.png)

Stocks’ Details

Telstra Corporation Limited

Key Takeaways from Investor Day Presentation:Telstra Corporation Limited (ASX: TLS) is in the provisioning of telecommunication and information services, which include mobiles, internet and pay television. The market capitalisation of the company stood at A$42.93 Bn as on 27th November 2019. Recently, the company has published a presentation, primarily stating about updates on the key market dynamics in the Enterprise and Consumer & Small Business segments, as well as the transformation of those businesses under T22.

The company stated that T22 is performing multiple jobs, which include delivering cost reductions as well as simplifying its business. It also stated about delivering revenue and profit margin benefits. While remaining focused on delivering operational results from T22, TLS also closely monitors the leading indicators that show the ways theseoutcomes translate into financial benefits for the company.

What to Expect:After excluding expected in-year headwind of nbn, the company is expecting underlying EBITDA to grow up to $500 million. In FY 2020, there are expectations that Capex would be in the range of $2.9 billion- $3.3 billion, which is lower than FY 2019 figure of $4.1 billion. The following image is important in this regard:

.png)

FY20 Guidance (Source: Company Reports)

Stock Recommendation:The company added that, for fixed, a major improvement in economics would require a significant adjustment to the NBN pricing. However, the company has been doing everything it can to improve things that are within its control. Net margin of the company stood at 8.5% in FY19 as compared to the industry median of 6.3%. This reflects that the company possesses better capabilities to convert its top-line into the bottom-line against the broader industry. The stock of TLS has EV to Sales multiple of 2.4x in comparison to the industry average (Telecommunications Services) of 13.1x on TTM basis. In addition, TLS has EV to EBITDA multiple of 7.2x in comparison to the industry median (Telecommunications Services) of 8.5x on TTM basis. Therefore, considering the company’s work on growth opportunities, target to decrease underlying fixed costs by a cumulative $2.5 billion by FY22 and expectations of lower capex in FY 2020 on the YoY basis, we maintain a “Hold” rating on the stock at the current market price of A$3.710 per share, up 2.77% on 27th November 2019.

TPG Telecom Limited

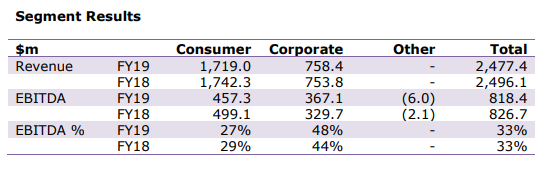

Notice of 2019 AGM: TPG Telecom Limited (ASX: TPM) is engaged in the provisioning of consumer, wholesale and corporate telecommunication services. The company has a market capitalisation of A$6.11 Bn as on 27th November 2019. The company has scheduled to conduct its 2019 Annual General Meeting on 4th December 2019. FY19 reported results of the company have been heavily impacted by the decision of the group to cease the launch of its Australian mobile network in January 2019, which gave rise to an impairment expense amounting to $236.8 Mn and a significant rise in amortisation and interest expense relating to TPM’s Australian spectrum licences. The below picture provides an idea of segment results for the financial year ended 31st July 2019:

Segment Results (Source: Company Reports)

Future Guidance:The company expects FY20 to be the year, where it will experience the substantial financial impact from customer migration to NBN, with combined headwinds from residential DSL and home phone customers moving to NBN anticipated to be approximately $85 Mn. The group forecasts to have less than 15% of its residential broadband customer base remaining on ADSL by the end of FY20.

Stock Recommendation:In FY19, the Group’s net operating cashflows before tax stood strong, surpassing EBITDA at $836.3 Mn. Return on equity of the company stood at 6.1% in FY19 against the industry median of 5.7%, demonstrating decent returns provided to shareholders against the peer group. Debt to equity of TPM stood at 0.61x in FY19 in comparison to the industry median of 0.73x. The stock of TPM is trading at a price to cash flow multiple of 9.1x as compared to the industry average (Telecommunications Services) of 17.7x on TTM basis. TPM has EV to sales multiple of 3.2x against the industry average (Telecommunications Services) of 13.1x on TTM basis. Thus, considering the company’s deleveraged balance sheet and returns to shareholders, we give a “Hold” rating on the stock at the current market price of A$6.850 per share, up 3.945% on 27th November 2019.

