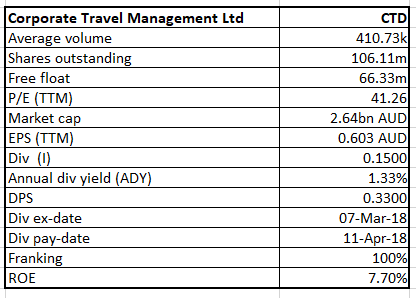

Corporate Travel Management Limited

CTD Details

Strategic Acquisition and ANZ Leadership Changes: Corporate Travel Management Limited (ASX: CTD) is a mid-cap stock with market capitalisation of $2.64 Bn (as at May 01, 2018). The group has announced the acquisition of SCT Travel Group Pty Ltd which trades as Platinum Travel Corporation (PTC) in Queensland (QLD) and New South Wales (NSW). The acquisition will be effective from July 01, 2018. The acquisition cost will be around $5 Mn which represents approximately 5x FY19 EBIT (Earnings before interest and tax), via a mixture of cash and stock, with an additional earn-out component based upon long term growth. This will be funded entirely from short-term cashflow, and there will be no contribution to FY18 results. The rationale behind the acquisition is to increase the market power, by acquiring unique capabilities and resources such as excellent management team, foot hold in international market and high EPS accretive.

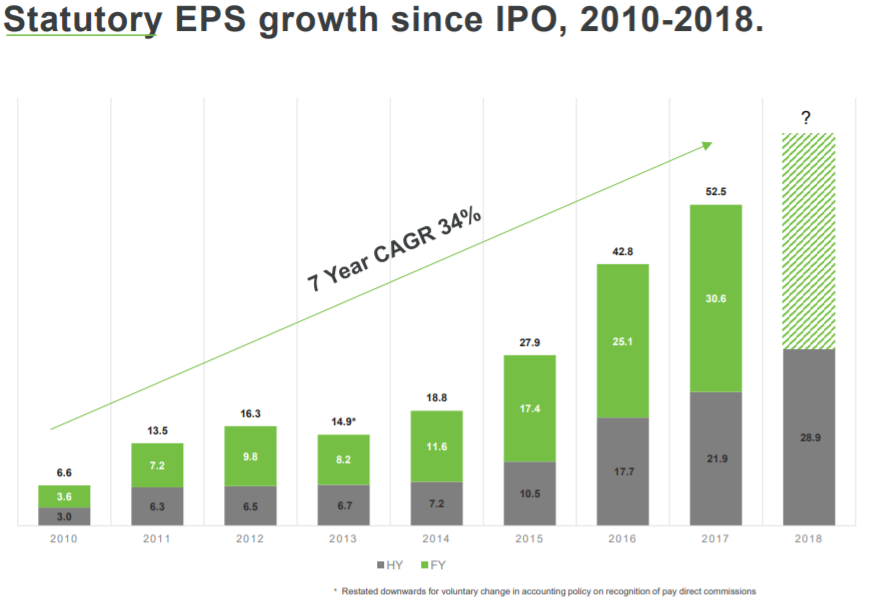

Statutory EPS Growth Since IPO (Source: Company Reports)

This acquisition brings the opportunity to adopt founder of SCT, Mr. Greg McCarthy who has an impeccable reputation in the travel industry and possesses leadership skills which are valued by Corporate Travel. He has over three decades of experience and will be appointed as the Chief Executive Officer of Australia and New Zealand (ANZ) business. Besides this, Anthony Bellas, director of the Company, having an indirect interest in the Company recently disposed of 23,000 shares under off-market transfer, as at 27 March 2018. Meanwhile, the share price rose by 22.74% in the past three months (as at April 30, 2018) and we recommend a “Hold” at the current price of $ 24.770.

