.png)

Stocks’ Details

Appen Limited

Substantial Increase in NPAT: Appen Limited (ASX: APX) provides quality data solutions and services for machine learning and artificial intelligence applications for global technology companies, auto manufacturers and government agencies. The company has recently announced that it will release earnings information for the year ended 31 December 2019 on 25 February 2020. For the first half ended 30 June 2019, revenue of the company went up by 60% to $245.1 million and underlying EBITDA margins improved from 16.8% to 18.9%. In addition to high revenue growth, underlying NPAT witnessed an increase of 67% and stood at $29.6 million. The strong financial performance of the company enabled the Board to declare a partially franked dividend of 4 cents per share.

.png)

Financial Performance (Source: Company Reports)

What to Expect: The company has recently provided an improved EBITDA guidance for FY19 and expects it to be in the range of $96 million to $99 million. This improvement is a result of increase in monthly relevance revenues and margins, driven from existing projects with existing customers. The company has also confirmed its ARR guidance and expects it to be between $30 million to $35 million.

Valuation Methodology: EV/Sales Multiple Approach

.png)

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock gave a return of 9.11% on YTD basis and a return of 2.80% in the last one month. For 1H19, gross margin of the company improved from the prior period and stood at 40.8%. In the same period, Return on Equity was in-line with the industry median and stood at 6.2%. Considering the returns, improvement in gross margin and increased EBITDA guidance, we have valued the stock using one relative valuation menthod, i.e., EV/Sales multiple approach and arrived at a target upside of lower double-digit (in percentage terms). For the said purposes, we have considered WiseTech Global Ltd (ASX: WTC), Altium Ltd (ASX: ALU), Link Administration Holdings Ltd (ASX: LNK) and Iress Ltd (ASX: IRE) as peers. Hence, we recommend a “Hold” rating on the stock at a current market price of $24.33, up by 0.537% on January 15, 2020.

Splitit Payments Ltd

Strong Black Friday Sales: Splitit Payments Ltd (ASX: SPT) provides credit card-based instalment solution to businesses and merchants. As on 15 January 2020, the market capitalization of the company stood at ~$222.75 million. The company has recently announced that 5,368,699 fully paid ordinary shares will be released from mandatory escrow. The company has performed well during the Black Friday and Cyber Monday holiday period with first ever day of underlying merchant sales of more than $1 million. The Average Order Value (AOV) for the same period went up to US$820, representing an increase on the Company’s year-to-date AOV of US$644.

The company has recently released its quarterly update for September quarter, wherein it reported strong growth across all key operational performance metrics. For the quarter ended 30 September 2019, total merchants reached 624, up by 97% on pcp with merchant transaction volume of US$30.5 million, up by 100% from US$15.2 million in Q318.

.png)

Performance Metrics (Source: Company Reports)

Growth Opportunities: The company will continue to implement its growth strategy and will acquire large merchants and will build strong partnerships with eCommerce platforms, payment processors, technology services, point of sale providers, banks and large multinational corporations to scale at a faster rate. SPT also anticipates unique customers and transaction volumes, which will support growth in merchant fees in the upcoming years.

Stock Recommendation: As per ASX, the stock of SPT gave a return of 3.62% in the last one month and is inclined towards its 52-weeks’ low level of $0.305, offering a decent opportunity for accumulation. For 1H19, gross margin of the company stood at 90.4%, higher than the industry median of 74.5%. The company also reported a strong financial balance sheet with Debt/Equity of 0.01x, lower than the industry median of 0.34x. Considering the returns, trading levels, higher gross margin and decent outlook, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.68, down by 4.895% on January 15, 2020.

Xref Limited

CVCheck and Xref form Strategic Alliance: Xref Limited (ASX: XF1) develops human resources technology, which automates the candidate reference process for employers. The company has recently announced that it has issued 10,593,939 new fully paid ordinary shares at a consideration of $0.33 per share. CV Check Limited and Xref Limited recently formed a strategic alliance, which will create a formidable offering to benefit each other’s customers.

