.png)

Stocks’ Details

Nearmap Ltd

US Acquisition of Roof Geometry Technology: Nearmap Ltd (ASX: NEA) provides geospatial map technology for businesses, enterprises and government customers. As on 17 January 2020, the market capitalization of the company stood at $1.23 billion. The company has recently announced that it will release its financial results for the half-year ended 31 December 2019 on 19 February 2020. The company stated that it has reduced the number of restricted stock units on an issue by a total of 7,001. NEA recently acquired technology and intellectual property from Primitive LLC for a consideration of US$3.5 million. This acquisition will allow the company to extract and disseminate roof geometry from widescale 3D content along with the new type of location intelligence to customers.

Growth in Portfolio Value: In the recently held AGM, the top management stated that portfolio lifetime value went up to $1,175 million in FY19 from $983 million in December 2018. The company also witnessed continued momentum with CAGR of 12% in subscriptions.

.png)

Portfolio Value (Source: Company Reports)

Growth Opportunities: Nearmap Ltd witnessed an excellent FY19, and the Management expects continuing to execute its growth strategies. The company expects FY20 Group annualized contract value to be in the range of $116 million to $120 million. It is scaling growth and is investing in automation and analytics to identify new customers and upsell opportunities.The company is also expecting its first enterprise sales of AI content in Australia and North America in 2H20 with commercialization in MapBrowser.

Stock Recommendation: As per ASX, the stock of NEA gave a return of 7.97% on YTD basis and is inclined towards its 52-weeks’ low level of $1.785. Over the span of 4 years, the company witnessed a CAGR of 31.97% in revenue. During FY19, current ratio of the company improved from the previous year and stood at 1.63x. The stock experienced a short interest of ~12.14% (as per the ASIC report of 13 January 2020). Considering the returns, trading levels, CAGR in revenue and positive outlook, we recommend a “Buy” rating on the stock at the current market price of $2.650, down by 2.214% on January 17, 2020.

Domino's Pizza Enterprises Limited

Update on French Legal Proceedings: Domino's Pizza Enterprises Limited (ASX: DMP) is a food retailer which operates a pizza chain, comprising both franchisee-owned, and company-owned corporate stores. As on 17 January 2020, the market capitalization of the company stood at $4.9 billion. The company has recently announced the Cour de Cassation, one of the courts in France, has delivered its judgment in an appeal by Speed Rabbit Pizza (SRP) in favour of Domino's Pizza France (DPF) and has held SRP liable for disparaging DPF and ordered it to pay DPF €500,000 in damages.

Decent Rise in Revenue: In the recently held AGM, the Management stated that the company delivered strong performance with an increase in revenue by 24.4% to $1,435 million in FY19. In the same time span, NPAT (Net Profit After Tax) stood at $141.2 million, reflecting an increase of 6.1%. This led the EPS to increase by 8% to 165 cents per share.

.png)

FY19 Financial Performance (Source: Company Reports)

What to Expect from DMP: The company gave an illustration of medium-term annual growth expectations and its earnings guidance and expects same-store growth between 3% to 6% in the next 3-5 years. It also expects an increase in annual net capex of between $60 million to $100 million due to increased investment in corporate and franchise stores.

Valuation Methodology: EV/Sales Multiple Approach

.png)

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of DMP gave a return of 47.36% in the past 6 months and a return of over 6.42% in the last one month. The stock of DMP is trading close to its 52-weeks’ high level of $57.89. During FY19, gross margin of the company stood at 63.7%, higher than the industry median of 55.4% and Return on Equity was 35.5% as compared to the industry median of 12.2%. Considering the returns, trading levels, high ROE and decent outlook, we have valued the stock using EV/Sales multiple approach and arrived at a downside of lower double-digit (in percentage terms). The stock experienced a short interest of ~9.76% (as per the ASIC report of 13 January 2020). Hence, we have an “Expensive” rating on the stock at the current market price of $55.450, down by 2.463% on January 17, 2020.

Galaxy Resources Limited

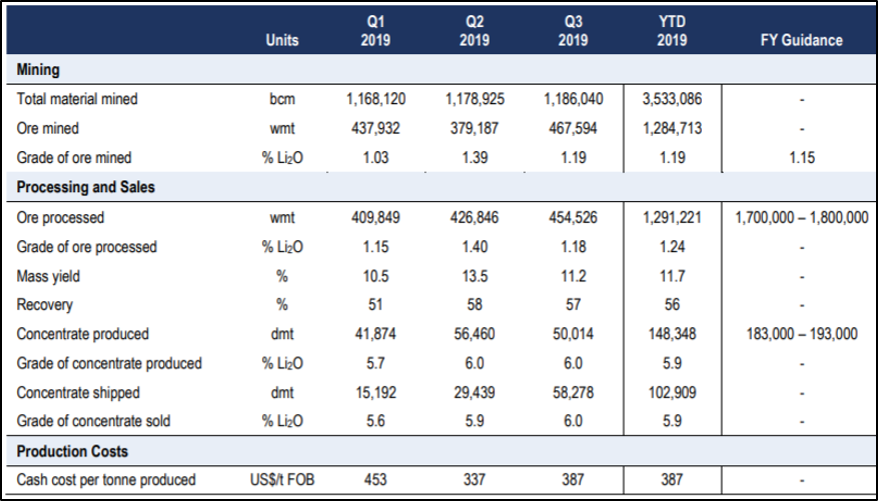

2019 Guidance Achieved: Galaxy Resources Limited (ASX: GXY) is engaged in the production of lithium concentrate and exploration for minerals in Australia, Canada and Argentina. The company has recently announced that it will release its quarterly activities report for the quarter ended 31 December 2019 on 23 January 2020. It also announced that the company achieved lithium concentrate production volume of 43,222 dry metric tonnes at the upper end of guidance of 35,000 – 45,000 dmt. During the quarter, the company sold 29,778 dmt of lithium concentrate, very close to its guidance of 30,000 - 45,000 dmt.

