Stocks’ Details

Woodside Petroleum Limited

Significant growth in operating revenue: Woodside Petroleum Limited (ASX: WPL) is the pioneer of the LNG industry with its operations in Australia. It is the leading natural gas producing company in Australia with world-class capabilities as an integrated upstream supplier of energy.

The company in its recent sustainability report discussed its 2019 priorities including progress transition to a predominantly residential operational workforce in Karratha, enhancing diverse workforce representation and increase technical discipline opportunities.

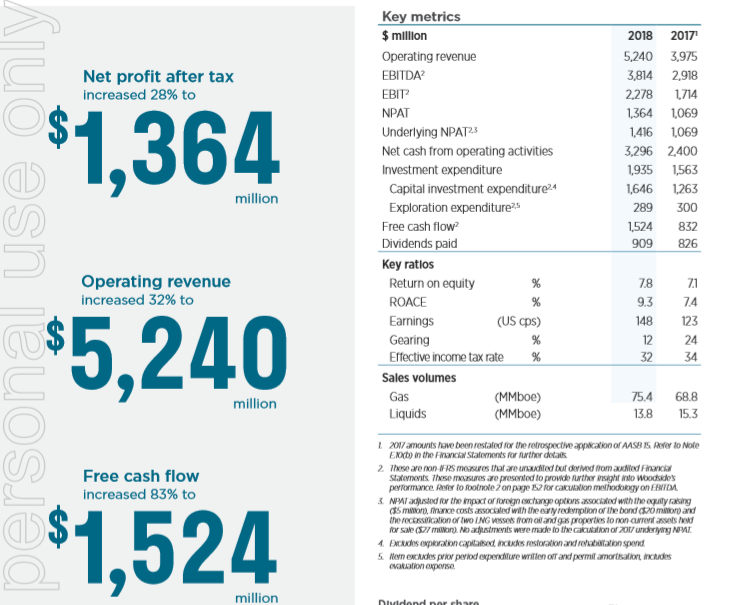

FY18 Financial Summary (Source: Company Reports)

The company achieved 32% increase in the operating revenue to $5.2 billion in FY18 as compared to $3.9 billion in FY17, and a 28% increase in net profit after tax to ~$1.36 billion in FY18. These strong results were driven by increased production due to the start-up of major projects, higher prices and discipline on costs.

What to expect going forward: The investment expenditure guidance for the company in 2019 is $1,600 million to $1,700 million. The company is increasing expenditure on its growth projects including Scarborough, Pluto LNG Train 2, Browse to North West Shelf Project and SNE Field Development Phase 1. Expenditure for the Greater Enfield Project will reduce ahead of expected first oil in mid-2019, and work will continue on the Wheatstone Julimar Phase 2 development.

Considering the robust fundamentals based on a significant increase in free cash flows with improvement in financial performance, we maintain our “Buy” rating on the stock at CMP of $34.840 (up 1.338% on 28 March 2019).

Qantas Airways Limited

Strong earnings quality: Qantas Airways Limited (ASX: QAN) provides services related to passenger and freight air transportation globally and in Australia. The company has made an announcement related to its ongoing on-market buy-back event involving a total consideration of up to $305 million which would be acquired under the buyback. The remaining consideration to be paid for shares under the buy-back is up to $245,181,576.47. Till date, the company has bought back 10,806,093 shares at a consideration of $59,818,423.5. However, the company announced cancellation of buy-back of 93,74,058 shares at a consideration of $52,159,192.8.

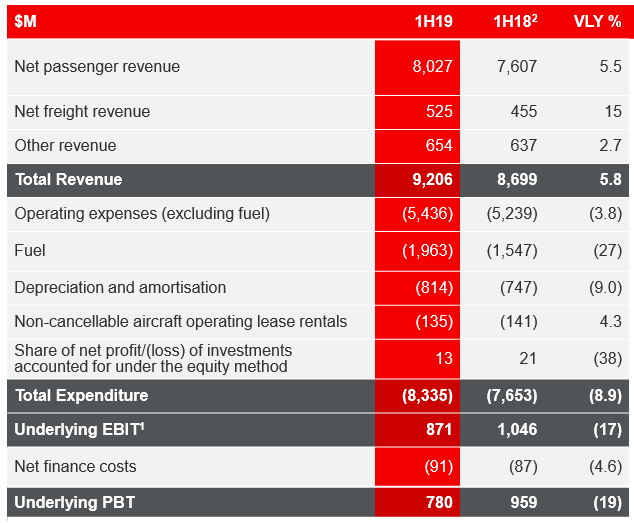

1H FY 2019 Group Revenue (Source: Company Reports)

The domestic group posted record profit, up 1 per cent to $659 million, on the back of higher earnings from both Qantas and Jetstar.The revenue of Qantas International increased by ~7 per cent to $3.7 billion however the EBIT declined by 60% to $90 million mainly because of the rapid rise in fuel costs.

