.jpg)

Stocks’ Details

Syrah Resources Limited

FY20 Production Guidance at 120kt to 150kt:Syrah Resources Limited (ASX: SYR) operates in mining, exploration and distribution of graphite and related products. Recently, SYR informed that Bank of America Corporation and its related bodies corporate have increased its voting power from 5.32% to 7.75%. The change was done on December 11, 2019.

Q3FY19 Operational Highlights for the Period Ended 30 September 2019:SYR announced its quarterly results, wherein the company reported graphite production of 45kt, up from 44kt in Q2FY19. On YTD basis, total production stands at 137kt with ~50% of capacity utilization. During Q3FY19, the company improved recovery at 69% as compared to 66% in Q2FY19, aided by continued elimination of recovery constraints and a proven increase in process control and operational stability. During September 2019, the company reported 71% recovery, aided by increased production ratio of coarse flake graphite to 16% as compared to 12% in Q2FY19.

.png)

Q3 FY19 Operational Highlights (Source: Company Reports)

Outlook:For FY20, the company expects qualification of purified spherical graphite while strategically, the company will focus on customer and partnership opportunities. The company is estimating its production for FY20 within 120kt to 150kt, subject to market conditions. The company is likely to ensure its production of final anode active material and delivery to customer qualification. For Q4FY19, the company will focus on optimisation of purified spherical graphite samples for potential customers and ongoing battery supply chain engagement.

Valuation Methodology:Enterprise Value to Sales Based Approach

.png)

Enterprise Value to Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of SYR is quoting at $0.430 with a market capitalization of ~$186.07 million. At current market price, the stock is quoting at the lower end of its 52-week trading range of $0.350 and $2.048. SYR emphasized on customer engagement, while continuing to deliver valuable input into product specifications and product development opportunities. Considering the aforesaid facts, we have valued the stock using one relative valuation method, i.e., enterprise value to sales (EV/Sales) multiple and arrived at a target price of higher single digit upside (in percentage terms). Looking at the current trading levels, price movements, and macro perspective, we recommend a ‘Speculative Buy’ on the stock at the current market price $0.430, down 4.444% on 17 December 2019.

Nickel Mines Limited

Improve Production to Aid Business Prospects:Nickel Mines Limited (ASX: NIC) is in the business of nickel mining. NIC announced its full-year results, wherein the company reported sales revenue at US$64.937 million as compared to US$13.551 million in FY18. The company reported a profit of US$71.826 million in FY19 as compared to a loss of US$2.926 million in the previous financial year. During quarter ended September 2019, the company reported completion of commissioning and ramp-up phase of Hengjaya Nickel and Ranger Nickel RKEF projects. During the year, the company reported nickel pig iron (NPI) production of 42,105.8 tonnes and Nickel Metal production of 5,787.7 tonnes.

Q1FY20 Production Updates for the Period Ended 30 September 2019: NIC announced its quarterly production, wherein, the company reported NPI production from Hengjaya Nickel and Ranger Nickel projects at 72,393 tonnes as compared to 33,733.5 tonnes in June quarter.Nickel metal production, during September 2019 quarter, stood at 10,019.6 tonnes as compared to 4,697.5 tonnes in June quarter. As far as price realisation is concerned, prices of LME Nickel witnessed a sharp appreciation during the second half of September quarter.

.png)

Q1FY20 production Update (Source: Company Reports)

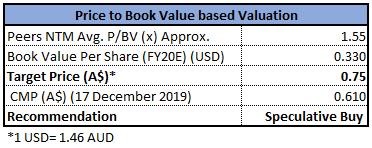

Valuation Methodology:Price to Book Value Approach

Price to Book value Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation:The stock of NIC is quoting at $0.610 with a market capitalization of ~$1.07 billion. The stock has delivered a mixed return of -12.33% and 72.97% in the last three months and six months, respectively. The stock is trading at the upper end of its 52-week trading range of $0.220 and $0.750. The business reported improvement in its price realisation during the second half of September quarter. Considering the aforesaid facts, we have valued the stock using one relative valuation method, i.e., price to book value multiple and arrived at a target price of lower double-digit upside (in % terms). Looking at the price movement, current trading levels, increased production and improved realisation, we recommend a ‘Speculative Buy’ on the stock at the current market price of $0.615, down 3.906% as on 17 December 2019.

Magnis Energy Technologies Ltd

Recent Collaboration to Aid Business Growth:Magnis Energy Technologies Ltd (ASX: MNS) is engaged in lithium-ion battery technology manufacturing across the USA and Australia along with pre-mine development of its Nachu Graphite project in Tanzania.