.png)

CTD Daily Chart (Source: Thomson Reuters)

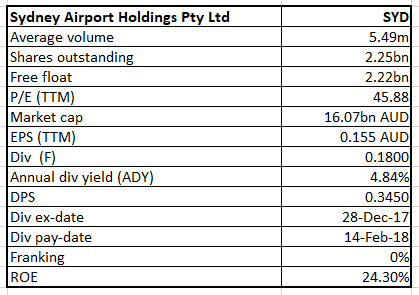

Sydney Airport

SYD Details

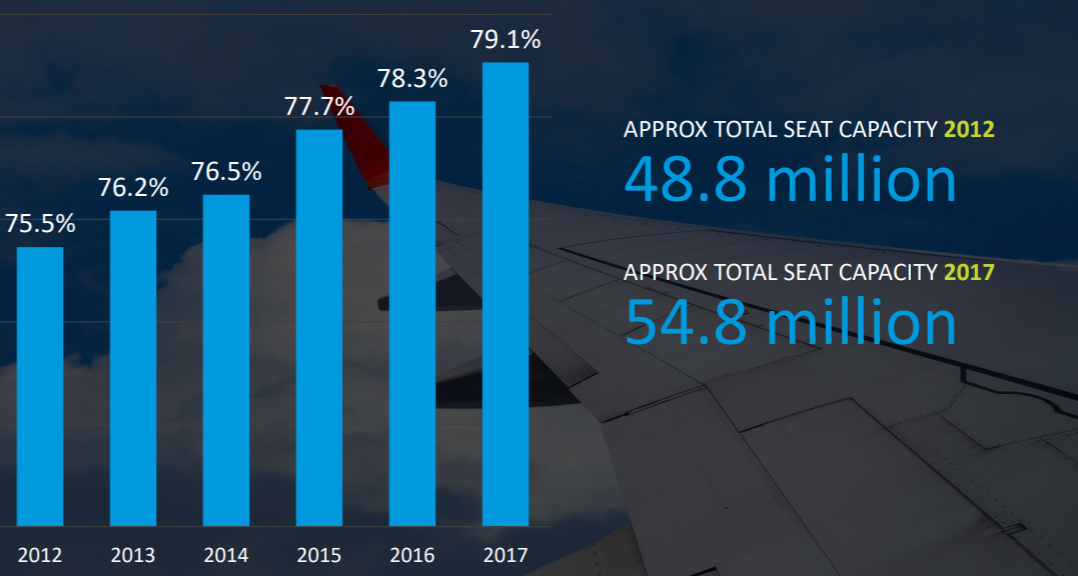

Positive Load factor and Capacity Improvement: Sydney Airport (ASX: SYD) has recently presented its business prospect at the Macquarie Conference, and highlighted about the major trends in travel and aviation business. The group has experienced positive load factor and capacity due to increase in passengers traffic year on year across the globe wherein China, USA, New Zealand, UK, South Korea, Japan, India, Hongkong, Singapore, and Canada contributed to inbound passengers traffic (approximately 17%, 12%, 12%, 8%, 5%, 4%, 4%, 3%, 3%, and 2%, respectively) in 2017. Due to this, the group has increased its total seat capacity to around 54.8 million in 2017 from 48.8 million in 2012. Moreover, the Group contributes significantly in economic activity every year and supports around 338,500 jobs. The Group focuses on toincrease aircraft utilization, improve engineering facilities and lower costs for airlines, thus resulting into overall growth of the company in years to come.

Positive Load factor and Capacity (Source: Company Reports)

Besides the above facts, strict rules and regulations, stiff competitions, and economic slowdown which can hamper traffic volume could be the key concern for the company. Meanwhile, the stockprice was up by 5.32 per cent in the past three months as on April 30, 2018, and is still trading at a slightly high P/E. We give an “Expensive” recommendation on the stock at the current market price of $ 7.120.

