Oil Search Ltd (ASX: OSH)

.png)

OSH Details

Rise in dividends: Oil Search, which focuses on Papua New Guinea, has reported for a record growth in full-year 2017 net profit at the back of high production and stronger commodity prices (average realised oil and condensate price up 24% and LNG and gas prices 21% higher). Up 236%, OSH’s net profit for 2017 soared to $US302.1 million ($382 million); and based on the result, the group declared a final dividend of US5.5 cents taking total dividends to US9.5 cents against US 3.5 cents in 2016. It is worth noting that the 2017 dividend payout ratio of 48% is at the upper end of Oil Search’s dividend guidance range of 35% - 50% of core net profit after tax and is not subject to a deduction for PNG withholding taxes. Total unit production costs were also competitive at US$8.67/boe and the operating margin was 73%. Group’s 2P Reserves and 2C Resources life is 45 years in view of the 2017 production of 30.3 mmboe. With regards to the outlook, 2018 production is expected to be between 28.5 and 30.5 mmboe with unit production costs within the range of US$8.50–9.50/boe, while unit depreciation and amortisation guidance is US$11.50–12.50/boe. Total capital expenditure for 2018, excluding Alaskan acquisition costs, is expected to be between US$475 million and US$575 million and will be funded from operating cash flows and existing cash balances, along with funds from existing corporate facilities, if required.

.png)

2018 Guidance (Source: Company Reports)

However, OSH 2018 capex is forecasted to be higher owing to activity on growth projects in view of the evaluation at Muruk, Barikewa and Kimu wells, an extensive seismic programme in PNG, pre-FEED and FEED activities on LNG expansion and exploration and appraisal activities in Alaska. We maintain a “Hold” on the stock at the current price of $7.55

.png)

OSH Daily Chart (Source: Thomson Reuters)

Senex Energy Ltd (ASX: SXY)

.png)

SXY Details

Completion of Asset Portfolio Review: Senex Energy, oil and gas small-cap player, slipped by 1.4% on February 20, 2018 as the group indicated that its first-half earnings to be released during the week will see an impact of $80 million owing to write-downs of its non-core assets in the Cooper Basin, planned to be sold or abandoned. This move has been a part of SXY’s strategy to prioritise its projects and focus on East Coast Gas development based on bagging the acreage in Queensland while the group does not intend to allocate any capital on other permits. The group has highlighted that its east coast gas business will drive major production and earnings growth from 2019 and the requirements at Atlas Project from which gas delivery is expected from 2019 are capital-intensive laden for which asset selection has been figured out as the solution to move forward. Thus, the non-core permits are said to be impaired by an amount of about $80 million. Meanwhile, the group’s December 2017 quarterly report had indicated 11% rise in net production to 200,000 boe on the prior quarter with the first full quarter's contribution from the Marauder-1 well and initial gas volumes from the Western Surat Gas Project Phase 2 wells. SXY had then identified more than 15 exploration drilling targets in the Cooper Basin western flank from the newly interpreted Liberator 3D seismic survey. While potential is high, we look forward to the earnings update due on February 22, 2018, and give a “Hold” at the current price of $0.36

.png)

SXY Daily Chart (Source: Thomson Reuters)

Origin Energy Ltd (ASX: ORG)

.png)

ORG Details

Improved Earnings: Origin Energy’s half year 2018 results indicated for 43% increase in operating cashflow from continuing operations with revised 31 December 2017 carrying value of $279m. ORG had received net cash flow from Australia Pacific LNG of $116m. The non-cash post-tax impairment charge of $173m impacted the profit partially. ORG’s Energy Markets Underlying EBITDA increased by $156m or 21% to $891m while Integrated Gas Underlying EBITDA (excluding Lattice Energy) increased by $343m to $630m, up 120%. This was partially offset by a $187m increase in interest, tax, depreciation and amortisation. The group’s underlying profit was significantly up but impairments led ORG report for a statutory loss ($207 million). On the other hand, the natural Gas gross profit margin increased to $2.80/GJ from $2.70/GJ in HY2017. The group now aims to reduce its upstream costs at APLNG with focus on simpler model and improving productivity. ORG is also focussing on its customer experience via digital channels for an easy interaction and new product offers and innovative solutions.