Expected strong second half: The group is in a better position to post a strong second half performance and to completely recover its increased fuel cost by the end of this financial year. Forward bookings are up by 6.8% as at 31 December 2018, which includes the impact of Easter falling in Q4, reducing RASK growth for Q3. The company is flexible to respond to the market conditions.

Considering the robust fundamentals of the company, decent annual dividend yield of around 4.04% and decent outlook, we reiterate our “Buy” recommendation on the stock at the current market price of $5.530 per share (up 1.654% on 28 March 2019).

Commonwealth Bank of Australia

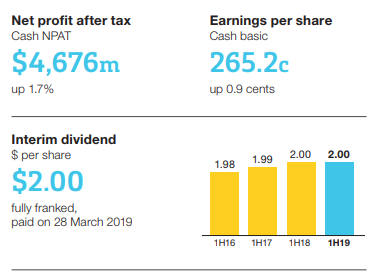

A Look at Letter to Shareholders: Commonwealth Bank of Australia (ASX: CBA) had recently issued a letter to the shareholders in which 2019 half year highlights were given. The bank’s cash NPAT amounted to $4,676 million in the six months ended December 2018 which implies a rise of 1.7% on the same period of the previous year. The bank declared interim dividend amounting to $2.00 per share (fully franked). CBA stated that almost three-quarters of the cash net profit after tax is being returned to the shareholders in the form of dividends.

Key Metrics (Source: Company Reports)

The bank had stated that they rolled out several new initiatives that help in removing customer pain points and that support the customers which are experiencing financial difficulties.

What to Expect From CBA: The bank stated that moving forward, they would be ramping up the work being done to respond to the Royal Commission final report and to deliver on the Remedial Action Plan. The bank had earlier stated that they would be working with the government and regulators and that they are focused on putting the customers first. The bank is targeting lower absolute cost base which would be driven by simpler, more focused and highly digitised businesses.

Stock Recommendation: The stock of CBA has generated a 1.08% return over the span of the previous 6 months, and in the time frame of the previous three months, it posted a 0.73% return. The annual dividend yield of the bank is about 4.20% on a five-year average basis (FY14-18). Also (as at 28 March 2019), the bank has an annual dividend yield of 6.08% which can be considered at decent levels considering the challenging operating environment.

Considering the above factors, along with a decent outlook and strong fundamentals, we maintain our “Buy” rating on the stock at the current market price of $70.910 per share.

Super Retail Group Limited

Strong contribution from Macpac segment: Super Retail Group Limited (ASX: SUL) is a retail industry player with operations in retailing of auto parts and accessories, retailing of boating, and other outdoor equipment; and retailing of sporting equipment and apparel, etc.

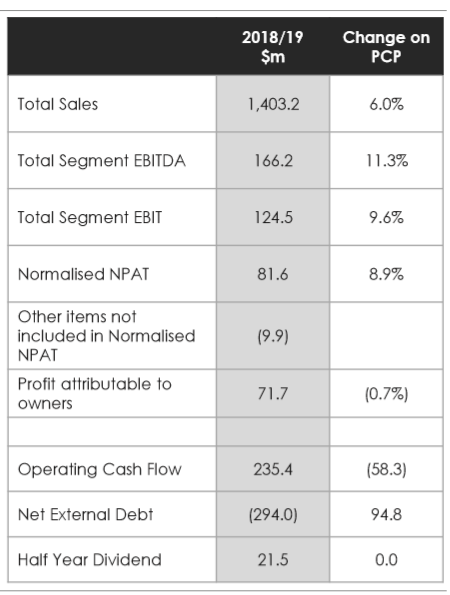

1HFY19 Group Results (Source: Company Reports)

Sales for the period were $1,403.2 million as compared to $1,323.7 million in 1HFY18 reflecting an increase of 6.0 per cent, with core businesses delivering solid sales including strong contribution from Macpac and investment in Omni-retail capabilities.The normalised net profit after tax stood at $81.6 million, an increase of 8.9 per cent over the prior corresponding period.

Focus on growth in market share: The company’s focus for the year ahead is on the execution of its strategy. Precisely, it will focus on growing market share in order to sustain its position as one of Australasia’s leading retailers. Supercheap Auto, BCF and Rebel are the leading businesses in their respective categories, and the company has a plan to grow Macpac into a leadership position. There are opportunities to grow sales and margins in BCF and Rebel through better operational execution.

Meanwhile, the stock generated a YTD return of 9.96%, with a PE multiple of 11.610x. Also, the company had a strong operating cash flow of $235.4 million driven by higher profits.

Considering the above factors and current trading level, we maintain our “Buy” rating of the stock at CMP of $7.600 (up 1.198% on 28 March 2019).

(1).PNG)

Stock Price Comparative Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...