.png)

Stocks’ Details

Vocus Group Limited

FY19 Results in-line with the Guidance:Vocus Group Limited (ASX: VOC) provides fibre and network solutions, connecting all mainland capitals with Asia. The company has backhaul fibre, connecting most regional centres in Australia. It also operates an extensive and modern network in New Zealand, connecting the country’s capitals and most regional centres. The company recently updated that the voting power of Challenger Limited increased from 7.09% to 8.18%.

Financial Highlights of FY19:During the year ended 30 June 2019, the company reported revenue amounting to $1,892.3 million, up 0.4% on the previous year’s revenue of $1,884.7 million. Underlying EBITDA, excluding share-based payment, stood at $360.1 million, down 2% on the previous year underlying EBITDA of $366.7 million. Vocus Network Services, the core business reported a growth of 5% in recurring revenue. In addition, the company continued to post decent performance from Vocus New Zealand, with revenue and EBITDA increasing at a rate of 4.5% and 2.5%, respectively.

.png)

FY19 Financial Summary (Source: Company Reports)

Outlook: The company issued the revised guidance for FY20 to exclude share-based payments of $9 million from underlying EBITDA. FY20 underlying EBITDA is expected to be in the range of $359 - $379 million, as compared to the earlier guidance of $350 - $370 million. Capital expenditure is expected to be in the range of $200 - $210 million. Vocus Network Services’ EBITDA is expected to report a growth in the range of $20 - $30 million, which will be offset by a similar decline in Retail. Cash conversion for the year is expected to be between 90% - 95%.

Stock Recommendation: The stock of the company has generated YTD returns of 14.01% and is currently trading below the average of its 52-week trading range of $2.810 - $4.900. During FY19, the company reported a decent growth in its core business that contributed to the majority of EBITDA. All the key metrics were in-line with the guidance provided, laying the foundations to deliver growth in the future. With the right leadership & skills in place and re-orientation of the business strategy to capitalise on its exceptional infrastructure assets, the company will now focus on executing its growth plans over the coming 24 months. Considering the above factors and current trading levels, we give a “Hold” recommendation on the stock at the current market price of $3.570, up 2% on 22 October 2019.

amaysim Australia Limited

Capital Raise provides Enhanced Financial Flexibility:amaysim Australia Limited (ASX: AYS) is primarily engaged in the delivery of mobile and retail energy plans in Australia. The company recently updated on a change in KMP (Key Management Personnel) remuneration structure, wherein KMP will forgo cash bonuses for FY20 and FY21, potentially up to 75% of an individual’s annual base salary each year, under the Short-Term Incentive Plan (STIP). In exchange, they will be provided with a base salary increase from $450,000 to $550,000 and a grant of 4,250,000 performance rights under the Long-Term Incentive Plan (LTIP).

As per another announcement, the company notified that the 2019 Annual General Meeting will be held on 24 October 2019.

FY19 Financial Highlights: During the year ended 30 June 2019, the company generated net revenue amounting to $510.9 million, down 7.4% on a comparable basis on the previous year. Underlying EBITDA for the period stood at $47.3 million, down 14.5% on pcp. Gross profit margin for the year remained stable at $153.7 million as compared to $155.2 million in FY18.

.png)

FY19 Financial Metrics (Source: Company Reports)

Guidance: Earnings in FY20 are expected to be materially lower than FY19. Underlying EBITDA for the year is expected to be between $33 million - $39 million, down from $47.3 million in FY19, on a ‘New GAAP’ basis.

Stock Recommendation: The stock of the company generated a negative YTD return of 62.04%. The stock price gained more than 14% on 22 October 2019, following the announcement regarding changes in KMP’s remuneration structure. In FY19, the company met the top end of the guidance while simultaneously maintaining its market share in mobile, despite the unfavourable conditions in the mobile and energy markets. The company has enhanced its financial flexibility and balance sheet strength through a capital raise of $50.6 million in March 2019, that makes it well-positioned to take advantage of growth opportunities. Considering the aforesaid scenario and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.390, up 14.706% on 22 October 2019, owing to the release of KMP remuneration structure.

