well as good margin management financed through a mix of sources which includes a high level of retail deposits. Moreover, it is targeting return on equity of 8% by FY22. We have valued the stock using P/BV based relative valuation approach, and for the purpose, we have taken peer such as Bendigo and Adelaide Bank Ltd (ASX: BEN), National Australia Bank Ltd (ASX: NAB), Westpac Banking Corp (ASX: WBC) etc., and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Hence, considering the refreshed five-year strategy and expected growth in dividend, we give a “Buy” recommendation on the stock at the current market price of $6.930 per share, down by 4.017% on 6th March 2020.

IOOF Holdings Limited

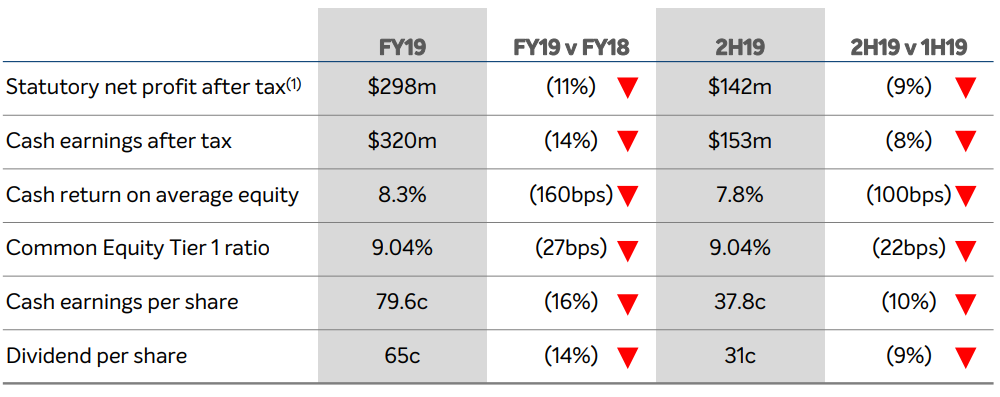

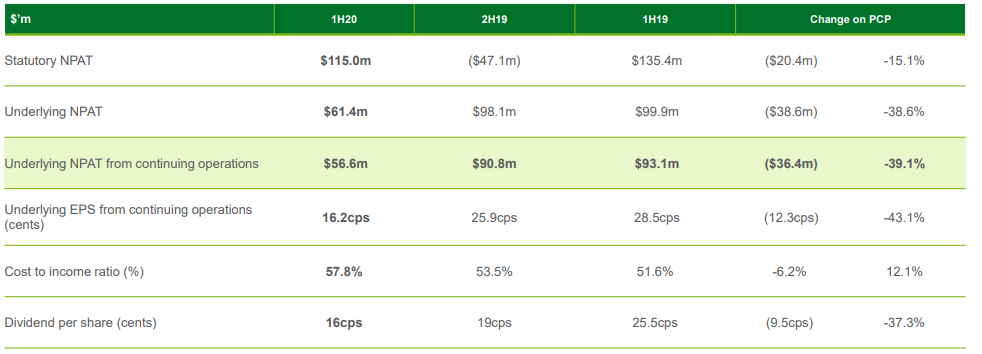

1HFY20 FUM Growth at 5.2%: IOOF Holdings Limited (ASX: IFL) is mainly involved in financial advice and distribution and portfolio and estate administration. Recently, the company has responded towards class action proceedings by Shine Lawyers. The class action is on behalf of certain shareholders of IOOF who acquired an interest in IFL between 1 March 2014 and 7 July 2015. However, the company intends to defend the proceedings.

For 1H FY20, funds under management, advice and administration witnessed a rise of 5.2% to $145.7 billion. The statutory net profit after tax for the period stood at $115.0 million, and it posted underlying net profit after tax from continuing operations amounting to $56.6 million. The result indicates the company’s recent focus in reshaping the business for the upcoming opportunities. The Board of the company declared fully franked interim dividend amounting to 16 cps. At the current market price of $5.350 per share, the annual dividend yield of the company stood at 4.9%.

Financial Results (Source: Company Reports)

Expected Financial Benefits: The company expects significant financial benefits from the step-change in scale and the synergy opportunities, which are underpinning its capability to lower the longer-term cost base of the combined businesses while allowing for continued reinvestment.

Valuation Methodology: P/BV Multiple Based Valuation

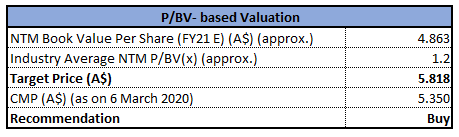

P/BV Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: During 1H FY20, the company has wrapped up the acquisition of ANZ Pensions and Investments at the re-negotiated sale price of $825 million. Debt to equity of the company stood at 0.26x in 1H FY10 as compared to the industry median of 0.64x. This reflects that the company has stable balance against the peer group. We have valued the stock using P/BV based relative valuation approach and arrived at a target price of high-single digit (in percentage terms). Thus, taking into account the growth in FUM, deleveraged balance sheet and valuation, we give a “Buy” recommendation on the stock at the current market price of $5.350 per share, down by 6.305% on 6th March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...