.png)

SYD Daily Chart (Source: Thomson Reuters)

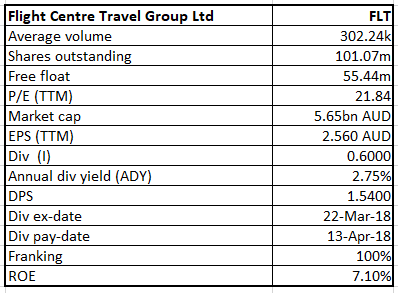

Flight Centre Travel Group Limited

FLT Details

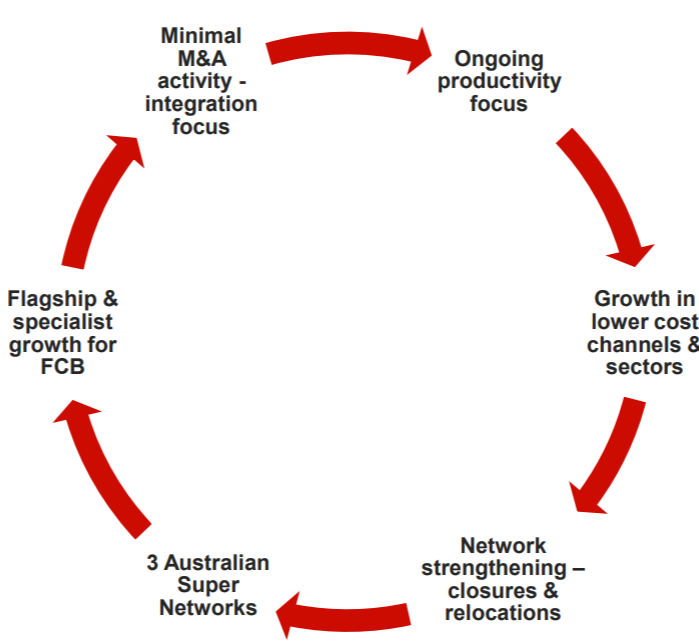

Modest Upgrade to Full Year Target: Flight Centre Travel Group Limited (ASX: FLT) is recognised to be a potential stock for the growth in the corporate travel sector. Recently, the Group has revealed its 2018 fiscal year guidance after the strong first half year growth wherein profit during the period was slightly above the targeted 1H range ($120 Mn-$135 Mn), which compelled FLT to lift its full year guidance of PBT to $360 Mn-$385 Mn as compared to its initial target of $350 Mn-$380 Mn. Moreover, FLT's transformation program is expected to deliver further 2H benefits, along with some additional costs, as the company moves to lower head office overheads, continues to invest in its tech transformation and launches its Australian super networks. While 2H costs will increase, the company remains comfortable with its target of less than $100 million cost growth during FY18. We expect that the group will have brighter outlook on the back of digital commerce growth, globalization, controlling cost & improving efficiency and investment in growth brands & business models.

FY18 Outlook: Continued Network Improvement (Source: Company Reports)

On the other hand, the Group is a cash rich company with cash and cash equivalent of $1,281.6 Mn, net debt to equity of less than 1x and net operating cash flow of $295.3 Mn and free cash flow of $191.2 Mn. The company has been paying regular dividends which reflects the sound financial health of the company. On the other hand, the group has been asked to pay a penalty of $12.5 Mn in relation to the competition law test case, which was initiated by the Australian Competition and Consumer Commission (ACCC) in 2012. But, this penalty will not affect FLT’s market guidance for FY18 relating to underlying profit before tax of between $360 Mn and $385 Mn, and penalty will be included in the Group’s statutory results for the year. Meanwhile, the share price was up by 74.09 per cent in the last one year (as at April 30, 2018). Giving the strategic development and positive start of the year, we expect that the group will continue to perform well. We give a “Hold’ recommendation on the stock at the current market price of $ 55.430.

