.png)

Stocks’ Details

Telstra Corporation Limited

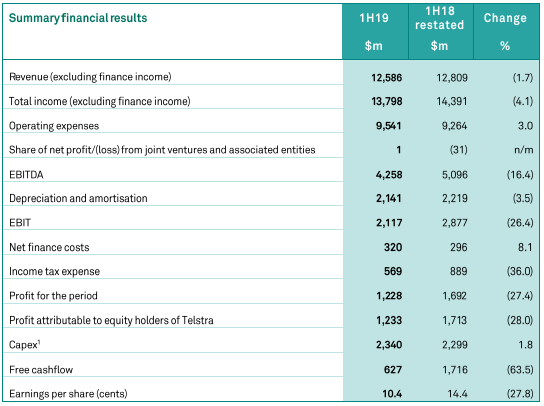

Good Progress on T22 Strategy: Telstra Corporation Limited (ASX: TLS) is into the provisioning of telecommunication and information services, which include mobiles, internet and pay television. The market capitalisation of the company stood at ~A$46.74 Bn as on 14th Aug 2019. Recently, the company with the help of a release announced that it would be conducting a virtual retail shareholder meeting on 3rd September 2019. As per the release dated 29th May 2019, the company announced that it anticipates to make a non-cash impairment and write down of the value of its legacy IT assets by approximately $500 Mn, as a result of good progress on its T22 strategy. With respect to the strategic investment in digitisation, which was announced in 2016, the company has made good progress in standing up its new IT platforms, which are allowing TLS to retire some of its legacy platforms. The following picture provides an idea of financial results for 1H FY19:

Financial Results (Source: Company Reports)

What to Expect: The company has increased its guidance for restructuring costs by around $200 Mn for FY19 on the back of bringing forward a consultation on proposed job reductions. The company further stated that it had started a consultation with employees and representative unions on proposed job reductions, which was previously anticipated to be announced in the 1H FY20. This would result in the relevant restructuring cost being brought forward from FY20 to FY19. The company expects total income in the range of $26.2 Bn - $28.1 Bn and EBITDA (excluding restructuring costs) of between $8.7 Bn to $9.4 Bn for FY19.

Stock Recommendation: The company is expecting to release its full-year results for FY19 on 15th August 2019. The net margin of the company stood at 9.8% in 1H FY19 , which is higher than the industry median of 8.9%. This implies that TLS is effectively converting its top-line into the bottom-line. When it comes to shareholders return, the company delivered a return on equity of 8.5% in 1H FY19 against the industry median of 6.6%, which represents that Telstra Corporation Limited is providing feasible return to shareholders in comparison to the broader industry. Hence, considering the above-stated facts, we give a “Hold” recommendation on the stock at the current market price of A$3.940 per share (up 0.254% on 14th Aug 2019), ahead of its full-year results which are to be released on 15 August 2019.

Baby Bunting Group Limited

Quarterly Rebalance of the S&P/ASX Indices: Baby Bunting Group Limited (ASX: BBN) is leading specialty retailer of baby goods, which is having a market capitalisation of A$278.17 million on of 14th Aug 2019. Recently, the company via a release announced that Mitsubishi UFJ Financial Group, Inc. has become an initial substantial holder in the company with the voting power of 7.07% on 2nd August 2019.

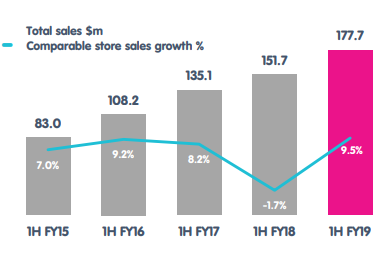

The company would be releasing its results for the financial year 2019 on 16th Aug 2019. As per the release dated 8th March 2019, S&P Dow Jones Indices announced changes in the S&P/ASX indices, wherein Baby Bunting Group Limited has been added to S&P/ASX 300 Index which became effective at the open on 18th March 2019.The company reported total sales amounting to $177.7 Mn, reflecting YoY growth of 17.2%, which have been primarily resulted by strong comparable store sales as well as new and annualising stores.

Total Sales (Source: Company Reports)

Future Prospects: The company is expecting EBITDA for FY19 to be between $25.0 Mn to $27.0 Mn, representing growth in the range of around 34% to 45%. The guidance assumes comparable store sales growth of mid to high single digits for the year and full year gross margin of around 35% for FY19. The guidance also assumes the opening of six new stores in FY19.

Stock Recommendation: The company is capitalising on market share opportunities from competitor closures and securing prime sites for its store network.It is driving private label and exclusive product expansion program. The current ratio of the company stood at 1.73x in 1H FY19 in comparison to the industry median of 1.18x. This implies that the company is well-positioned to address its short-term obligations as compared to the broader industry. Currently, the stock is trading slightly below the average of 52 weeks high and 52 weeks low price of $2.63 and $1.95, respectively. Hence, considering the above-stated facts and current trading levels, we maintain our “Hold” rating on the stock at the current market price of A$2.280 per share (up 3.636% on 14th Aug 2019).

