Qantas Airways Ltd (ASX: QAN)

.png)

QAN Details

Strong Demand across key markets: Qantas released a trading update for the third quarter of FY18 and confirmed it is on track for a record Underlying Profit Before Tax full-year result. The third quarter follows the Group’s record half-year result in February and has been underpinned by positive market conditions, capacity discipline and ongoing transformation. Overall, total revenue for the three months period ending 31 March 2018 was up 7.5 per cent to $4.25 billion compared with the same period last year, and Group Unit Revenue (RASK) increased by 6.0 per cent. Group Domestic Unit Revenue increased by 8.0 per cent compared to the prior corresponding period which reflects strong demand across key markets, including continued recovery of the resources sector and gains within the small-to-medium enterprise segment.Group International Unit Revenue rose by 5.2 per cent. This performance was driven by underlying demand growth and higher load factors, as well as the benefits of ongoing network adjustments to better match demand. Qantas Group International capacity grew by 2.3 per cent while total market capacity grew by 5.0 per cent.

.png)

Capital Allocation (Source: Company Reports)

The Qantas Group affirmed its existing outlook for capacity, fuel costs, capital expenditure and transformation benefits in the second half of FY18. Based on these expectations, Qantas anticipates a Full Year Underlying Profit before tax of between $1.55 billion and $1.60 billion. As of the end of April 2018, the Group has hedged approximately 70 per cent of its expected fuel costs for FY19 and retains significant participation to falls in oil price. The group is lifting the fleet of its Dreamliner while setting to retire the last six Boeing 747s by 2020. Meanwhile, the share buyback of up to $378 million announced in February 2018 as of 30 April 2018 was 51 per cent complete, with 31,510,682 shares acquired. This takes the total number of shares on issue after cancellation to 1,712,598,089. Once this latest buyback is finished, Qantas will have bought back an estimated 24 per cent of its stocks since October 2015, returning significant value to shareholders. The stock prices were up by 8.4 per cent in the last three months followed by a marginal drop of 0.85 per cent in the last five days. The stock rocketed up by 8.1 per cent as on 2 May 2018 after releasing the trading update. Therefore, we give a “Buy” recommendation at the current market price of $6.27.

.png)

QAN Daily Chart (Source: Thomson Reuters)

Propel Funeral Partners Ltd (ASX: PFP)

.png)

PFP Details

Exploring potential acquisitions: Propel is listed on the Australian Stock Exchange and is the second largest provider of death care services in Australia and New Zealand. Propel currently operates from 103 locations, including 23 crematoria and 7 cemeteries. Propel Funeral Partners announced that one of its subsidiaries, FV (ACT) Pty Ltd (Bidder), is now the registered holder of 96.8% of the shares in Norwood Park Limited (Norwood Park). The Bidder has commenced the process of compulsorily acquiring the remaining shares in the capital of Norwood Park pursuant to the relevant provisions of the Corporations Act 2001 (Cth). It is expected that Norwood Park will become a wholly owned subsidiary of the Bidder during Q4 FY18. Financial performance of Propel exceeded expectations during the six months ended 31 December 2017 (1H FY18). As on 31 December 2017, Propel had a strong balance sheet, with net cash of $52.0 million and no senior debt. Propel intends to explore raising a senior debt facility during 2018.

.png)

Death volume Trend (Source: Company Reports)

An increase of 84 per cent in revenue ($38.9 million) and of 90 per cent in pro forma operating NPAT ($6.3 million) was reported as compared to the same period in the last year. Taking into consideration the 1H FY18 financial performance and the expected impacts of the Brindley Group and Norwood Park transactions, Propel has increased its full year pro forma forecast Operating EBITDA for FY18 to $21.1 million, which is an increase of 15% above the pro forma forecast Operating EBITDA in the Prospectus of $18.4 million. No interim dividend has been declared in H1 FY18, however, the board intends to declare a final dividend around the time of the release of the FY18 financial statements. The share price was down by 7.8 per cent since the start of the year, followed by a rise of 2.3 per cent in the last five days. The stock tumbled by about 1 as on 2 May 2018. So, we give a “Speculative Buy” recommendation at the current market price of $3.14 by looking at the growth of the funeral industry and increasing volume of deaths in Australia.