Vocus Group Limited

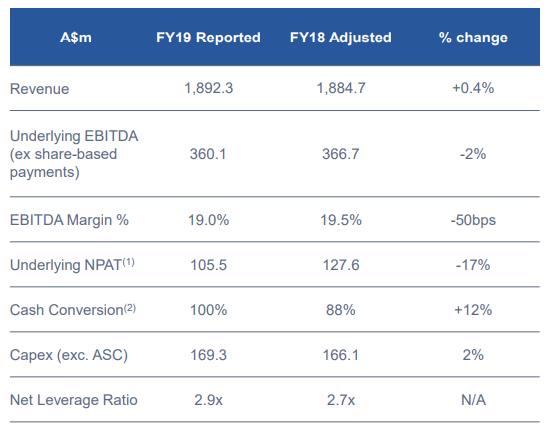

Results of FY19 within Guidance:Vocus Group Limited (ASX: VOC) is a provider of specialist fibre and network solutions, connecting all mainland capitals with Asia. The market capitalisation of the company stood at A$2.06 Bn as on 27th November 2019. The company recently announced that Julie Fahey has made a change to holdings in the company by acquiring 7,510 ordinary shares by paying a consideration of $25,016.57 on 7th November 2019. CEO of the company addressed the shareholders and stated that VOC has delivered its FY19 results, which were in-line with the guidance provided.The revenue of the group was steady at $1.9 billion, and underlying earnings before interest, tax, depreciation and amortisation witnessed a decline of 2%, and the figure stood at $360 million.

Financial Summary (Source: Company Reports)

Future Guidance:For FY20, the company reiterated its guidance for underlying EBITDA in the range of $359 Mn-$379 Mn. The company also anticipates that EBITDA growth in Vocus Networks of $20 Mn-$30 Mn would be offset by a similar decline in the Retail business.

Stock Recommendation:Current ratio of the company stood at 0.78x in FY19, which is in-line with the industry median. The stock of VOC has EV to Sales multiple of 1.6x in comparison to the industry median (Telecommunications Services) of 2.8x on TTM basis. VOC’s stock is trading at a price to cash flow multiple of 7.2x against the industry average (Telecommunications Services) of 17.7x on TTM basis. In the span of the last three months, the stock delivered a return of 4.08% and 8.14% on a YTD basis. Thus, considering the company’s strong position to deliver on its core market opportunity, expectation of second-half performance to be stronger against the first-half, decent valuation parameters, we give a “Buy” recommendation on the stock at the current market price of A$3.200 per share, down 3.614% on 27th November 2019.

amaysim Australia Limited

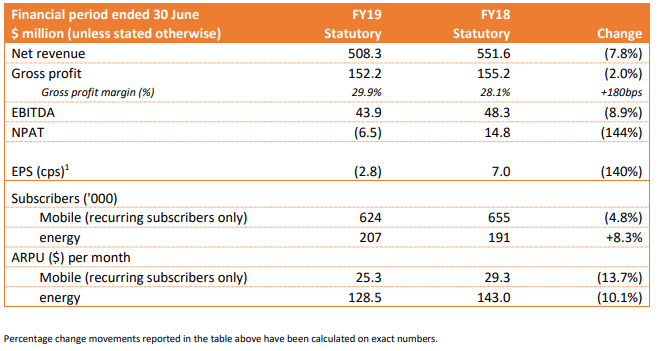

Re-Set Year for the Business:amaysim Australia Limited (ASX: AYS) provides mobile services in Australia and has a market capitalisation of A$109.19 Mn as on 27th November 2019. As per the key personnel of the company, the financial year 2019 has been a re-set year for the business. It was mentioned that the mobile market has continued to be highly competitive. The network operator’s ‘growth-at-any-cost’ mentality had an adverse impact on ARPU throughout the entire market. The below picture provides an overview of the financial summary for the year ended 30th June 2019:

Key Numbers (Source: Company Reports)

Future Prospects:The Board and Management of the company are positive for the medium to long term outlook for the business, despite the challenges in mobile and energy. The company is well placed to take benefit of growth opportunities with funding secured from the capital raise, which is providing the financial flexibility to drive growth.

Stock Recommendation:As at 18th October 2019, recurring mobile subscribers stood at 648k.This reflected the growth of 19k in Q1 FY20 and a further 5k net subscribers in the first three weeks of October. The stock of AYS has EV to Sales multiple of 0.3x against the industry average (Telecommunications Services) of 13.1x on TTM basis. In addition, EV to EBITDA multiple for the stock stands at 3.5x in comparison to the industry average (Telecommunications Services) of 6.8x on TTM basis, indicating an undervalued position at the current juncture. As per the ASX, the stock of AYS is trading towards its 52-week lower levels. Therefore, in light of the company’s focus on its core businesses with necessary resources to execute on its strategy, current trading levels and favorable valuation metrics, we give a “Speculative Buy” recommendation on the stock at the current market price of A$0.360 per share, down 2.703% on 27th November 2019.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...