Stocks’ Details

AGL Energy Limited

Growth in Customer Accounts: AGL Energy Limited (ASX: AGL) is engaged in the operation of energy businesses and investments, including electricity generation, gas storage and the sale of electricity and gas to residential, business and wholesale customers. The market capitalisation of the company stood at $10.56 Bn as on 29th June 2020. The company recently appointed Mark Bloom as a Non-Executive Director, effective 1 July 2020. The company has also bought back a total of 32,686,947 shares at a consideration of $620,417,272.58. Despite the uncertainty caused by COVID-19, the customer metrics are positive. The company added that the customer accounts have grown by more than 28,000 since 31 December 2019. National electricity demand was broadly stable despite COVID-19, and the reductions have been driven by milder weather.

.png)

Customer Accounts (Source: Company Reports)

Guidance: For FY20, the company expects underlying profit after tax in the range of $780 million to $860 million despite the recent increase in customer bad debt expense and other unanticipated operating costs arising from COVID-19 lockdown. However, the guidance is subject to no further deterioration in market conditions or regulatory impacts on operations.

Key Risks: The company’s business is sensitive to strategic risks, which include market disruptions, Government intervention, climate change and investment decisions. Market disruptions are associated with the inability of the company to meet changing customer expectations and preferences regarding energy sources, prices and related products and services.

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

.png)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: AGL possesses a strong balance sheet and decent liquidity with cash and undrawn facilities of around $1 billion. The company also has a decent capacity to finance growth from organic cash flows. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers like AusNet Services Ltd (ASX: AST), Infigen Energy Ltd (ASX: IFN), etc. Therefore, considering the growth in customer accounts despite COVID-19, healthy balance sheet, and decent liquidity position, we give a “Buy” recommendation on the stock at the current market price of $16.500 per share, down by 2.367% on 29th June 2020.

Spark Infrastructure Group

AER Final Decision: Spark Infrastructure Group (ASX: SKI) owns a diversified portfolio of quality essential service infrastructure. The market capitalisation of the company stood at $3.7 Bn as on 29th June 2020. Recently, the company has noted the Australian Energy Regulator (AER) Final Decision for the next five-year regulatory period for SA Power Networks, in which Spark Infrastructure holds a 49% interest. The AER has approved key financial outcomes to apply for the 5-year regulatory period commencing 1 July 2020 to 30 June 2025, which include, the nominal smoothed revenue allowance of $3,914 million and rate of return of 4.75%.

.png)

Key Financial Outcomes (Source: Company Reports)

Reiterated Distributed Guidance: The objective of the company revolves around delivering long-term value via capital growth and distributions to security holders from its portfolio of high-quality, long-life essential services infrastructure businesses. For FY20, the Board of the company has the reiterated distribution guidance of a minimum 13.5 cents per share.

Key Risks: The company is exposed to climate change risk and to mitigate it, the company would adopt the Task Force on Climate related Financial Disclosures (TCFD) in the future. The energy industry is currently experiencing unprecedented change and uncertainty, and this proves as a major industry risk for the company. Over the last few years, the entire industry has been subjected to intense scrutiny, which has led to a continual stream of reviews, regulatory change and government interventions.

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

.png)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The company has achieved an average payout ratio of 71% of look-through net operating cash flows over the last four years. Net margin of the company stood at 29.0% in FY19 as compared to the industry median of 18.6%. This indicates that the company has decent capabilities to convert its top-line into the bottom-line against the broader industry. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers like Contact Energy Ltd (ASX: CEN), Mercury NZ Ltd (ASX: MCY) and Meridian Energy Ltd (ASX: MEZ). Thus, considering the reiterated distribution guidance, decent capabilities to convert its top-line into the bottom-line, and current trading levels, we give a “Hold” recommendation on the stock at the current market price of $2.150 per share on 29th June 2020.

Mercury NZ Limited

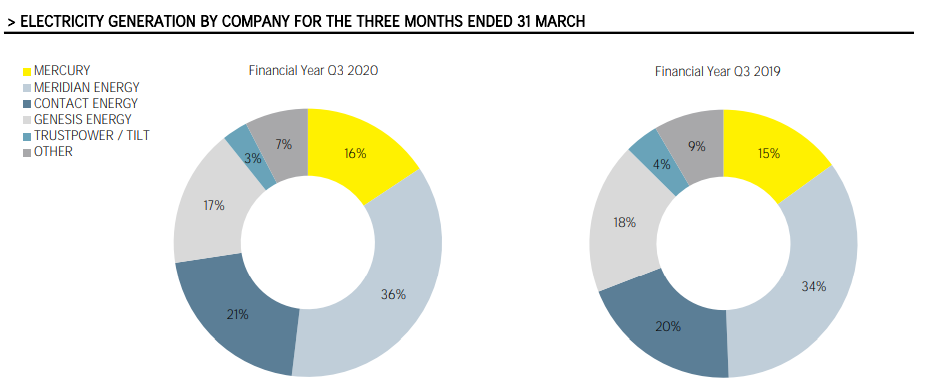

A Look at Q3 FY20 Update:Mercury NZ Limited (ASX: MCY) is engaged in retailing and generation of electricity. The market capitalisation of the company stood at $6.13 Bn as on 29th June 2020. As per the recentquarterly rebalance provided by S&P Dow Jones Indices, the company has been added to All Ordinaries, which became effective on 22nd June 2020. The company has recently released its operational update for the quarter ended 31st March 2020, wherein, it stated that its robust business continuity planning has allowed a smooth transition to operating under the COVID-19 lockdown. MCY’s high Taupo storage position at the start of the period enabled increased hydro generation despite significantly below-average inflows.