PFP Daily Chart (Source: Thomson Reuters)

REA Group Ltd (ASX: REA)

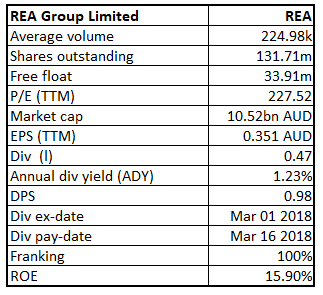

REA Details

In the process to acquire Hometrack Australia: REA Group earlier acquired realestate.com.au Pty for a consideration of $104.5 million and it recently announced that realestate.com.au Pty Ltd has entered into an agreement to acquire 100% of Hometrack Australia Pty Ltd (“Hometrack Australia”) whule the acquisition is subject to ACCC approval. Hometrack Australia is a residential property data company and subsidiary of Hometrack Data Systems, which is owned by UK listed ZPG Plc (LSE: ZPG). Its suite of products includes property data analytics and insights, customised data platforms and an Automated Valuation Model (AVM). The purchase consideration of $130 million will be funded from existing cash reserves and debt of $70 million.

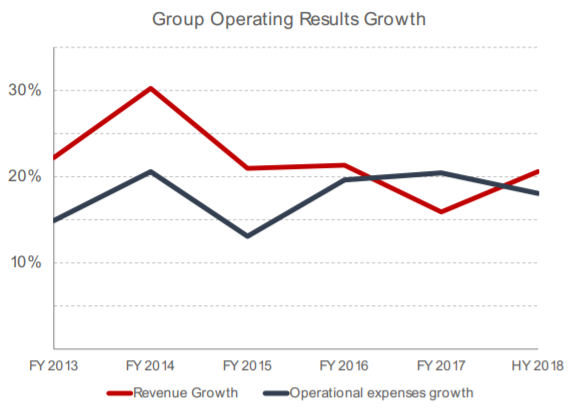

Group Operating Results Growth (Source: Company Reports)

Hometrack Australia is forecast to deliver revenue between $13 million to $15 million and EBITDA between $6 million to $7 million for their financial year ended 30 September 2018. There would also be cost synergies realised in the REA business once the Hometrack business is fully integrated into REA’s platforms. It’s an exciting move for its business and a natural extension for realestate.com.au. The acquisition will allow it to deliver more property data and insights to its customers and consumers. REA is a natural fit for Hometrack in Australia. The Hometrack Australia management team will continue under the leadership of Brendan Darcy and it will maintain its current structure and brand. REA’s share price was up by 8.8 per cent in the last six months and after this announcement of the acquisition the share price jumped up by 2.1 per cent on 2 May 2018. We recommend to “Hold” the stock at the current market price of $81.52.

.png)

REA Daily Chart (Source: Thomson Reuters)

Ramsay Health Care Ltd (ASX: RHC)

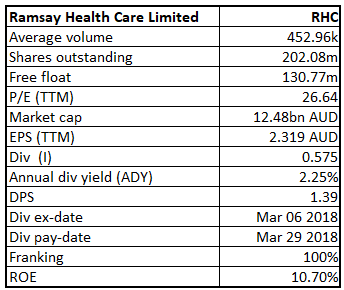

RHC Details

Joint venture agreement with Ascension: Ramsay Health Care Ltd, an Australian operator of hospitals that operates approximately 235 hospitals and day surgery facilities across Australia, the United Kingdom, France, Indonesia, Malaysia and Italy, witnessed a stock price rise of about 1.1% on 2 May 2018 after a fall on 1 May 2018, as the market became sceptical of CEO Mr Craig McNally selling out 75,000 shares to meet some personal tax obligations, and other directors including Roderick Hamilton McGeo disposing about 4,500 ordinary shares, held through McGeoch Holdings Pty Ltd. On the other hand, Ramsay Health Care has moved up on ASX on 2 May 2018, as it inked a joint venture agreement with Ascension, the largest private, tax-exempt, non-governmental health organisation in the United States to develop a new global supply chain to help combine the purchasing power of Ascension with Australian-based Ramsay Health Care. This move is expected to result in initial savings anticipated to be a touch EPS positive to Ramsay in the short term. Meanwhile, Ramsay’s robust balance sheet and strong cash flow generation has continued to provide it with the flexibility to fund the rising demand for brownfield capacity expansion, future acquisitions and ongoing working capital needs. In the UK, the Group is expecting that a positive tariff adjustment taking effect from 1 April 2018 will help the normal volume growth return in the short to medium term. Given the fundamentals, RHC has reaffirmed its Core EPS growth of 8% to 10% for FY18. We maintain a “Buy” on the stock at the current price of $ 62.440.

.png)

RHC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...