For the quarter ended 30 September 2019, production volume of Mt Cattlin of lithium concentrate stood at 50,014 dmt with a unit cash cost of US$387/dmt produced.

Production & Sales Statistics (Source: Company Reports)

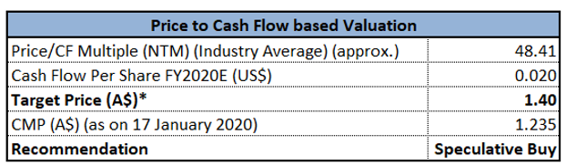

Valuation Methodology: Price/ Cash Flow Multiple Approach

Price/ Cash Flow Multiple Approach (Source: Thomson Reuters) * 1USD=1.45 AUD

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of GXY gave a return of 29.41% in the past one month and is trading close to its 52-weeks’ low level of $0.815, offering a good opportunity for accumulation. GXY has undertaken a review of all key contracts and will focus on cost reduction initiatives at Mt Cattlin. During FY19, EBITDA margin was broadly in-line with the industry median and stood at 30.9%. In the same time span, current ratio of the company was 4.97x, higher than the industry median of 1.87x. Considering the returns, trading levels, decent operating performance and positive outlook, we have valued the stock using Price/Cash Flow multiple based approach and arrived at a target upside of lower double-digit (in percentage terms). For the said purpose, we have considered Orocobre Ltd (ASX: ORE), Pilbara Minerals Ltd (ASX: PLS), Altura Mining Ltd (ASX: AJM), Imdex Ltd (ASX: IMD) and Red 5 Ltd (ASX: RED) as peers. The stock experienced a short interest of ~16.43% (as per the ASIC report of 13 January 2020). Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $1.235, up by 1.646% on January 17, 2020.

Orocobre Limited

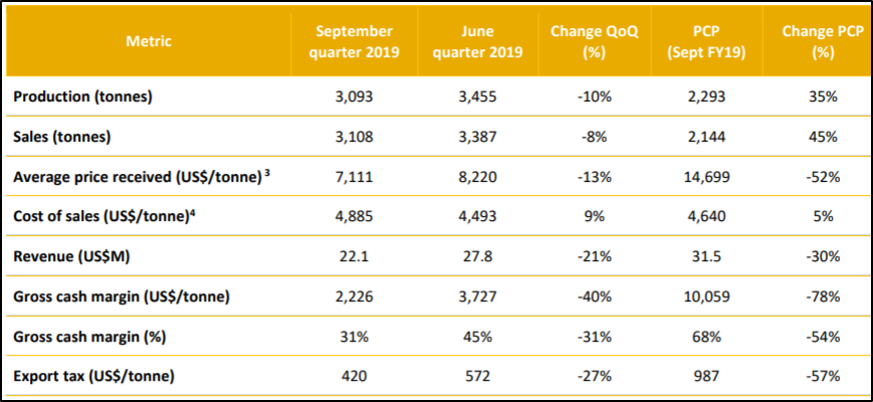

Record Production in September Quarter: Orocobre Limited (ASX: ORE) is minerals exploration and production company, focused on developing Lithium/Potash resources in Argentina. Despite the extended maintenance activity during August which saw a full-plant shutdown for five days, the company witnessed record production of 3,093 tonnes in Q1 of FY20, up by 35% on the previous corresponding period. In the same time span, quarterly sales revenue went down by 21% to US$22.1 million. This was mainly due to market softness.

FY19 Performance (Source: Company Reports)

Growth Opportunities: The company expects full-year production for FY20 which is likely to be at least 5% higher than FY19. It also anticipates the average sales price in the December quarter will be approximately US$6,200 to US$6,500/tonne.

Stock Recommendation: As per ASX, the stock of ORE gave a return of 29.24% in the past 6 months and a return of 31.14% in the last one month. The stock is inclined towards its 52-weeks’ high level of $4.04. During FY19, net margin of the company stood at 67.3%, higher than the industry median of 10.9%. In the same time period, current ratio of the company stood at 3.27x, as compared to the industry median of 1.81x. On the TTM basis, the stock is trading at an EV/Sales multiple of 7.3x, lower than the industry median (Chemicals) of 30.1x. The stock experienced a short interest of ~13.83% (as per the ASIC report of 13 January 2020). Considering the returns, trading levels, high net margin and positive outlook, we recommend a “Hold” rating on the stock at the current market price of $3.650, up by 1.955% on January 17, 2020.

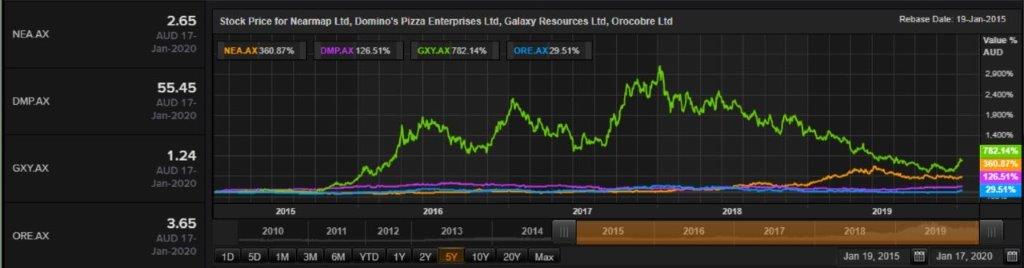

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...