.png)

Stocks’ Details

Metcash Limited

Cost Cutting Initiatives & Decent Liquidity Position are Key Catalysts: Metcash Limited (ASX: MTS) is a wholesaler to independent retailers in the food, grocery, liquor, hardware and automotive industries. The market capitalisation of the MTS stood at $2.21Bn as on 16 March 2020. Recently, MTS stated that Brad Soller has showed his intention to step down from the post of Group Chief Financial Officer in the company. Mr Soller has agreed to continue with his roles and responsibilities in the company till the appointment of a successor, which is likely to be completed by FY21 end.

H1FY20 Financial Highlights: During the period, the company’s revenue increased 1.6% year over year and came in at $6,289.8 million. Underlying EBIT stood at $149.7 million, depicting a decline of 5.3%, primarily due to lower contribution in the Food pillar from the resolution of onerous lease obligations. Underlying profit after tax came in at $95.7 million, as compared to $100.3 million in 1HFY19. The company paid a fully franked interim dividend of 6 cents per share during the period.

.png)

1HFY20 Financial Highlights (Source: Company Reports)

What to Expect: Metcash anticipates construction activity to be supported by population growth as well as undersupply of housing. The company further anticipates cost cutting initiatives to help offset the cost inflation impact over the remainder of FY20.

Valuation Methodology: P/BV Multiple Based Relative Valuation

.png)

P/B Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company is currently inclined towards its 52-week low of $2.170. Current ratio of the company stood at 1.11x in H1FY20 as compared to the industry median of 0.66x. This reflects that the company is in a decent position to address its short-term obligations against the broader industry. We have valued the stock using the P/BV based relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). For the purpose, we have taken peers such as Graincorp Ltd (ASX: GNC), Coca-Cola Amatil Ltd (ASX: CCL), Treasury Wine Estates Ltd (ASX: TWE), to name few. The stock experienced a short interest of ~12.94% (as per the ASIC report of 10 March 2020). Considering the decent liquidity position and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $2.41 per share, down 0.823% on 16 March 2020.

Orocobre Limited

Total Production for 1HFY20 up 10% Year Over Year: Orocobre Limited (ASX: ORE) is engaged in the exploration and production of minerals along with the development of potash and lithium resources in Argentina. Recently, the company announced that Svenska Handelsbanken AB Publ has become a substantial holder of the company, with a voting power of 5.14%. In another update, the company stated that Martin Perez de Solay, one of the Directors in the company, has acquired 272,813 Performance Right for nil consideration.

H1FY20 Financial Highlights for the Period ended 31 December 2019: During the period, the company’s total production came in at 6,679 tonnes of lithium carbonate, which reflects an increase of 10% on a year over year basis. The company received positive results from the Olaroz Lithium Facility with revenue amounting to US$39.4 million from the sale of 6,395 tonnes of lithium carbonate. Underlying net loss after tax stood at US$9.9 million.

.png)

Production and Price (Source: Company Reports)

Outlook: For FY20, the company anticipates production to be at least 5% higher as compared to FY19, with respect to Olaroz Lithium Facility. The company expects the average sales price of ~US$5,000 per tonne FOB for the March 2020 quarter.

Stock Recommendation: The stock of the company is currently trading below the average of its 52-week high & low level of $3.960 and $1.835, respectively. The stock posted a negative return of ~22% on a year-to-date basis. On the valuation front, the stock is trading at a price to book multiple of 0.6x as compared to the industry average of 2.2x on TTM (Trailing Twelve Months) basis. The stock experienced a short interest of ~14.17% (as per the ASIC report of 10 March 2020). Hence, considering the above factors, we give a “Buy” recommendation on the stock at the current market price of $2.12 per share, down by 3.196% on 16 March 2020.

Galaxy Resources Limited

Sneak Peek at GXY Operational & Shipping Update: Galaxy Resources Limited (ASX: GXY) is engaged in the manufacturing & production of lithium, exploration of minerals and brine assets in Argentina, Australia and Canada. The company recently updated the market with its operational and shipping activities of Mt Cattlin. The company stated that on March 11, 2020, lithium concentrates production volume of 33,000 dry metric tonnes from Mt Cattlin, was shipped from the Esperance Port. The move depicts that processing resources in China are slowly rebounding back since the trouble caused by COVID-19.