.png)

FLT Daily Chart (Source: Thomson Reuters)

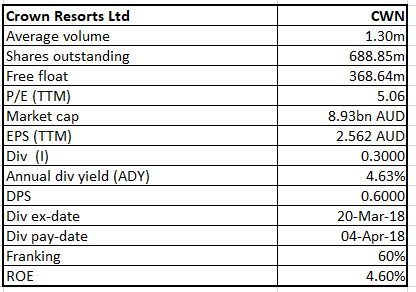

Crown Resorts Limited

CWN details

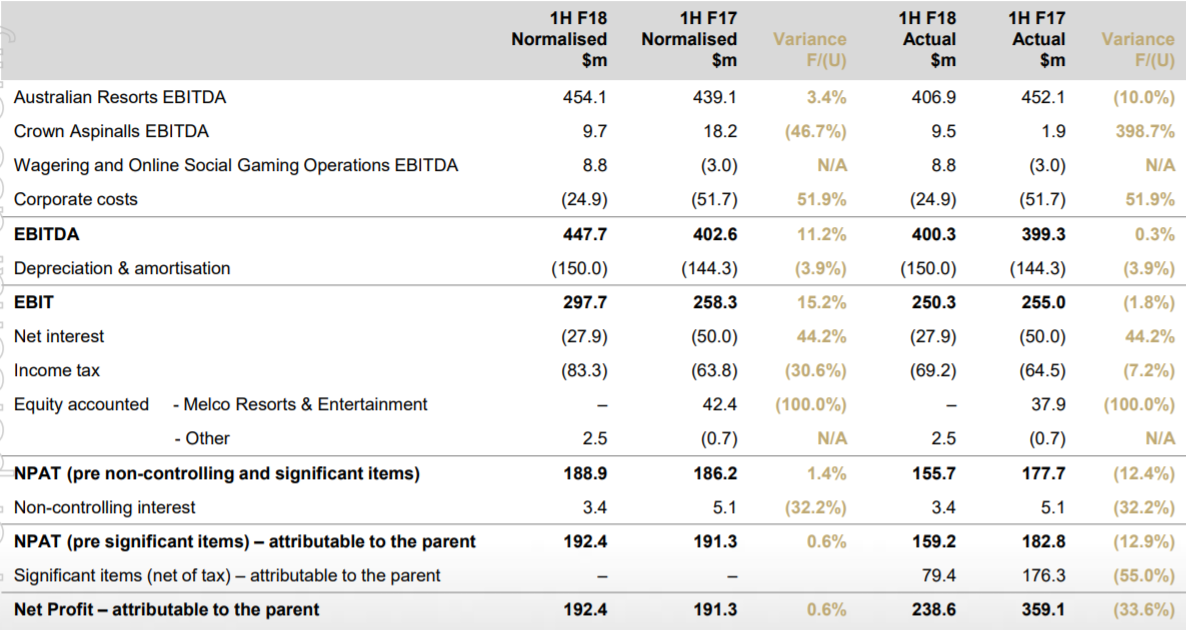

Few headwinds: Crown Resorts Limited (ASX: CWN) updated the market about its buy-back programme wherein cumulative total of 1,314,390 of outstanding Subordinated Notes were bought back and about 4,005,310 of outstanding Notes were issued but not bought back by the Group, as on 27 April 2018. Recently, the company announced about the regulatory matters wherein the group is imposed with a fine of $300,000 by Victoria state gaming regulator for slot machine tampering amid new whistle-blower allegation of company misconduct. On the other hand, the group has recorded growth in revenue at a CAGR of 10.4% during FY13-17 while PAT grew substantially at CAGR of 147.4% during the same period on the back of product mix growth with cost optimization strategy. Return on Equity (RoE) stood at 36.8% during FY17, reflecting sound profitability of the company. We expect that the Group will grow further on the back of strong portfolio of future projects and complementary investment anchored by Crown Sydney including digital business.

1H FY18 Performance Highlights (Source: Company Reports)

Over the period, the Group has gained insight into the marketplace and a better understanding of internal and external factors which could impact the industry. Besides this, the Group has appointed Guy Jalland to the Board as a Director. The stock price was up by 12.99 per cent in the past six months and slightly up by 1.41 per cent in the past five days. We recommend to “Hold” the stock at the current market price of $ 12.980, given the recent developments.

.png)

CWN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...