Saracen Mineral Holdings Limited

.JPG)

SAR Details

Boost from macro-economic scenario: Saracen Mineral Holdings (ASX: SAR) witnessed a stock price rise of 5.8% on 29 August 2017, as investors latched on to the safe haven stocks and avoided riskier investments post North Korea’s move on firing a missile over Japan. Recently, SAR has reported robust financial and operational results for the year to 30 June 2017. Revenue surged 53% yoy to A$423.1m (FY16: A$276.5m) while EBITDA grew 54% to a record A$113.4m (FY16: A$73.5m). Accordingly, Underlying NPAT moved up 25% to A$33.7m (FY16: A$26.9m) led by increased gold sales of 266,556 ounces (FY16: 188,024 ounces) and a strong Australian-dollar gold price. Depreciation and amortisation more than doubled to A$74.7m (FY16: A$33.9m) primarily due to Thunderbox A Zone, Karari and Deep South operations being in commercial production for their first full financial year in FY2017. At the end of the year, the Company held cash and bullion of $45.2 million, up from A$40.3 million a year earlier, with no debt. This was after spending A$138.9m during the period on project development and exploration. The substantial increase in cashflow and earnings marks a pivotal year of transition for Saracen and highlights the growth over the next three years as production increases and costs fall.

.png)

Key financial and operating results; (Source: Company Reports)

During the year, approximately A$15.7 million of gold sales were made from gold recovered from development activities at the King of the Hills underground mine. However, this amount was offset against the project’s capital development costs and is not accounted for as sales revenue. Moreover, the substantial investment that the company has made in growing inventory and production is now reaping rewards. The company maintains its production outlook for FY18 remains ~300,000oz at an AISC of A$1,150/oz. Given the prospects and macro-economic environment, we maintain a “Buy” recommendation on the stock at the current market price of $ 1.35

Doray Minerals Limited

.JPG)

DRM Details

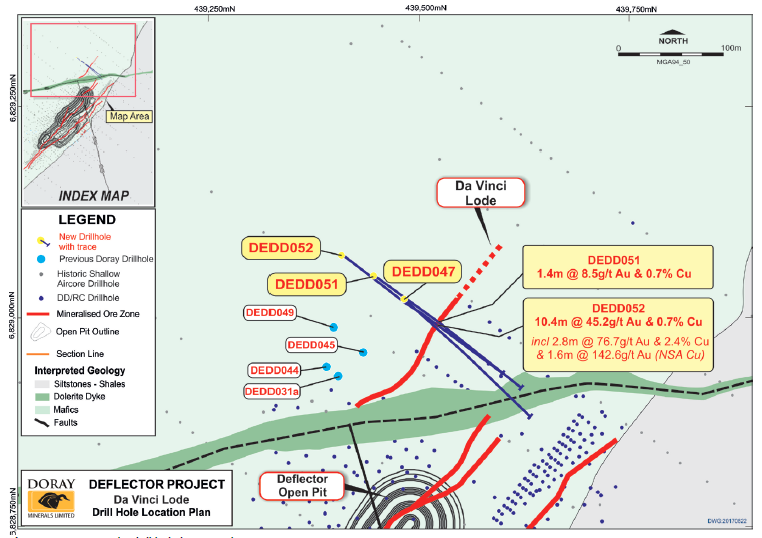

Exceptional assay results at Da Vinci: Shares of Doray Minerals Limited (ASX: DRM) surged 7.3% on 29 August 2017, along with the boost in other gold stocks given the global economic scenario. The company has also announced further exceptional assay results from drilling at the new Da Vinci discovery, located immediately north of the Deflector Gold Copper mine. These holes have now returned outstanding gold and copper assays, confirming the high-grade nature of this new discovery, with DEDD052 returning 10.4m @ 45.2g/t Au and 0.7% Cu from 226m, including 2.8m @ 76.7g/t Au and 2.4% Cu and 1.6m @ 142.6g/t Au (No significant Cu); and DEDD051 returning 1.4m @ 8.5g/t Au and 0.7% Cu from 143.5m. With these continuing spectacular grades and mineable widths so close to underground development, Da Vinci is looking like being a serious game changer for Doray Minerals.

