CARSALES.COM LIMITED (ASX: CAR)

Executing strategic priorities with strong growth: Recently, Carsales issued 5,504 of fully paid ordinary securities while Pinnacle Investment Management Group Limited and Pinnacle Investment Management became the substantial holder by holding 13,917,629 of securities with 5.82 per cent of the voting power. Mr Jeffery Browne, a reputed Board member retired from the Board effectively from 23 March 17 and Mr Richard Collins, previously Deputy Chair of the Board will assume his responsibilities. Group released its first half results of 2018 and reported an increase of 12 per cent and 9 per cent in the revenue ($200.1m) and EBITDA ($90.6m), respectively. The Board declared an interim dividend of 20.5 cents per share (10 per cent increase on pcp) and this will be paid on 19 April 2018. It completed the acquisition of SK Encar in January 2018 by acquiring the rest of 50.1 per cent interest. CAR expects that its domestic adjacent business will continue to build scale and breadth that will be consistent with H1FY18 and its premium listing and depth products will continue to grow well. The stock price was up by 9.15 per cent in the past six months and was down by 3.23 per cent as on 22 March 18 as the group traded ex-dividend. The stock still looks “Expensive” at the current market price of $14.09

.png)

Revenue Performance (Source: Company Reports)

HUON AQUACULTURE GROUP LIMITED (ASX: HUO)

Strong First half performance: IOOF Holdings Limited became the substantial holder of Huon Group by holding 5,380,424 of securities with 6.161 per cent of the voting power since 22 February 18. The Group released the results of first half of 2018 and reported an increase of 28 per cent in revenue as compared to the first half of prior year. The revenue was in line with higher volumes and reflected a continued strength in domestic salmon prices. It was supported by good growing conditions and delivered a record of average fish weight of 5.29 kg due to improved fish diets. The overall gearing remained at 21 per cent as compared to 19 per cent in the prior corresponding period. The Company committed $85m for capital investment program to expand production. The Board declared a dividend of 5.0 cents per share (50 per cent franked) and the Group targets a pay-out ratio of not more than 35 per cent of operating net profit after tax. It is expected that contracted sales into the export channel will increase by more than 65 per cent in 2H18. The stock price was down by 7.2 per cent in the past six months and by 2.22 per cent on March 22, 2018 as HUO traded ex-dividend. We believe the stock is still at a higher level and give an “Expensive” recommendation at the current market price of $4.41

.png)

Operational Performance (Source: Company Reports)

WEBJET LIMITED (ASX: WEB)

Fastest growing B2B Player: Commonwealth Bank of Australia (substantial holder) earlier acquired 8,685,828 of securities and was holding 7.31 per cent of the voting power and now it holds 10,061,647 of securities with 8.47 per cent of the voting power. Meanwhile, WEB’s Total Transaction Value and Total Revenue were up by 55 per cent and by 290 per cent for the period of 6 months ending 31 December 17, amounting to $1,443 million and $359.8 million, respectively. The ongoing growth of the Webjet OTA business with flight bookings continued to outperform the market by more than 4 times and reflected a strong growth for the ancillary products. The flight bookings (both domestic and international) for the period (6 months ending 31 December 17) were up by 11 per cent as compared to PCP. EBITDA grew by 26 per cent. An interim dividend of 8.0 cents was declared. The Group expects to deliver EBITDA of more than $80 million for full year. However, EBITDA margin has been impacted by the loss of credit card surcharges. The stock price climbed up by 7.38 per cent in the past six months but was down by 5.5 per cent on 22 March 18 while it is yet to trade ex-dividend on March 27, 2018. This drop seems to be linked to some negative sentiments erupting on the stock with market developments. By looking at the overall scenario, the stock seems “Expensive” at the current market price $11.42

.png)

Cash Flow Performance (Source: Company Reports)

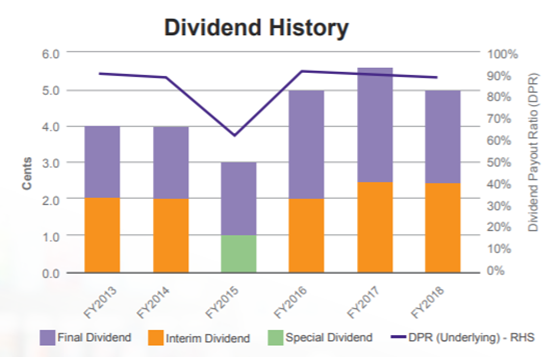

SIGMA HEALTHCARE LIMITED (ASX: SIG)

Bleak full year result: Sigma has declared a soft full year result, and the Board declared a final dividend of 2.5 cents per share, which will be paid on 20 April 2018. It reported a rise of 3.5 per cent in EBIT that amounted to $83.7 million for FY18 and whereas underlying EBIT was down by 10.0 per cent and amounted to $90.3 million. This was in line with the guidance which was provided earlier to the market. It focussed on ROIC that amounted to 16.6 per cent which was a decent return during the Company’s investment cycle. Sigma’s Investment in Project Renew continued and it is expected that it will derive operational efficiencies which will enhance its capacity and ability to serve customers in a better way. It completed the construction at Berrinba in Queensland and began its operations in February 18. It acquired MPS recently and MPS provided aid for its administration services and provided support in the aged care. It initiated a buy-back program and has already bought back over 130 million of shares and raised 14.6 million. The stock price was down by 7.4 per cent as on 22 March 18 at the back of the result. Looking at the revenue and profit dip (5.4 per cent and 10.5 per cent, respectively), the stock looks “Expensive” at the current market price of $0.815

Dividend Trend (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...