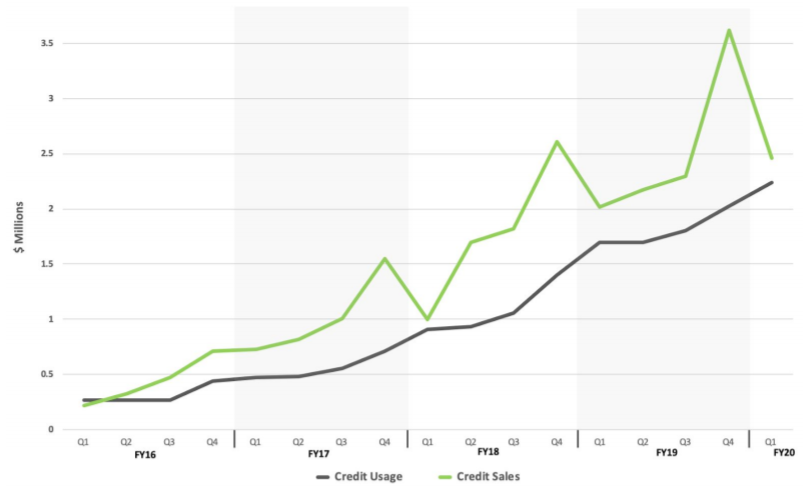

The company achieved record credit usage of $2.24 million with record cash receipts of $3.53 million in Q1FY20. Net cash outflow for the quarter stood at $1.946 million as compared to $1.519 million in Q4 FY19.

Sales & Credit Usage (Source: Company Reports)

Stock Recommendation: As per ASX, the stock of XF1 is trading close to its 52-week low of $0.310 and is offering a good opportunity to accumulate. The company has introduced new products and features in Q1FY20 and is in a great position to leverage opportunities. Over the period of 3 years, from FY16-19, the company witnessed a CAGR of 82.24% in revenue. In the same time span, EBITDA margin also witnessed a substantial improvement. Considering the trading levels, CAGR in revenue and improvement in EBITDA margin, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.325 on January 15, 2020.

Elmo Software Limited

Expansion in R&D Capability: Elmo Software Limited (ASX: ELO) is a leading provider of software-as-a-service (SaaS), cloud-based human resources and payroll solutions. As on 15 January 2020, the market capitalization of the company stood at $481.06 million. The company has recently announced an investment of $1.18 million in Hero Brands Pty Limited in an exchange for 50% equity ownership. This will enable the company with increased Research and Development capability.

In the recently held AGM, the Management stated that the Annualised recurring revenue has increased by 47.8% to $46 million in FY19. The company has increased its customer base to 1,341 and witnessed a CAGR of 51.6% over the period of FY15-19.

.png)

Financial and Operational Highlights (Source: Company Reports)

Growth Opportunities: The company has expanded its market opportunity with the recent entry into payroll and rostering / time & attendance. It is also building a platform which is broad in functionality and simple in usability. The company expects strong momentum in FY20 and expects ARR to lie between $61 million to $63 million and revenue to range between $53 million to $55 million.

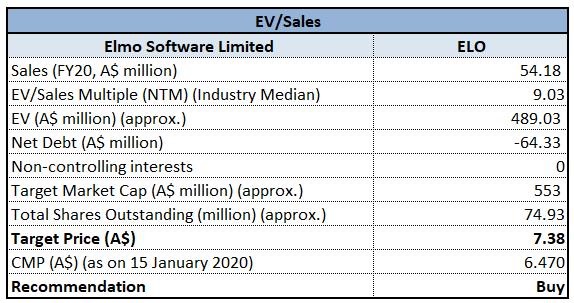

Valuation Methodology: EV/Sales Multiple Approach

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of ELO gave a return of 3.22% in the past one month and a return of 1.74% on YTD basis. Over the period of FY15 to FY19, the company witnessed a CAGR of 41.17% in gross profit. During FY19, gross margin of the company stood at 86.5%, higher than the industry median of 83.7%. This indicates that the company is managing its costs well and is capable to convert its revenue into profit. Considering the returns, CAGR in gross profit and modest outlook, we have valued the stock using a relative valuation method, i.e., EV to Sales Multiple approach and arrived at a target upside of lower double-digit (in percentage terms). For the said purposes, we have considered Xero Ltd (ASX: XF1), Integrated Research Ltd (ASX: IRI), Livetiles Ltd (ASX: LVT), Volpara Health Technologies Ltd (ASX: VHT) as peers. Hence, we recommend a “Buy” rating on the stock at the current market price of $6.47, up by 0.779% on January 15, 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...