Da Vinci Lode drill hole location plan; (Source: Company Reports)

In addition, DEDD052 intersected significant high-grade structures further into the footwall of the main zone of mineralisation (0.6m @ 7.5g/t Au from 296m and 0.7m @ 55.4g/t Au from 299.2m). These intersections potentially represent mineralised splay structures off the main lode. Importantly, this pattern of mineralisation is commonly seen within the main Deflector ore system. Assay results from DEDD047 returned 0.4m @ 1.3g/t Au and 0.4% Cu from 82.9m indicating the persistence of mineralisation towards surface. All holes were drilled along strike from the previously announced 7.5m @ 29.7g/t Au from 235.5m in hole DEDD049, demonstrating at least 120m of continuity of these exceptional grades that are completely open along strike and at depth. Drilling has commenced on a new deeper diamond drill hole, a further 80m north along strike. In addition, RC drilling has commenced on the prospect to rapidly test the strike extent of the system and the near surface potential. The stock has declined 40% over the past six months while it is down 72.3% in the last one year (as at August 28, 2017), owing to suspension of its Andy Well Gold Mine operations and weak financials. We maintain an “Expensive” recommendation at the current price of $ 0.22

Caltex Australia Limited

.JPG)

CTX Details

Decent Supply and Marketing Earnings: For the six months ending 30 June 2017, Caltex Australia Limited (ASX: CTX) reported 21% growth in Replacement Cost Operating Profit (RCOP) at $307 million on the previous corresponding period. As a result, the stock edged slightly up about 1% post the result release. CTX continues to make solid progress with its convenience retail program and with the company’s operating model review which has identified an initial $60 million annual cost saving. On HCOP (Historic Cost Profit) basis, Caltex’s after-tax profit was $265 million for the first half of 2017, including a net $2 million gain on significant items. Significant items represent the profit on sale of Caltex’s fuel oil business, offset by the establishment of the previously announced $20 million Franchisee Employee Assistance Fund. First half HCOP NPAT was of the order of $265 million (including $44 million after tax inventory losses) and RCOP NPAT of $307 million, was up 21% (excluding significant items). The interim HCOP result of $265 million is down 16% on the $318 million after tax profit for the first half of 2016 as the 2017 half year result includes crude and product inventory losses of $44 million after tax, compared with crude and product inventory gains of $64 million after tax for the half year to 30 June 2016.

.png)

Results summary; (Source: Company Reports)

Supply and Marketing delivered an EBIT result of $377 million, which includes unfavourable externalities of $4 million, comprising a price timing lag gain of $13 million (2016 first half: a price timing lag loss of $8 million) less a realised loss on foreign exchange of $17 million (2016 first half: a realised loss of $2 million). Excluding these externalities, the underlying Supply and Marketing EBIT increased 6% to $381 million, comparing favourably to the first half 2016 EBIT of $359 million. Lytton Refinery delivered an EBIT of $149 million in the first half, compared with an EBIT of $92 million for the first half of 2016. We maintain a “Hold” rating on the stock at the current market price of $ 33.75

Downer EDI Limited

.JPG)

DOW Details

Downer closes its offer to acquire Spotless: Shares of Downer EDI Limited (ASX: DOW) moved up 2.0% on 29 August 2017 after the company reported better than expected results. For the 12 months ended 30 June 2017, total revenue for the Group increased by 5.7% to $7.8 billion. Transport revenue increased 16.4% to $2.2 billion due to continuing strong performance on existing contracts, improved contribution from Infrastructure Projects, including Newcastle Light Rail, and the acquisition of RPQ. Utilities revenue increased 19.1% to $1.5 billion, led by new contracts in the renewable energy, power & gas, water sectors in Australia and New Zealand and strong contributions from nbn contracts in Australia and the Chorus contract in New Zealand. Rail revenue increased 2.9% to $850.2 million driven by the Sydney Growth Trains (SGT) and High Capacity Metro Trains (HCMT) projects and the sale of locomotives. However, these improvements were offset by the completion of freight build manufacturing contracts. EC&M revenue increased 6.2% to $2.0 billion due to increased activities on the Wheatstone project and contribution from the Hawkins acquisition, offset by significant projects completed in the prior year not being fully replaced. Mining revenue decreased 18.5% to $1.3 billion mainly as a result of the completion of the Christmas Creek contract in September 2016. On the other hand, total expenses increased by 6.7%

.png)

Financial summary; (Source: Company Reports)

EBIT for the Group increased 0.3% to $277.8 million, with increased earnings in Transport and Rail offset by the impact of contract completions not fully replaced in Mining and EC&M. Statutory Net Profit After Tax (NPAT) for the Group increased 0.5% to $181.5 million. This included a pre-tax $19.8 million fair value gain on revaluation of the initial 19.99% investment in Spotless and other income, offset by $15.2 million of Spotless transaction costs. Excluding the impact of the Spotless transaction, NPAT was $181.4 million with no operating earnings from Spotless included in this result as it is considered not material to the Downer Group. Downer has also closed its offer to acquire Spotless and currently owns 87.8% of the group.

The stock has moved up 48%, 3.9% over the past twelve months and six months, respectively, led by strong financials and optimistic outlook. Given the current trading at elevated levels, we give an “Expensive” recommendation on the stock at the current price of $ 7.01

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...