.png)

Stocks’ Details

G8 Education Limited

Revenue for H1CY19 up by ~9% Year Over Year: G8 Education Limited (ASX: GEM) is involved in providing quality care and education services in Australia and Singapore. It is engaged in the business of ownership of early education centre franchises and operations, which are owned by the group.

G8 Revealed Completion Of 25 Centres in WA: The company recently announced the completion of sale of its 25 centres in Western Australia to Sparrow Early Learning Pty Ltd for approximately $6.4 million.

H1CY19 Key Takeaways for the Period Ended 30 June 2019: The company reported total revenue of $430.6 million, up 8.6% year over year, primarily due to occupancy, fee growth and acquisitions. Profit for the period came in at $19 million, down 20% year over year. The decrease was due to the implementation of the new accounting standard. Underlying EBIT for the period came in at $51.6 million, up 7.3% year over year.

.png)

Financial Highlights (Source: Company Reports)

What to Expect: The company is expecting occupancy growth of approximately 1% pts in CY19. In CY19, the company anticipates underlying EBIT to be in the band of $131 million - $134 million. The company expects the new rostering platform to be completed in May 2020, which is anticipated to bring further wage efficiencies.

Valuation Methodology: Price to Cash Flow Multiple Approach

.png)

rice to Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock gained 4.55% in the past one month. Currently, the stock is trading below the average of its 52-week high and low level of $3.635 and $1.832, respectively. As on 03 January 2020, the company’s market capitalisation stands at ~$899.65 million, with 460.18 million outstanding shares. Considering the decent outlook and current trading levels, we have valued the stock using Price to Cash Flow based relative valuation method and have arrived at a target price with an upside of lower double-digit in % terms.Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of $1.955 per share as on 06 January 2020.

Ainsworth Game Technology Limited

AGI Targeting Long-Term Growth:Ainsworth Game Technology Limited (ASX: AGI) is involved in growth, rental, production, sales and servicing of gaming machines and other associated equipment and services. On 5th December 2019, the company announced that Spheria Asset Management Pty Ltd, a substantial holder of the company, has increased its voting power from 5.16% to 6.23%.

Key Takeaways for FY19 Period Ended 20 June 2019: The company reported total revenues of $234.3 million, down 11.8% year over year. Profit for the year came in at $10.9 million as compared to $31.9 million reported in the year-ago period. Net cash at the end of FY19 was $6.2 million.

.png)

FY19 Financial Highlights (Source: Company Reports)

What to Expect: The company remains confident on driving enhanced long-term growth by focusing on R&D and combining organic performance with selective purchases to bring in financial efficiencies.

Valuation Methodology: Price to Cash Flow Multiple Approach

.png)

Price to Cash Flow based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock gained 12.7% in the past 6 months. Currently, the stock is trading above the average of its 52-week high and low level of $0.905 and $0.590, respectively. As on 06 January 2020, the company’s market capitalisation stands at ~$254.28 million, with 336.79 million outstanding shares. Its quick ratio and current ratio for FY19 stood at 4.3x and 5.79x, better than the industry median of 0.99x and 1.08x, respectively, which implies the company’s good liquidity position. Considering the backdrop of the above factors, We have valued the stock using P/CFbased relative valuation method and for the purpose, have taken the peer group - Aristocrat Leisure Ltd (ASX: ALL), Star Entertainment Group Ltd (ASX: SGR) and Crown Resorts Ltd (ASX: CWN). Therefore, we have arrived at the target price with an upside of single-digit in % terms.Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.785 per share, up 3.974% as on 06 January 2020.

Seven West Media Limited

Terminated the Scheme Implementation Deed: Seven West Media Limited (ASX: SWM) is engaged in offering free to air television and radio broadcasting, newspaper and magazine publishing. Recently, the company informed that the Spheria Asset Management Pty Ltd became a substantial holder of the company, with a voting power of 6.23%.The company also stated that together with Seven Network (Operations) Limited and SWM’s other subsidiaries, it became a substantial holder in Prime Media Group Limited with a voting power of 14.9%.

Other Recent Updates: On 19 December 2019, the company announced the issuance of 30,000,000 ordinary shares in the Company to Spheria Asset Management Pty Limited. In another update, the company informed that it has terminated the Scheme Implementation Deed with Prime Media Group Limited, due to non-approval of necessary majorities of Prime Media Group’s shareholders.

