.png)

Stocks’ Details

WiseTech Global Limited

WiseTech Rejects Allegations Imposed by J Capital:WiseTech Global Limited (ASX: WTC) is engaged in providing software to the logistics services industry globally. The company recently updated that its shares will be on a trading halt on account of a pending announcement, till 23 October 2019 or upon release of the said announcement.

Response to Misinformation: As per a recent announcement, the company denied the allegations of financial impropriety and irregularity in the report, issued by J Capital Research Limited. The company rejected the claims in the reports and stated that the report was published without prior inquiry.

The report suggested that the information on organic growth and acquisition revenues in FY19 was unclear. In addition, JCAP also believes that the company’s profit is overstatedon account of exaggeration due to ‘the payment for intangible assets (capitalised costs),’ representing that capitalising the costs of software asset development is an inflation of assets. Other claims in the report consisted of overstatement of European/EMEA revenues, scepticism in relation to growth rates, audit partner movement, etc.

FY19 Financial Highlights:During the year ended 30 June 2019, the company generated revenue amounting to $348.3 million, up 57% on prior corresponding period revenue of $221.6 million. Net profit for the period stood at $54.1 million, up 33% on pcp profit of $40.8 million. Earnings per share increased by 27% to 17.7 cents.

‘.png)

FY19 Financial Summary (Source: Company Reports)

Stock Recommendation: The stock of the company generated returns of 36.99% over the last 6 months. In FY19, the company reported strong growth with the simultaneous expansion of the global platform. EBITDA during the year increased by 39% on prior corresponding period. In addition, the company reported a growth of 76% in free cash flow. Recently, the company has come under the lens due to the report released by J Capital Research, containing allegations on the company’s financial performance. Therefore, the company has requested ASX for a trading halt to keep the shareholders from relying on any misleading information. As a result of the above announcement, the stock made a low of $26.060 and managed to close at $26.300 as on 21 October 2019. Given the aforesaid factors, we have a watch stance on the stock at the current market price of $26.300, down 12.333% on 21 October 2019 and suggest investors to wait till further clarification.

EML Payments Limited

Period of Record Underlying EBITDA:EML Payments Limited (ASX: EML) is engaged in the provision of prepaid payment services in Australia, Europe, and North America. The company recently updated that the shareholding of Challenger Limited reduced to 7.73%, from 8.73% earlier. As per another announcement, the company updated that the 2019 Annual General Meeting will be held on 13 November 2019.

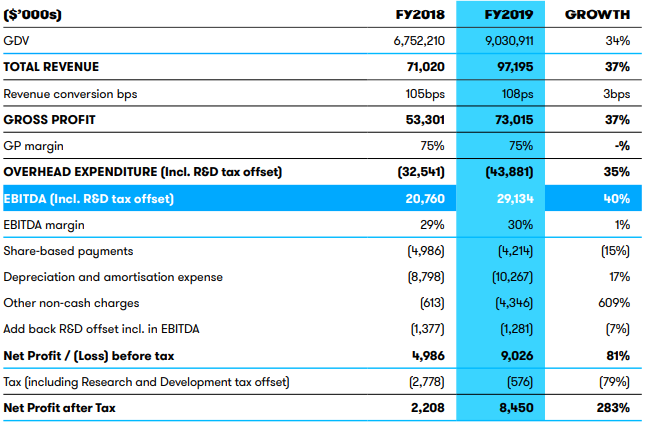

Key Highlights of FY19 Results: During the year ended 30 June 2019, group revenue amounted to $97.2 million, up 37% on prior corresponding year. Group EBITDA for the year stood at $29.1 million, up 40% on the previous year. Gross debit volume for the year stood at $9.03 billion, up 34% on prior corresponding year.

P&L Statement (Source: Company Reports)

During the year, the company successfully acquired and integrated PerfectCard DAC, transitioning to self-issuance in Europe, utilising Irish e-money license.The company also acquired Flex-e-Card group, marking global leadership in the shopping mall segment. The period also saw the launch of Pointsbet and bet365, providing debut in the North American sports betting market.

Stock Recommendation: The stock of the company generated returns of 148.28% over a period of 6 months and is currently trading towards the upper band of its 52-week trading range of $1.210 - $4.670. FY19 was a period of record growth in Gross Debit Volume, driven by Gift & Incentive and Virtual Account Numbers segments. During the year, the company made its debut in the North American sports betting market, which is expected to be a 5 to 10 years growth driver for the business. During the year, both revenue and EBITDA exceeded the guidance range. Moreover, the company has a track record of EBITDA growth with 5-year (FY15 – FY19) EBITDA CAGR of 82%. Considering the above factors and price movement in the last 6 months, we give a “Hold” recommendation on the stock at the current market price of $4.200, down 2.778% on 21 October 2019.