Domain Holdings Australia Limited

Unmarketable Parcel Sale Facility: Domain Holdings Australia Limited (ASX: DHG) is into the real estate media and technology services business which is focused on the Australian property market. The market capitalisation of the company stood at ~A$1.7 Bn as on 14th Aug 2019. Recently, the company, via a release dated 9th August 2019 advised the market that it is establishing an opt-out share sale facility for the shareholders who hold less than $500 worth of fully paid ordinary DHG shares. The company further stated that an Unmarketable Parcel is 179 shares or less based on the closing price of DHG’s shares on ASX, which was $2.78 on 6th August 2019. The company will be conducting its Annual General Meeting on 11th November 2019, and it will release its full-year results on 16th August 2019.

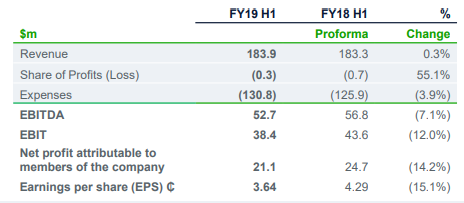

In another update, the company stated that it has wrapped up the sale of its 50% interest in utilities comparison and connection service Compare & Connect to its JV partner TW Australia Holdings 2 Pty Ltd. The following picture provides an idea of group’s performance:

Group Trading Performance (Source: Company Reports)

Future Aspects: The company stated that the first six weeks of 2H FY19 witnessed continued growth in yield and lower listing volumes in a seasonally low listings period. The company is anticipating underlying costs to be slightly low against proforma FY18.

Stock Recommendation: The company delivered a negative return on equity of 12.7% in 1H FY19. It posted asset to equity ratio of 1.32x in 1H FY19 as compared to 1.25x in 1H FY18. As per ASX, the stock of Domain Holdings Australia Limited is trading closer to 52-week higher levels of $3.640.Hence, considering the aforesaid facts and current trading levels, we advise the investors to avoid the stock at the current market price of $3.00 per share (up 3.093% on 14th August 2019), and wait for better entry levels.

Jumbo Interactive Limited

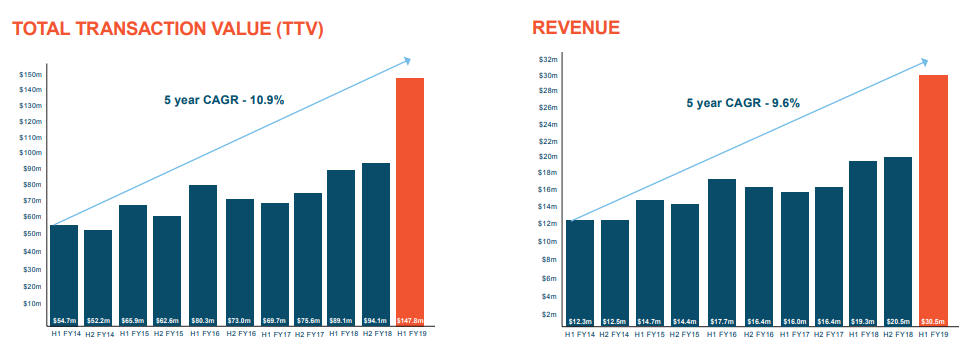

Third Party Share Options Lapse: Jumbo Interactive Limited (ASX: JIN) advised that following certain vesting conditions not being satisfied, a total of 50,000 options expiring February 2, 2022 exercisable at $2.25 lapsed on June 30, 2019 unexercised. The company has also made an announcement about the fully franked special dividend amounting to 8 cents per ordinary share, which have been declared as part of its ongoing capital management strategy. It would be having around $11 million in retained earnings and $10 million in franking credits following payment of the special dividend for the future capital management considerations. The following picture provides an idea of the company’s total transaction value and revenue:

TTV and Revenue (Source: Company Reports)

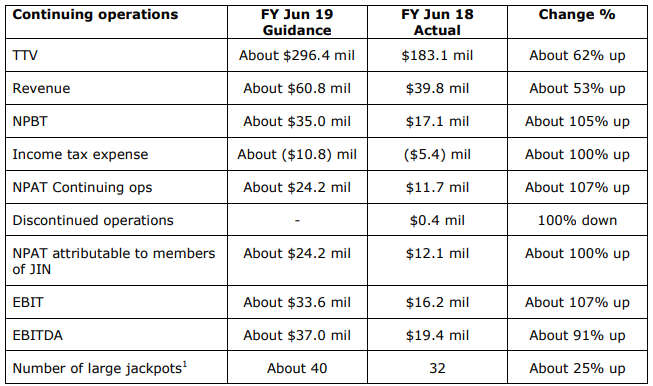

What To Expect From JIN: The company is expected to post TTV amounting to around $296.4 million in FY 2019, which reflects a YoY increase of about 62%. Also, in FY 2019, its revenue has been anticipated at about $60.8 million, implying an increase of around 53% on a YoY basis. The following table gives a broader idea of its guidance for FY 2019:

FY 2019 Outlook (Source: Company Reports)

Stock Recommendation: In the results presentation for 1H FY 2019, the company added that its strong cash generative nature of the operations supports the dividend policy and, we expect, that this might attract the attention of the market players. As per ASX, at the current market price of A$20.710 per share, the annual dividend yield stood at 1.31%, implying decent income for the shareholders. Currently, the stock of JIN is trading closer to its 52-week high price of $21.35 and, thus, it can be said that the price might witness some correction moving forward. Hence, considering the aforesaid facts and current trading levels, we have a wait and watch stance on the stock at the current market price of $20.710 per share (up 4.49% on 14th August 2019) and wait for better entry levels.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...