The company’s continued focus on customer value has resulted in the Commercial & Industrial average sales yield of NZ$92/MWh during Q3 FY20, reflecting a rise of 12.7% from NZ$82/MWh in Q3 FY19.

Electricity Generation (Source: Company Reports)

Revised Guidance:For FY20, the company has revised its EBITDAF guidance from NZ$490 million to NZ$480 million, which indicates an anticipated 100 GWh decline in full-year hydro generation to 3,700 GWh due to continued dry weather conditions in the Taupo catchment in FY20.

Key Risks:Mercury NZ Limited is exposed to various climate change scenarios such as changing rainfall patterns across different time scales, which can impact generation operations and generation assets. The company is also exposed to price risks from energy contracts that establish a fixed price at which future specified quantities of electricity are purchased and sold. In addition, regulations in New Zealand, such as the Zero Carbon Bill, renewable energy targets, and a revised Emissions Trading Scheme have implications for the business.

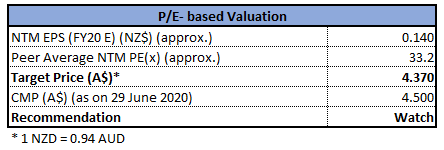

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: Debt to equity multiple of the company stood at 0.36x in 1H FY20 as compared to the industry median of 0.46x. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a price correction of low single-digit (in percentage terms).For the purpose, we have taken peers such as AusNet Services Ltd (ASX: AST), Spark Infrastructure Group (ASX: SKI), Genesis Energy Ltd (ASX: GNE), etc. Hence, considering the anticipated 100 GWh decrease in full year hydro generation and expected correction in price, we have a wait and watch stance on the stock at the current market price of $4.500 per share on 29th June 2020.

Infigen Energy

Updated Takeover Offers: Infigen Energy (ASX: IFN) is engaged in the generation of renewable energy from its fleet of owned wind farms. The market capitalisation of the company stood at $859.07 Mn as on 29th June 2020. Recently, the company has received updated takeover offers from UAC Energy Holdings Pty Ltd (UAC) and Iberdrola Renewables Australia Pty Limited, wherein UAC has removed its bid conditions, and increased the price offered to 86 cents per Infigen Stapled Security and accelerated the payment terms to Infigen Security Holders, while Iberdrola has varied its conditional off-market takeover offer first announced on 17 June 2020 to increase the price offered to 89 cents per Infigen Stapled Security.

As of now, IFN’s Board has advised the security holders to take no action with respect to the updated offers. The Board is currently considering developments and will provide a detailed response for the benefit of Infigen Security Holders. During the month of May 2020, total Renewable Energy Generation sold from the Smithfield OCGT stood at 154GWh.

May 2020 Production (Source: Company Reports)

Suspension of Distribution: The company has decided not to pay a distribution for 2H FY20 as the off-market takeover offers from Iberdrola Renewables Australia Pty Ltd and UAC Energy Holdings Pty Ltd are on the basis of no distribution being paid with respect to 2H FY20.

Key Risks: The company’s key business risk mainly involves uncertainty pertaining to demand & price for Electricity and Large-Scale Generation Certificates (LGCs). Adverse changes in the price for electricity and LGCs arising from decreasing demand, increasing competition, or regulatory changes can affect the business. The company is also exposed to operations & production risk, which is associated with the variation in wind resources causing changes to Infigen’s electricity production level and generation profile and adversely affecting the company’s revenue and market sentiment.

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Current ratio of the company stood at 2.01x in 1H FY20 as compared to the industry median of 0.50x, reflecting decent capabilities of the company to address its-short-term obligations against the peer group. We have valued the stock using the EV/Sales multiple based illustrative relative valuation method. For the purpose, we have taken peers such as AusNet Services Ltd (ASX: AST), Genesis Energy Ltd (ASX: GNE), Meridian Energy Ltd (ASX: MEZ) and arrived at a price correction of low single-digit (in percentage terms). Considering the takeover offer from UAC Energy Holdings Pty Ltdand Iberdrola Renewables Australia Pty Limited, we would like to gaze on how these offers will pan out for security holders. Hence, considering the above-stated factors, we have a watch stance on the stock at the current market price of $0.915 per share, up by 3.39% on 29th June 2020.

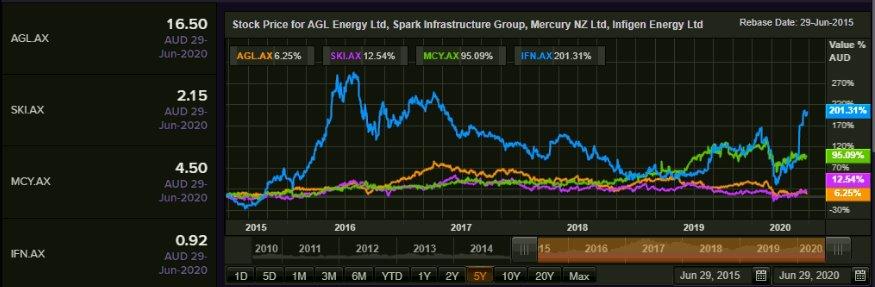

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...