Binding EPC Contract with Metallurgical Corporation of China: Recently, the company informed about its collaboration with Metallurgical Corporation of China (MCC) that includes turn-key solution for The Nachu Graphite Project, which is likely to produce 240,000 tpa of graphite.The project is likely to be funded by at least 80% in debt or delayed payments.

Q1FY20 Cash Flow Update for The Period Ended 30th September 2019: MNS declared its quarterly cash flow statement, wherein the business reported net cash used in operating activities at $1.538 million, which includes $0.444 million used for exploration and evaluation, $0.41 million used for staff cost and $0.688 million for administration and corporate costs.The business reported a cash balance of $0.257 million as on 30 September 2019.

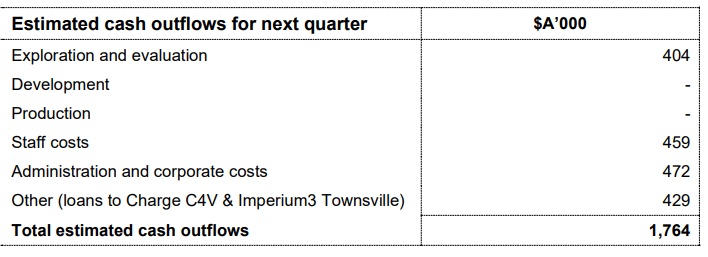

Cash Flow Guidance: As per the guidance for Q2FY20, the company estimates a cash outflows of $1.764 million, which includes $0.404 million of exploration and evaluation expense, staff costs at $0.459 million and administration and corporate costs at $0.472 million.

Q2FY20 Expected Cash Flow (Source: Company Reports)

Stock Recommendation: The stock of MNS is quoting at $0.092 with a market capitalisation of ~$57.94 million. The stock is trading at the lower end of its 52-week trading range of $0.092 and $0.375. MNS produces 99.95% pure graphite via mechanical processes, and the business is ready to cater to the anode materials market used for rapidly growing battery market. Looking at the current price movement, trading levels, recent agreement with MCC, business prospects and sector specific scenario, we recommend a ‘Speculative Buy’ on the stock at the current market price of $0.092, down by 1.075% on 17 December 2019.

Great Boulder Resources Limited

New Base Metal Target Identified:Great Boulder Resources Limited (ASX: GBR) is primarily engaged in the exploration of Gold. Recently, GBR announced that it identified a new base metals target at the Mt Venn prospect within its Yamarna Project in WA.

Q1FY20 Operational Highlight for The Period Ended 30 September 2019:GBR announced its quarterly results, wherein the company reported net cash, which is used in operating activities at $0.562 million, and net cash used in investing activities was $0.053 million. However, net cash from financing activities at $0.68 million. During the quarter, the company announced its acquisition of the 430km2 Whiteheads Project north of Kalgoorlie. It was also added that an EM survey at Mt Carlon resulted in discovery of 2 large anomalies coincident with the prospective geology.

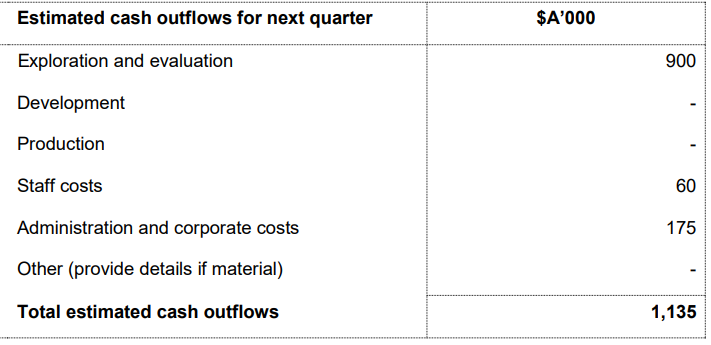

Guidance: As per the Q2FY20 estimates, the company expects cash outflows of $1.135 million, which includes $0.9 million in exploration and evaluation, followed by $0.06 million and $0.175 million in staff costs and administration and corporate costs, respectively. For FY2020, the company will commence further testing during the 2020 field season, in conjunction with other work already scheduled at Winchester and Mt Carlon. As per the guidance, this work is expected to commence during March-April 2020.

Q2FY20 Estimated Cash Flow (Source: Company Reports)

Stock Recommendation:The stock is quoting at $0.038 with a market capitalization of ~$4.8 million. The stock is trading at the lower end of its 52-week trading range of $0.035 and $0.190. The stock has generated mixed returns of 2.86% and -32.33% in the last three months and six months, respectively. Thestock isavailable at a price to book value of 0.8x on trailing twelve months basis as compared to the industry (Basic Materials) median of 1.5x. Considering the current price movement, trading levels, upcoming operating activities, identification of new target point, and business prospects, we recommend a ‘Speculative Buy’ on the stock at the current market price of $0.038, up 5.556% as on 17 December 2019.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...