TPG Telecom Limited

FY19 Actual EBITDA Ahead of Guidance:TPG Telecom Limited (ASX:TPM) is engaged in the provision of consumer, wholesale and corporate telecommunication services.The company recently announced that it will pay a dividend amounting to AUD 0.0200 per ordinary share, on 19 November 2019.

Financial Highlights for FY19: During the financial year ended 31 July 2019, reported revenue amounted to $2,477.4 million, down ~1% in comparison to $2,496.1 million in FY18. Reported EBITDA before impairment amounted to $809.4 million as compared to $826.7 million in FY18. Reported results for the year were impacted by the decision to cease the rollout of the Australian mobile network in January 2019, resulting in an impairment expense of $236.8 million and a material increase in amortisation and interest expense, pertaining to Australian spectrum licenses.

.png)

FY19 Results Summary (Source: Company Reports)

FY20 Guidance:In FY20, the company is expected to witness the greatest financial impact from customer migration to NBN. The company expects a financial impact of around $85 million from the combined headwinds from the movement of residential DSL and home phone customers to NBN. In addition, a further headwind of approximately $25 million is expected due to the annualization of the deterioration of profitability of existing NBN customers experienced in 2H19.

Stock Recommendation: The stock of the company generated returns of -4.56% and 0.45% over a period of 1 month and 3 months, respectively. In FY19, the company’s actual EBITDA on a comparable basis stood above the top end of the guidance range of $823.8 million. The period was also marked by strong net operation cashflows, exceeding EBITDA at $836.3 million. Going forward, the company expects another year of growth for the Corporate Division. Hence, considering the above-stated factors and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $6.720, up 0.299% on 22 October 2019.

Telstra Corporation Limited

FY20 Guidance Revised due to NBN Co’s Corporate Plan 2020:Telstra Corporation Limited (ASX: TLS)provides telecommunications and information services to domestic and international customers.

Result of 2019 AGM: In the Annual General Meeting, the company announced the election of Eelco Blok and Nora Scheinkestel, as Directors. In addition, Craig Dunn was re-elected as a Director of the company. In another resolution, the company approved the grant of 372,187 restricted shares and 558,281 Performance Rights under the Telstra FY19 Executive Variable Remuneration Plan, to the CEO and Managing Director, Andrew Penn.

As per another recent announcement, the company notified that Kim Krogh Anderson has been appointed as Group Executive, Product & Technology. Also, the company paid a dividend amounting to AUD 0.0800 per ordinary share, on 26 September 2019.

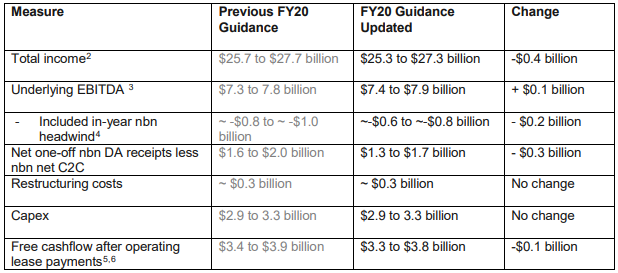

FY20 Guidance Update: The company revised the FY20 guidance, following the release of NBN Co’s Corporate Plan 2020. As per the revised guidance, total income for the year is now expected to be between $25.3 million - $27.3 million, as compared to the previous guidance of $25.7 million - $27.7 million. Guidance for other metrics is provided in the table below:

FY20 Revised Guidance (Source: Company Reports)

Stock Recommendation: The stock of the company generated a YTD return of 32.27% and has a market capitalisation of ~$42.82 billion. In FY19, the company delivered strong progress on the T22 strategy and expects to rollout 5G in 35 cities across Australia in the near future. The company’s gross margin for FY19 stood at 63.8%, which is higher than the industry median of 61.0%. Net margin for the year stood at 8.5%, higher in comparison to the industry median of 7.8%. Currently, the stock is trading close to its 52-week high levels of $3.978 with PE multiple of 19.89x. Based on the above factors, we recommend a “Hold” rating on the stock at the current market price of $3.610, up 0.278% on 22 October 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...