.png)

Stocks’ Details

Origin Energy Limited

Changed Credit Rating from BBB- (positive) to BBB (stable): Origin Energy Limited (ASX: ORG) noted the decision by Standard & Poor’s Global Ratings (S&P) to upgrade its long-term senior unsecured credit rating for the company to BBB (stable) from BBB- (positive). At the same time, S&P upgraded the senior unsecured credit rating for Origin Energy Finance Limited to BBB (stable) from BBB- (positive).

.png)

Strong Performance HY 2019 (Source: Company Reports)

The statutory profit stood at $796 million for HY1FY19. During the period, the underlying EBITDA of the company stood at $1,727 million, with an underlying profit of $592 million, which reflected a higher oil linked revenue in integrated gas and reduced financing costs from lower debt and a lower average interest rate.

Guidance Going Forward: In FY 2019, the company expects higher underlying profit compared to FY2018 and further debt reduction. The breakeven guidance update primarily includes lower capex due to well cost savings, scope and timing changes. The higher operating expenses due to additional gas purchases to offset reduced non-operated production. The Energy Markets guidance is unchanged, with Underlying EBITDA expected to be in the range of $1.5 to $1.6 billion.

With a stronger balance sheet, upgraded credit rating along with robust financial performance over the first half of FY19, the outlook for the company looks decent.

Moreover, with a YTD return of 15.35% and the stock trading slightly closer to its 52-week low range, proffering a decent opportunity for accumulation. Hence, we maintain our “Buy” rating on the stock at CMP of $7.290 per share.

Rio Tinto Limited

Guidance Reduced For Pilbara Shipments In FY19: Rio Tinto Limited (ASX: RIO) faced several challenges in its iron ore business during the commencement of the year, precisely on the back of tropical cyclones due to which the 2019 guidance for Pilbara shipments is reduced to between 333 and 343 million tonnes. The quarterly operational performance in other product lines was however solid, generally higher than the previous year.

.png)

Financial Review FY18 (Source: Company Reports)

The underlying earnings of the company stood at $8.8 billion in FY18 as compared to $8.6 billion in 2017. However, growth in the end-markets was relatively subdued and inflationary pressures increased in some of the company’s product groups. The underlying EBITDA of the company stood at $18.1 billion, decreased by $0.4 billion from 2017 primarily on the back of higher volumes of iron ore and copper and higher prices for aluminium and copper being offset by lower iron ore prices, the coal divestments, and rise in energy and raw material costs.

Outlook: The company expects the markets to remain volatile, with some risk of a trade war and a deceleration in economic activity. The company continues its strong focus on value over volume, growth and mine-to-market productivity with partnership and sustainability remaining important priorities. It seeks to allocate capital with discipline, to continue delivering superior returns to its shareholders.

The stock is currently trading closer to its 52-week high price indicating a probable factoring of positive results and financials in its current stock price.Therefore, the market should look out for further growth catalysts moving forward. Hence, we maintain our “Expensive” rating at CMP of $101.200 per share (up 0.447% on 16 April 2019).

Eclipx Group Limited

Strong Growth In NOI: Eclipx Group Limited (ASX: ECX) announced that Garry McLennan has advised the Board of his intention to retire from the company in six months, or earlier if a successor is appointed. Mr McLennan has been Chief Financial Officer and an Executive Director of Eclipx since January 2014. He will step down from the Board immediately.

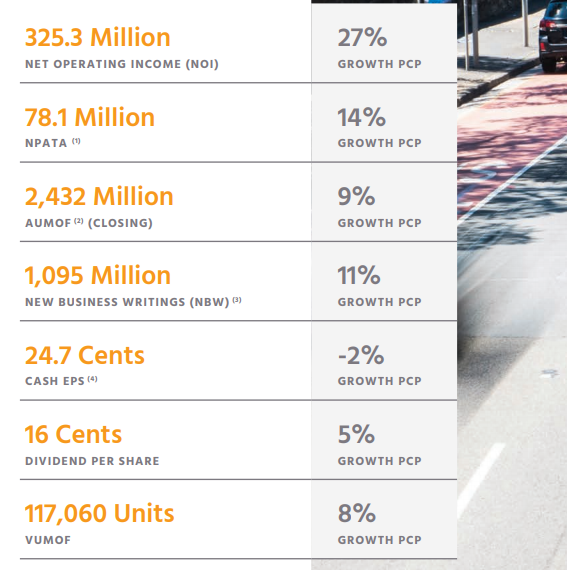

Financial Highlights FY18 (Source: Company Reports)

The net operating income increased by 27% to $325.3 million for the year and Group Net Profit After Tax adjusted for Amortisation and One-off Costs (NPATA) improved by 14% to $78.1 million in FY18.The cash NPATA has increased by $9.8 million as a result of an increase in statutory earnings $8.0 million, increase post tax adjustments of amortisation of intangibles associated with the acquisition of Grays and software $2.3m and a decrease in restructuring and acquisitions related costs of $0.5m post tax.

Guidance for FY19: The company currently expects its net profit after tax and before amortisation for FY19 will be broadly in-line with reported FY 2018 NPATA. The estimated net profit before tax for FY19 is expected to show higher growth when compared to Eclipx’s pro forma pre-tax FY18 results driven by the average corporate tax rate for FY18 being 25% compared to the estimated FY19 corporate tax rate of 29%.

With solid financial performance Y-o-Y backed by improvement in NOI, NPATA and efficiency ratio, the outlook for the company looks stable.Moreover, the stock is trading slightly closer to its 52-week low of $0.540. Based on the foregoing, we maintain our “Hold” recommendation on the stock at the current market price (CMP) of $0.905 per share (up 9.036% on April 16, 2019).

Blackmores Limited

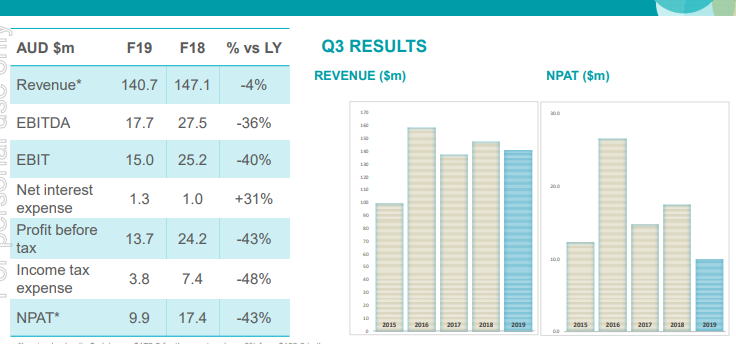

Significant Decrease In Profits On Pcp: Blackmores Limited (ASX: BKL) announced its third quarter results for FY19.

Third Quarter FY19 Results (Source: Company Reports)

The profit for the first nine months stood at $44 million, down 14% compared to the prior corresponding period (pcp), with revenue of $460 million, up by 6% on pcp.The profit for the quarter ending 31 March 2019 was $10 million, down 43% compared to pcp. Revenue was $141 million for the quarter, down 4% (on pcp). The key margins of the company remained under pressure against the pcp.

Future expectations: The company does not expect the second half profit performance to be ahead of the first half result.The company is accelerating its plan to streamline the business and target $60 million in savings over three years. Implementation will incur some one-off costs in Q4.

The YTD returns remained negative for the stock at 28.39%. Moreover, the company’s financials were down, and margins were under pressure against pcp. Thus, we have a wait and watch stance on the stock at the current market price of $88.300 (down 1.561% on 16 April 2019).

.PNG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...