Appen Limited

Strong Growth in Core Business:Appen Limited (ASX: APX) is engaged in the provision of quality data solutions and services for machine learning and artificial intelligence applications for global technology companies, auto manufacturers, and government agencies. Recently, the company issued 7,033 fully paid ordinary shares on account of vesting of performance rights.

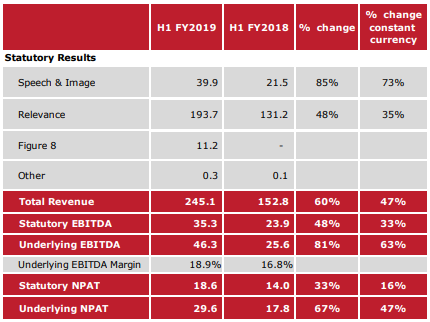

Financial Summary of H1FY19: During the first half ended 30 June 2019, the company generated revenue amounting to $245.1 million, up 60% on the previous year. Underlying EBITDA for the period stood at $46.3 million, up 81% on the previous year. Underlying NPAT amounted to $29.6 million, up 67% on pcp. Speech & Image revenue stood at $39.9 million, up 85% on prior corresponding period in last year. Relevance revenue stood at $193.7 million, up 48% on pcp. The Board declared an interim dividend of 4.0 cents per share.

1HFY19 Financial Highlights (Source: Company Reports)

Outlook: The company is looking forward to strengthening its position in the market through investments in sales & marketing, technology, government markets, and China. Underlying EBITDA for the year ending 31 December 2019 is trending to the upper end of the guidance range of $85 million - $90 million.

Stock Recommendation: The stock of the company generated a negative return of 23.27% over 3 months. H1FY19 proved to be a period of strong cash conversion with underlying EBITDA cash conversion reported at 84%. High growth in Speech and Image revenue came on the back of the expansion of existing projects and new work. The acquisition of Figure Eight helped the company in accelerating its technology roadmap, diversifying revenue and expanding markets for the business. Moreover, the company also achieved efficiency and scale benefits from the integration of Leapforce into the business. Considering the above factors and outlook issued by the company, we give a “Buy” recommendation on the stock at the current market price of $22.000, down 4.265% on 21 October 2019.

LiveTiles Limited

Healthy Outlook for FY20 and Beyond:LiveTiles Limited (ASX: LVT) offers intelligent workplace software for the commercial, government, and education markets. The company recently updated that it has raised an amount of $5.0 million under a Share Purchase Plan. The SPP will include allotment of 14,285,422 shares at an issue price of $0.35 per share.

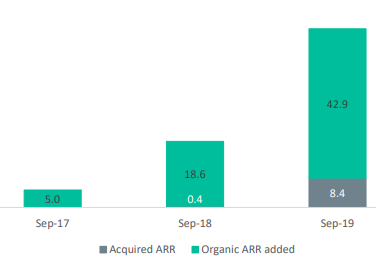

Q1FY20 Highlights: During the quarter ended 30 September 2019, the company witnessed a strong performance in the Asia Pacific region, offset by seasonal buying patterns in the U.S. and European markets. The company reported strong growth from Wizdom, the recently acquired intranet software for the enterprise market, with an increase in the pipeline of deals for FY20. As at 30 September 2019, Annual Recurring Revenue increased to $42.9 million, representing a year-on-year growth of 131%.

ARR Growth (Source: Company Reports)

Outlook: FY20 is expected to be another year of strong customer and revenue growth on the back of continued investments into products, partners & sales and marketing channels. It is targeting to achieve an ARR of at least $100 million by 30 June 2021, implying a compound annual growth rate of 62%.

Stock Recommendation: The stock of the company generated negative returns of 21.05% and 41.18% over 1 month and 3 months, respectively. The company has reported good progress in sales and marketing activity, early in Q2, with a strengthening pipeline and more engaged partner channel. In addition, integration of global sales and marketing teams across Wizdom and LiveTiles witnessed a strong response within the enterprise market in Q1. The company believes that the above efforts will help deliver targeted growth in FY20 along with the long-term growth targets. Hence, considering aforesaid facts and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.290, down 3.333% on 21 October 2019.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...