.png)

Stocks’ Details

Hansen Technologies Limited

A Quick Look at Operational Update: Hansen Technologies Limited (ASX: HSN) is engaged in the development, integration, and support of billings systems software for the telecommunication and utilities industries. The market capitalisation of the company stood at $628.27 Mn as on 2nd June 2020. The company recently updated the market with the operational update and stated that its top priority during this COVID-19 pandemic continues to be the health and wellbeing of its staff and customers. The company added that it has accelerated a number of initiatives resulting in the elimination of certain layers of management and the optimisation of its global teams, including the acceleration of the Sigma integration.

During 1H FY20, the company recorded several project wins, which included the first cross-sell by Sigma into its energy customer base, deploying for Simply Energy in Australia Sigma’s CPQ and Catalog products, integrated with its existing Customer Information System. This indicates the quality of HSN’s products and the expertise of its people. The company recorded operating revenue amounting to $144.3 million during 1H FY20, reflecting a rise of 28%. This was fueled by the contribution from Sigma after being acquired in June 2019.

.png)

Key Financials (Source: Company Reports)

What to Expect: For FY20, the company expects operating revenues in the range of $298 million - $300 million and EBITDA in the vicinity of $75 million and $76 million.

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

.png)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company continues to have decent funding to assist its cash flow requirements. Current ratio of the company stood at 1.70x in 1H FY20, reflecting YoY growth of 16.2%. This indicates that the company has improved its liquidity position to meet its short-term obligations. The stock of HSN is inclined towards its 52-week low level of $2.620, offering decent opportunities to accumulate. We have valued the stock using the EV/Sales multiple based illustrative relative valuation method. For the purpose, we have taken peers such as Infomedia Ltd (ASX: IFM), Integrated Research Ltd (ASX: IRI), rhipe Ltd (ASX: RHP), etc., and arrived at a target price with an upside of low double-digit (in percentage terms). Thus, it can be said that the stock of HSN is undervalued at current trading levels. Hence, considering the several contract wins during 1H FY20,contribution from Sigma, improved liquidity position and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $3.100 per share, down by 2.208% on 2nd June 2020.

EML Payments Limited

Revenue and Earnings Diversification: EML Payments Limited (ASX: EML) is an issuer of pre-paid financial cards. The market capitalisation of the company stood at $1.34 Bn as on 2nd June 2020. The company recently stated that it has a long-term strategy to deliver revenue and earnings diversification through organic growth and strategic acquisitions. For the nine months to 31 March 2020, the Gross Debit Volume (GDV) stood at $9.83 Bn, reflecting a rise of 55% over pcp. EML reported revenue amounting to $87.1 million with a rise of 20% over pcp. The company recently completed the acquisition of Prepaid Financial Services (PFS), which would make EML one of the leading global prepaid fintech enablers.

.png)

Financial Summary (Source: Company Reports)

Future Aspects: The company expects that Covid-19 would accelerate the take up of digital payments. EML is in the enviable position to finance business actions which would generate long-term value creation.

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

.png)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company is well-positioned to weather any downturn in business with a strong balance sheet and possesses decent financial strength to make investment in its growth. Net margin of the company stood at 7.3% in 1HFY20 as compared to the industry median of 6.2%, reflecting decent capabilities of the company to convert its topline into the bottom line. We have valued the stock using EV/Sales multiple based illustrative relative valuation method. For the purpose, we have taken peers such as Tyro Payments Ltd (ASX: TYR), Pushpay Holdings Ltd (ASX: PPH), ELMO Software Ltd (ASX: ELO), etc., and arrived at a target price with an upside of low double-digit (in percentage terms). Therefore, considering the long-term strategy to deliver revenue and earnings diversification, acquisition of PFS, improvement in net margin and strong balance sheet, we give a “Hold” recommendation on the stock at the current market price of $3.820 per share, up by 2.688% on 2nd June 2020.

