Kalkine has a fully transformed New Avatar.

Transurban Group

Constant ADT growth across various links:Transurban Group (ASX: TCL) has announced via a latest release stated that WestConnex (WCX) has successfully reached financial close in relation to a $600 million non-recourse senior bank debt construction facility (Facility) for the M4-M5 Link. The Facility has a tenor of 7 years. It is to be noted that the company has 25.50% stake in the WCX. This facility shall be drawn in order to meet the development costs of the M4-M5 Link. Moreover, the interest rate exposure has been fully hedged for the term of the facility by the company.

Also, the shareholders shall be distributed a sum of 29 cps for the period of six months ending 31st December 2018. This dividend shall be made up of 28 cents from the Transurban holdings trust and controlled entities and 1 percent from the Transurban holdings trust. The record date for the same shall be 31 December 2018 & the payment date shall be 15 February 2019.

For the quarter ended September 2018, the total hike in the average daily traffic (ADT) was 3.3%. The Sydney’s average daily traffic (ADT) surged by 2.5% to 6,81,000 trips, this was on the back of increased large vehicle trips, with total trips on M4 West being 1,40,000 trips, with large vehicles representing 8.10% of the trips. Moreover, the company achieved an EBITDA (excluding significant items) growth of 10.2% during FY 2018 on a YoY basis and thus stood at $1,796 Mn. This was on the back of growth in strong large vehicle traffic & due to full year impact of CTW large vehicle toll multiplier increase. The average daily traffic growth for the FY 2018 was 2.2%.

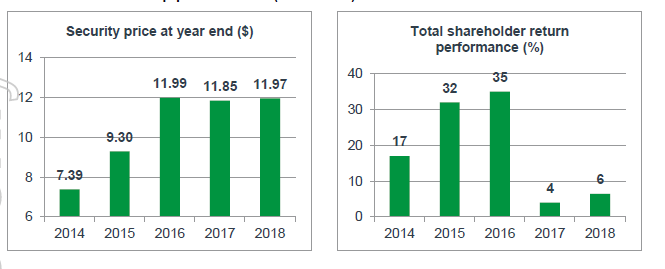

TCL’s Total shareholder Return (TSR) (Company Reports)

Meanwhile, the stock price has fallen by a marginal 0.51% over the past six months as on 19 December 2018. Hence considering the constant growth seen in the ADT and the decent EBITDA growth, we maintain our “Buy” recommendation on the stock at the current market price of $11.70.

Westpac Banking Corporation

Robust Net Interest Income: Westpac Banking Corporation (ASX: WBC) has via a recent release stated that the bank has successfully completed the Offer of Westpac Capital Notes 6 (Notes). Approximately 14.2 million Notes were issued at $100 each, raising approximately $1.42 billion. The confirmations regarding the allocation shall be done by the 21st December 2018. These notes are expected to commence the normal settlement trading on ASX under the code WBCPI from the 24th of December 2018. Moreover, the bank has notified that the distribution payment of A $0.79560 with dividend distribution rate of 1.9854% per annum WBCPD - CAP NOTE 3-BBSW+3.20% PERP NON-CUM RED T-03-19 and it will be paid on March 08, 2019 with the record date of 28 February 2018.

.png)

WBC’s Total Shareholder Return and ROE (Source: Company Reports)

As per the recent pillar 3 report, CET1 came in at 10.63% as at 30 September 2018. This was an improvement of 13 bps from the levels at 31 March 2018. The improvement in the capitalization was on account of the increase in cash earnings & conversion of preference shares to common equity. On the financial metrics, the company has Net Interest margins of 2.13% as compared to the 1.94% which is the Industry median. This shows that the bank has invested its funds more effectively as compared to the industry as a whole. Also, on the valuation front, the bank has got a dividend yield of 7.32% as compared to the banking industry median of 6.20% which shows the stock still has gained enough value left at these levels. Meanwhile, the stock price has fallen by 13.11% over the past six months as on 19 December 2018, thus posing an attractive opportunity for the investors to acquire the stock at these levels. Hence considering the robust NIM’s and strong Dividend yields, we maintain our “Buy” recommendation on the stock at the current market price of $24.07.

Paragon Care Limited

Significant market opportunities in Australia and New Zealand:Paragon Care Limited (ASX: PGC) has commenced with a critical review of its business segment namely “capital equipment”, in line with its undergoing transformation programme. This segment is expected to deliver ~10% of the company’s forecasted FY 19 revenues of $260 Mn. This strategic review is expected to decipher into aspects such as the evolution of this segment, keeping in mind the increased focus on innovative technologies and its potential to generate revenues on a continuous basis. The firm’s top line for the FY 2018 expanded by 17% and thus clocked at $136.7 Mn. This was mainly driven by the acquisition of “Total communications” which has aided in accretion of the high-technology revenues. At present, the total healthcare market spending in Australia & New Zealand is $193 Bn p.a. & firm’s addressable market is of $9 bn p.a. which is anticipated to grow at a rate of 6% p.a. Hence, moving further the company expects better opportunities & expansion in its market share.

PGC’s few of the established brands (Source: Company Reports)

The company is trading at an EV/Sales multiple of 1.0x while the industry median stands at around 5x, which indicates that the company is undervalued considering the sales it is generating. Also, the company’s dividend yield ratio is 4.92% which is decent enough & above the Industry median of 1.80%. These parameters suggest that the stock is trading cheap at the current market price. Meanwhile, stock price has fallen by 28.41% over the past six months period as on 19 December 2018. Hence considering growth in revenues and robust dividend yields, we maintain our “Speculative Buy” recommendation on the stock at the current market price of $0.610.

Boral Limited.

Strong EBITDA Margins: Boral Ltd (ASX: BLD) has started to gain footprints in North America due to the acquisition of Headwaters, hence a 20% EBITDA growth is expected from that market post the sale of its block business in FY19. The USG Boral is expected to see a growth of 10% in FY19 against FY18. This guidance is on the premise that the Non-residential demand would gain traction & increase by 10% steering over the impacts of the softening housing construction market. For the Q1 2019, the Boral Australia’s Infra and commercial activity showed robust signs. This was due to the moderation seen in the residential segments. As regards Boral North America, there were significant delays in construction activity due to very heavy rainfall leading to project delays. Based on robust growth in FY18, the company awarded a dividend of 26.5 cents per share, franked as to 50%. This represents a payout of 66% which is in line with the company’s dividend policy.

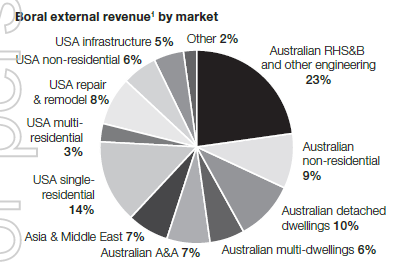

Boral’s Revenue by Geographical Segments (Resource: Company reports)

The company is trading at an EV/Sales multiple of 1.40x while the industry average stands at around 2x times, which indicates that the company is trading at a cheap valuation. At the current price, dividend yield of the company’s dividend stands at 5.34% which is decent enough. Hence these parameters suggest that the stock is trading cheap at the current juncture. Meanwhile, the stock price has fallen over the past six months by 21.27% as on 19 December 2018. Thus, considering strong operating performance from the various geographical segments and expanding EBITDA margins, we reiterate our “Buy” recommendation on the stock at the current market price of $4.81 (3.024% down on 20 December 2018).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...