FY19 Key Takeaways for the Period Ended 29 June 2019: The company reported revenue for the period of $1,552.9 million, down 4.2% year over year. The company reported a net loss of $444.4 million in FY19 against a profit of $132.8 million in FY18. The company exited FY19 with cash and cash equivalents of $90.455 million.

.png)

FY19 Financial Highlights (Source: Company Reports)

Outlook: For FY20, the company expects underlying EBIT to be in the range of $190 million to $200 million. In addition, the company expects Broadcaster Video on Demand (BVOD) market growth to be more than 25%.

Valuation Methodology: Price to Book Multiple Approach

Price to Book Value based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading below the average of its 52-week high and low level of $0.595 and $0.310, respectively. As on 06 January 2020, the company’s market capitalisation stands at ~$515.24 million, with 1.54 billion outstanding shares. The company targets to reduce costs across the group, thereby enhancing operational efficiency. Further, the company remains on track to improve its balance sheet and reducing overall debt. Considering the backdrop of the above factors, we have valued the stock using P/BVbased relative valuation method and for the purpose, have taken the peer group - REA Group Ltd (ASX: REA), Nine Entertainment Co Holdings Ltd (ASX: NEC) and Telstra Corporation Ltd (ASX: TLS). Therefore, we have arrived at the target price with an upside of lower double-digit (in % terms).Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.325 per share, down 2.985% as on 06 January 2020.

Retail Food Group Limited

New Business to Contribute ~$1 million to FY20 EBITDA:Retail Food Group Limited (ASX: RFG) is an Australia-based retail food and beverages company. The company is also involved in the expansion and supervision of the coffee roasting services, and wholesale supply of high-qualitycoffee and related products.

Business Update for Hudson Pacific Foodservice: On 3 January 2020, the company informed that the settlement transaction regarding its subsidiary, Hudson Pacific Corporation Pty Ltd has taken place. As per the deal, its subsidiary had announced a binding Term Sheet for the sale of its foodservice business and operations to Hudson Food Group Pty Ltd.

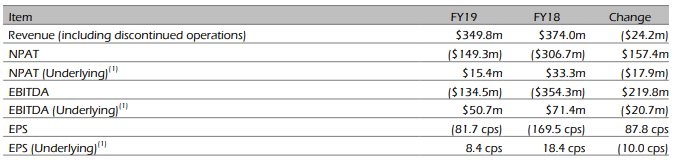

FY19 Key Takeaways for the Period ended 30 June 2019: The company reported revenue for FY19 at $349.8 million, down from $374 million reported in FY18. Underlying NPAT came in at $15.4 million, down from $33.3 million in FY18. The company’s underlying EBITDA stood at $50.7 million, as compared to $71.4 million reported in FY18.

FY19 Financial Highlights (Source: Company Reports)

Outlook: For FY2020, the company expects underlying EBITDA to be in the range of $42 million to $46 million. The company expects its new business in FY20 to contribute roughly $1 million to EBITDA.

Stock Recommendation: As per ASX, the stock is trading below the average of its 52-week high and low of $0.365 and $0.090, respectively. As on 06 January 2020, the company’s market capitalisation stands at ~$222.39 million, with 2.12 billion outstanding shares. Its gross margin for FY19 stood at 69.9%, better than the industry median of 52.8%. On the valuation front, the stock is trading at a price to earnings multiple of 8.3x as compared to the industry median of 12.2x, on TTM (Trailing Twelve Months) basis. Based on the current trading position, growth in gross margin and valuation, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.100 per share, down 4.762% as on 06 January 2020.

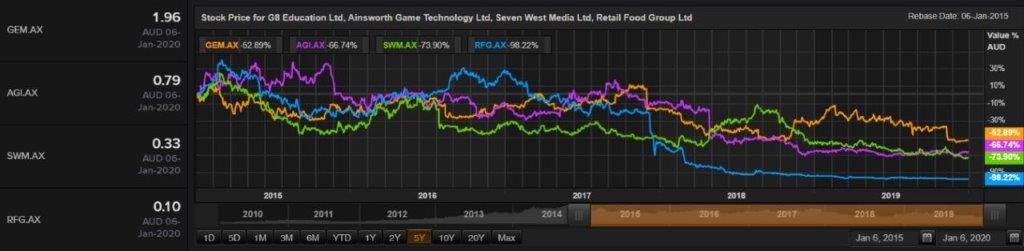

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...