Altium Limited

CAGR of 20% in Revenue Over Four Years: Altium Limited (ASX: ALU) is engaged in the development and sales of computer software for the design of electronic products. The market capitalisation of the company stood at $4.89 Bn as on 2nd June 2020. The company recently announced that Pinnacle Investment Management Group Limited and its subsidiaries have become an initial substantial holder in the company on 18th May 2020 with the voting power of 5.29%. Despite the ongoing COVID-19 market conditions, the company is well-placed operationally and commercially. ALU is working intensely to report a solid Q4 result within the unprecedented COVID-19 environment. The company has launched attractive pricing and extended payment terms to drive volume in challenging market conditions.

The company also accelerated the introduction of its new digital online sales capability, as part of the execution of its man-out-of-the-loop strategy to strengthen its transactional sales capacity. Over the span of four years (2015-2019), the company reported a CAGR of 20% in revenue. The below picture gives an overview of financial summary for 1H FY20:

.png)

Financial Summary 1H FY20 (Source: Company Reports)

Impact of COVID-19: As of now, the company expects some headwinds due to the prolongation of restrictions and continued lockdowns associated with the COVID-19 and their impact on the key economies of the US and Western Europe.

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

.png)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The company is profitable and financially strong with a healthy balance sheet and a current cash balance of over US$77 million. ALU is focused on the cash flow management, and it would leverage its strong balance sheet to support its customers. During the span of one month and three months, the stock of ALU has provided returns of 12.96% and 16.59%, respectively. We have valued the stock using the P/CF multiple based illustrative relative valuation methodand arrived at a target price with an upside of low single-digit (in percentage terms). For the purpose, we have taken peers like TechnologyOne Ltd (ASX: TNE), WiseTech Global Ltd (ASX: WTC), NEXTDC Ltd (ASX: NXT), etc. Thus, considering the CAGR of 20% in revenue, launch of attractive pricing and extended payment terms, strong balance sheet and returns provided in the past months, we give a “Hold” recommendation on the stock at the current market price of $37.230 per share, down by 0.214% on 2nd June 2020.

Superloop Limited

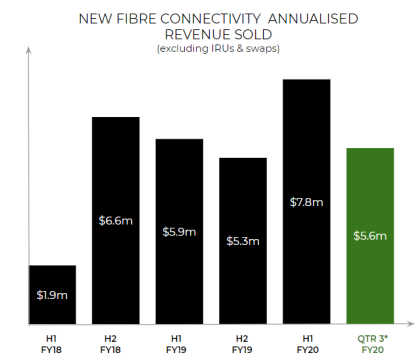

Strong Sales Performance in Q3 FY20: Superloop Limited (ASX: SLC) provides telecommunication infrastructure and managed services. The market capitalisation of the company stood at $402.45 Mn as on 2nd June 2020. During Q3 FY20, the company recorded strong core fibre connectivity sales performance, with sales totalling $5.6 million, which include multiple high capacity services (10G and 100G) contracted on the Indigo cable system and other routes on its recently completed international network. SLC’s cyber security services have also witnessed decent growth, as education providers transition to a distributed education environment due to COVID-19. The strong sales performance during Q3 underpinned revenue growth broadly in line with its expectations for FY20.

Annualised Revenue (Source: Company Reports)

Guidance for FY20: The company anticipates EBITDA in the ambit of $12 million — $15 million, reflecting expected downside risk relating to COVID-19. The company continues to track towards the midpoint of guidance despite challenging market conditions.

Stock Recommendation: Over the last few months, the company has experienced a growth in demand on its Internet / IP network. This was mainly driven by the changing traffic profile and volume as a result of work from home patterns as well as an increase in video conferencing / streaming services. Debt to equity multiple of the company stood at 0.12x in 1H FY20 against the industry median of 1.14x. Current ratio of SLC stood at 1.20x as compared to the industry median of 0.81x. This implies that the company is in a decent position to address its short-term obligations. The stock of SLC is trading at a price to cash flow multiple of 1.5x against the industry median (Telecommunications Services) of 10.1x. SLC is also trading at a price to book multiple of 1.0x versus industry median (Telecommunications Services) of 2.5x. Therefore, in light of the growth in demand on its Internet / IP network, strong core fibre connectivity sales performance, deleveraged balance sheet and decent liquidity position, we maintain a “Hold” rating on the stock at the current market price of $1.095 per share, down by 0.455% on 2nd June 2020.

Comparative Price Chart(Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...