Production Outlook: The company expects lithium concentrate production volume for Q1 FY2020 to be in the band of 14,000-17,000 dmt. For FY20, the company continues to expect lithium concentrate production volume in the range of 90,000 – 105,000dmt, with grading 6.0% Li2O. Ore processed for FY20 is expected to be in the range of 900,000 – 1,000,000 wmt, with grading in the range of 1.1% – 1.2% Li2O.

.png)

Outlook (Source: Company Reports)

Stock Recommendation: For Mt Cattlin, GXY is expected to implement a lower activity mine plan focused on reducing volumes and costs to maintain promising cash margins and preserving resource life. The stock posted a negative return of ~20.9% on a year-to-date basis and is currently trading close to its 52-week low level of $0.685. On the valuation front, the stock is trading at a price to book value multiple of 0.9x as compared to the industry average of 2.2x on TTM (Trailing Twelve Months) basis. The stock experienced a short interest of ~20.11% (as per the ASIC report of 10 March 2020). Considering the corporate strategy for 2020, current trading levels and other positives, we recommend a “Hold” rating on the stock at the current market price of $0.745, down 6.289% on 16 March 2020.

Syrah Resources Limited

Restructuring Activities to Reduce Costs Remains a Key Catalyst: Syrah Resources Limited (ASX: SYR) is involved in the exploration, mining & processing of natural graphite. Recently, the company announced that Bank of America Corporation and its related bodies corporate have become a substantial holder of the company, with a voting power of 7.01%. In another update, the company issued 888,393 fully paid ordinary shares at an issue price of $0.432 per share.

Fourth Quarter Highlights for the Period Ended 31 December 2019: The company’s total Recordable Injury Frequency Rate (TRIFR) for the quarter came in at 0.6. Graphite production for the fourth quarter stood at 15kt, as compared to 45kt in the previous quarter. Material reduction in prices discovered in Q3FY19 impacted graphite production. The company sold 17kt of graphite at a weighted average graphite price of US$458 per tonne (CIF) for December quarter.

December quarter Highlights (Source: Company Reports)

Key Developments: The company initiated restructuring activities during the quarter for a balanced production. The company remains on track to achieve a target of 20% to 25% in cost reduction through its restructuring plan. The company also took initiatives topurify spherical graphite produced from Vidalia and achieved purity of more than 99.95%.

Cash Flow Highlights: During the quarter, the company reported net cash outflow from operating of US$16.601 million. Net cash outflow from investing activities stood at US$7.604 million. At the end of December 2019, SYR had cash balance of US$80.583 million.

Cash Flow Estimate (Source: Company Reports)

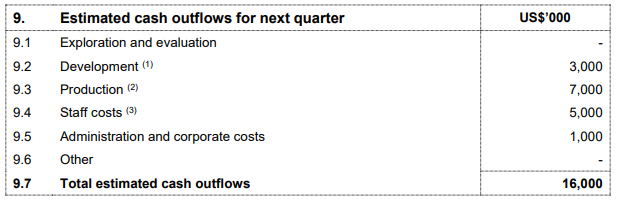

Outlook: SYR remains confident that the production at Balama will continue to be moderated through the first quarter of 2020. The plant at Vidalia will be utilized through 2020 for qualification of material in the battery supply chain and for the development of strategic and financial partnerships. For the coming quarter, the company expects total cash outflow to be ~US$16 million.

Stock Recommendation: As per ASX, the stock of SYR gave a negative return of 31.91% in the past three months. As on 16 March 2020, the market capitalisation of the company stood at ~$132.66 million. The stock is also trading close to its 52-week low level of $0.255 and offers a good opportunity for accumulation. On the valuation front, the stock is trading at a price to book multiple of 0.2x as compared to the industry median of 1.1x on TTM (Trailing Twelve Months) basis. The stock experienced a short interest of ~17.09% (as per the ASIC report of 10 March 2020). Considering the returns on stock and current trading levels, we recommend a “Hold” rating on the stock at the current market price of $0.26, down by 18.75% on 16 March 2020. The decline in share price can be attributed to supply-demand imbalance in global graphite markets.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...