.png)

Significant jump in underlying profit (Source: Company Reports)

Meanwhile, the group announced for plans to redeem the EUR500m Capital Securities due 2071 (2071 Capital Securities) issued by Origin Energy Finance and listed on the London Stock Exchange at their first call date (16 June 2018) in accordance with the terms of those securities. We maintain a “Hold” at the current price of $9.22

.png)

ORG Daily Chart (Source: Thomson Reuters)

Pearl Global Ltd (ASX: PG1)

.png)

PG1 Details

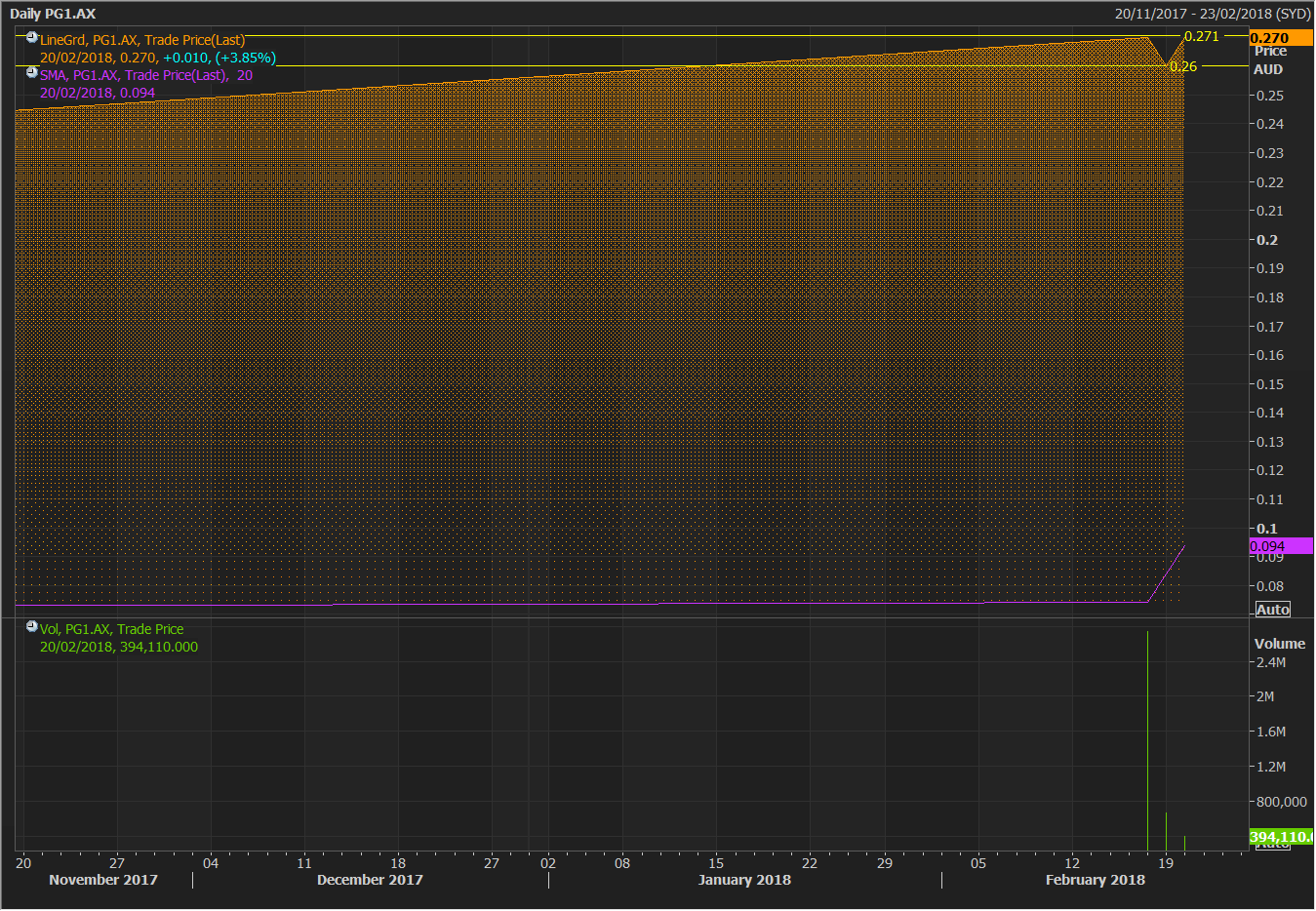

First of a kind for treating rubberfor valuable products: Up 3.8% on February 20, 2018, Pearl Global Ltd (ASX: PG1) has started commissioning its first production plant at the back of state government, environmental and council approvals received for its unique process to convert waste tyres into valuable secondary products. PG1 is said to be the first company in Australia to receive licenses for the thermal treatment of rubber that involves applied heating process called thermal desorption to cleanly convert end of life tyres into products including liquid hydrocarbon, high tensile steel and carbon char. The process that relates to low emissions, with no hazardous by-products and chemical intervention needed, is gaining traction in the industry. It has been indicated that at full production, each Thermal Desorption Units can process approximately 5,000 tonnes of shredded rubber per annum (equivalent of around 500,000 car tyres) which provides on average an annual output of 1.5 million litres of raw fuels, in the form of liquid hydrocarbons. The group is yet to move to field trials while it is moving to full production soon. PG1 has a cash payment of $542,000 from the Australian Taxation Office for research and development incentive claims in its 2016/2017 taxation return. While we do see some potential, but the risk level is high. We give a “Speculative Buy” recommendation at the current price of $0.27

PG1 Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...